PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1822595

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1822595

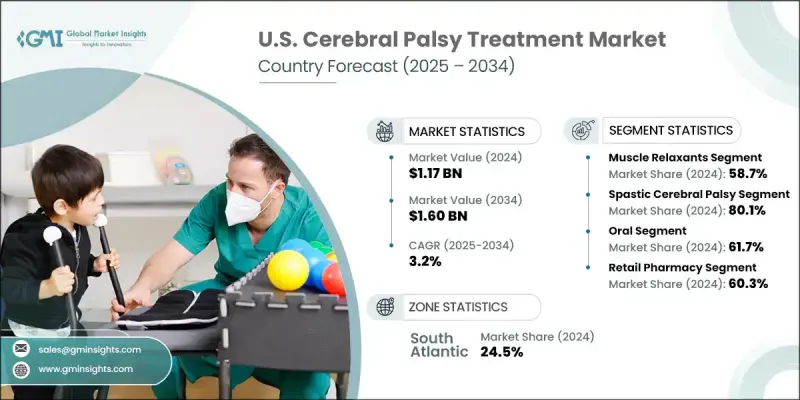

U.S. Cerebral Palsy Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

U.S. Cerebral Palsy Treatment Market was valued at USD 1.17 billion in 2024 and is estimated to grow at a CAGR of 3.2% to reach USD 1.60 billion by 2034.

This projected growth is fueled by a rising number of diagnosed cases nationwide, ongoing advancements in drug development, and expanding research investments. Increasing public and clinical focus on early diagnosis and supportive policies around reimbursement are also playing a central role. As more patients gain access to innovative therapies, the market continues to benefit from a growing commitment among healthcare providers and institutions to improve quality of life and motor function outcomes in individuals living with cerebral palsy through more individualized, multidisciplinary treatment options.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.17 Billion |

| Forecast Value | $1.60 Billion |

| CAGR | 3.2% |

Treatment for cerebral palsy in the U.S. spans a combination of therapeutic, surgical, pharmaceutical, and support-based approaches aimed at enhancing movement, managing symptoms, and improving daily living. Advances in oral drug therapies, injectable treatments, and assistive technologies are providing more tailored care strategies. Patients often undergo a combination of physical, speech, and occupational therapies, use assistive mobility tools, and receive medications such as muscle relaxants or undergo surgical interventions. These individualized treatment programs are developed to support greater independence and long-term symptom management, though the underlying condition itself is not curable.

The muscle relaxants segment held a 58.7% share in 2024, driven by their effectiveness in treating spasticity. Drugs such as diazepam, baclofen, and tizanidine are frequently used to reduce muscle stiffness and are often administered prior to orthopedic or neurosurgical procedures. These medications are critical components in rehabilitation regimens, supporting post-surgical recovery and long-term symptom relief. Patients typically access these drugs through a combination of hospital-based care, retail pharmacy options, and specialized channels for advanced delivery systems like intrathecal pumps.

The mixed type cerebral palsy segment is projected to grow at a CAGR of 3.8% through 2034. Individuals diagnosed with this form of CP experience overlapping symptoms, including spasticity, uncontrolled movements, and coordination challenges. Because of this complexity, treatment plans for mixed cerebral palsy increasingly rely on personalized pharmaceutical strategies. These include a blend of muscle relaxants, oral medications, and targeted injectables, often accompanied by surgical or rehabilitative therapies. This approach aligns with the increasing clinical shift toward customized treatment plans that cater to each patient's unique presentation of symptoms.

South Atlantic Cerebral Palsy Treatment Market held a 24.5% share in 2024. This dominance is linked to the presence of a robust support ecosystem made up of community groups, advocacy organizations, and regional care networks that promote early intervention and long-term management strategies. These networks actively promote public education, support fundraising for research, and help families better navigate the complex landscape of cerebral palsy treatments. Their efforts have helped improve patient access to care and encourage informed decision-making across the treatment journey.

Key companies active in the U.S. Cerebral Palsy Treatment Market include Teva, Novartis, AbbVie, Merz Pharmaceuticals, Amneal, UCB, GSK, Roche, CHEPLAPHARM, Dr. Reddy's, IPSEN, and VIATRIS. To strengthen their foothold in the U.S. cerebral palsy treatment landscape, leading companies are investing in clinical research to develop next-generation formulations with improved tolerability and long-acting efficacy. Many are also exploring innovative delivery systems such as infusion pumps and sustained-release drugs that improve compliance and reduce dosing frequency. Strategic alliances with hospitals and rehabilitation centers enable broader product integration into care protocols. Additionally, companies are expanding their reimbursement support programs and digital patient engagement platforms to enhance access and education for families and caregivers managing long-term treatment plans.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Country

- 1.3.2 Zonal/State

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Zonal trends

- 2.2.2 Drug type trends

- 2.2.3 Disease type trends

- 2.2.4 Route of administration trends

- 2.2.5 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of cerebral palsy

- 3.2.1.2 Advancements in drug formulations

- 3.2.1.3 Increased awareness and early diagnosis

- 3.2.1.4 Surging investments in research and development activities

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Adverse effects associated with drugs

- 3.2.3 Market opportunities

- 3.2.3.1 Development of targeted therapies

- 3.2.3.2 Strategic partnerships between pharma companies and pediatric hospitals

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Role of home healthcare in cerebral palsy management

- 3.5.1 Importance of home-based care for CP patients

- 3.5.2 Home-based therapy services (physical, occupational, speech)

- 3.5.3 Use of assistive devices and mobility aids at home

- 3.5.4 Home nursing and caregiver support dynamics

- 3.5.5 Cost benefit aspects of homecare vs hospital care

- 3.6 Technology and innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Reimbursement scenario

- 3.8 Brand analysis

- 3.9 Pipeline analysis

- 3.10 Emerging treatment therapies

- 3.11 Pricing analysis

- 3.12 Consumer behaviour analysis

- 3.13 Investment landscape

- 3.14 Epidemiological scenario

- 3.15 Porter's analysis

- 3.16 PESTEL analysis

- 3.17 Gap analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Drug Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Muscle relaxants

- 5.3 Anticonvulsants

- 5.4 Anticholinergics

- 5.5 Antidