PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1773363

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1773363

Pressure Ulcers Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

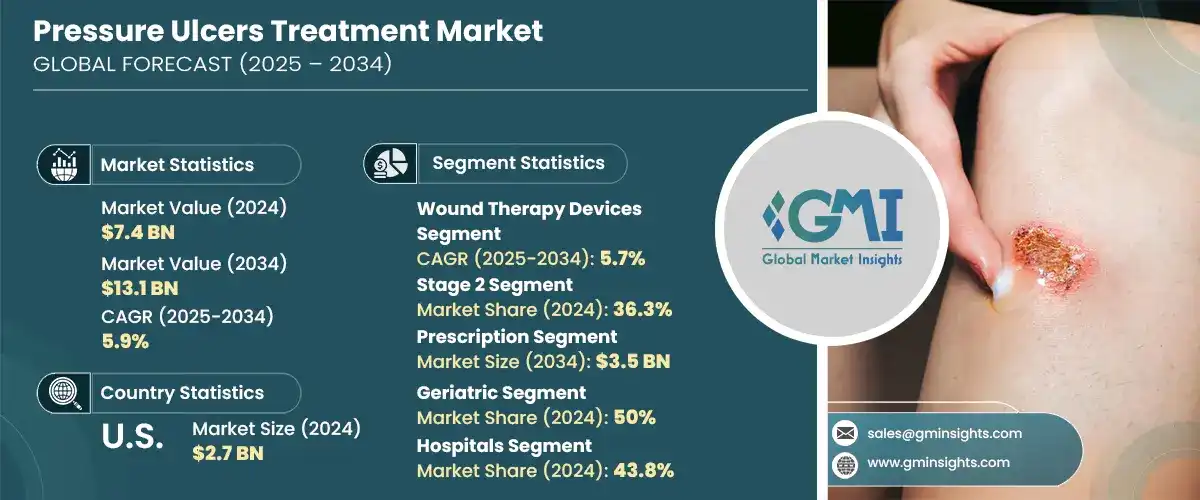

The Global Pressure Ulcers Treatment Market was valued at USD 7.4 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 13.1 billion by 2034. A major contributor to this growth is the aging population, particularly in developed nations, where limited mobility and prolonged immobility increase the risk of pressure ulcers. As individuals age, they are more likely to develop conditions that hinder movement, leading to the development of pressure sores. Additionally, the rising prevalence of lifestyle-related diseases such as obesity and diabetes-both of which are known to slow wound healing-further drives demand for effective wound care therapies. The growing incidence of chronic illnesses is translating into increased clinical cases of non-healing wounds, spurring the demand for sophisticated treatment approaches that improve patient outcomes.

The market is also benefiting from ongoing technological developments in wound care solutions. Innovations such as smart wound dressings, biologically active products, and modern therapy systems are revolutionizing pressure ulcer management by reducing healing time and improving comfort for patients. These solutions are increasingly adopted across both hospital settings and homecare environments due to their effectiveness in managing complex wounds. Greater awareness about early intervention and the benefits of preventive strategies is encouraging more patients and healthcare providers to opt for advanced products. Support from government healthcare programs, particularly in North America and Europe, is also bolstering adoption. Reimbursement schemes and clinical guidelines are reinforcing the preference for evidence-based wound care methods.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.4 Billion |

| Forecast Value | $13.1 Billion |

| CAGR | 5.9% |

Pressure ulcer treatment encompasses a range of medical solutions aimed at preventing and healing pressure-induced skin injuries. These ulcers, also referred to as bedsores or decubitus ulcers, generally occur in patients with limited mobility. The goal of treatment is to relieve pressure, promote tissue recovery, prevent infection, and enhance overall patient health. Therapeutic options include specialized dressings, biologics, therapy devices, and pharmaceutical agents designed for wound care. As clinical attention shifts toward improving healing outcomes, integrated treatment approaches that combine multiple therapies are gaining ground in the market.

Among the key product categories, wound therapy devices emerged as the top-performing segment in 2024 with a valuation of USD 3.3 billion and are projected to grow to USD 5.7 billion by 2034, registering a CAGR of 5.7%. These devices include technologies that support faster healing, reduce infection risk, and minimize patient discomfort. Their increasing use in hospitals and outpatient settings highlights the growing reliance on advanced technology to manage complex wounds more efficiently. Recent improvements in pressure management systems and automated wound monitoring are further enhancing the capabilities of this segment, leading to broader clinical adoption.

In terms of type, the prescription segment led in 2024 and is estimated to reach USD 3.5 billion by 2034. This dominance can be attributed to the higher efficacy of prescription therapies and the medical necessity for regulated interventions in treating severe cases. Products in this category include advanced topical formulations and systemic therapies that are prescribed for more complex or chronic wounds. As healthcare providers increasingly favor personalized treatment plans based on patient needs, the prescription category is expected to maintain its lead over the coming years.

By end use, hospitals represented the largest share of the market in 2024, accounting for 43.8%, and are projected to generate USD 5.5 billion in revenue by 2034. Hospitals remain the primary centers for treating pressure ulcers, particularly in advanced stages, owing to their comprehensive infrastructure, availability of skilled medical staff, and specialized departments for wound care. Patients with limited mobility or underlying health issues are more likely to seek hospital-based care where multidisciplinary approaches can be deployed effectively. Additionally, hospitals are often the first point of contact for patients requiring surgical intervention or intensive care.

Regionally, North America led the global market with a revenue of USD 2.9 billion in 2024 and is expected to reach USD 5 billion by 2034, growing at a CAGR of 5.5%. This leadership is supported by a well-established healthcare framework, early adoption of cutting-edge wound care technologies, and substantial investment in clinical research and development. The rising number of elderly individuals and the high prevalence of comorbid conditions such as obesity and diabetes in the region make advanced treatment solutions a necessity. Furthermore, favorable reimbursement scenarios and strong regulatory oversight have enabled a structured rollout of innovative therapies.

Leading companies continue to strengthen their positions through extensive product portfolios, strategic R&D investment, and global reach. Major participants are actively developing advanced wound management solutions and expanding their presence in emerging economies. Competitive strategies such as mergers, licensing agreements, and product launches are playing a vital role in shaping the landscape. Startups and smaller firms are also carving out a niche by focusing on specialized biologics and customizable care options, intensifying the pace of innovation within the industry.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Ulcer stage

- 2.2.4 Type

- 2.2.5 Age group

- 2.2.6 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of chronic disease

- 3.2.1.2 Growing advancement in wound care technologies

- 3.2.1.3 Increasing awareness and preventive care measures

- 3.2.1.4 Growing geriatric population

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment costs

- 3.2.3 Market opportunities

- 3.2.3.1 Expanding homecare-based wound management

- 3.2.3.2 Growing R&D investment and activities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology landscape

- 3.5 Regulatory landscape

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers and acquisitions

- 4.5.2 Partnerships and collaborations

- 4.5.3 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Wound care dressings

- 5.2.1 Alginate dressings

- 5.2.2 Foam dressings

- 5.2.3 Hydrocolloid dressings

- 5.2.4 Hydrogel dressings

- 5.2.5 Film dressings

- 5.2.6 Other wound care dressings

- 5.3 Biologics

- 5.3.1 Skin substitutes

- 5.3.2 Growth factors

- 5.3.3 Other biologics

- 5.4 Wound therapy devices

- 5.4.1 Negative pressure wound therapy

- 5.4.2 Hyperbaric oxygen therapy

- 5.4.3 Other wound therapy devices

- 5.5 Medications

- 5.6 Other products

Chapter 6 Market Estimates and Forecast, By Ulcer Stage, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Stage 1

- 6.3 Stage 2

- 6.4 Stage 3

- 6.5 Stage 4

Chapter 7 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Over-the-counter (OTC)

- 7.3 Prescription

Chapter 8 Market Estimates and Forecast, By Age Group, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Pediatric

- 8.3 Adult

- 8.4 Geriatric

Chapter 9 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Ambulatory surgical centers (ASCs)

- 9.4 Specialty clinics

- 9.5 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 3M Healthcare

- 11.2 AHA Hyperbarics

- 11.3 Integra LifeSciences

- 11.4 Ascend Laboratories

- 11.5 B. Braun

- 11.6 Baxter

- 11.7 BioTissue

- 11.8 Cardinal Health

- 11.9 Coloplast

- 11.10 Convatec

- 11.11 Ethicon (Johnson and Johnson)

- 11.12 GlaxoSmithKline (GSK)

- 11.13 Ipca Laboratories

- 11.14 LifeNet Health

- 11.15 Medline

- 11.16 MIMEDX

- 11.17 Molnlycke Health Care

- 11.18 Organogenesis

- 11.19 Pfizer

- 11.20 Smith & Nephew

- 11.21 StimLabs

- 11.22 Zimmer Biomet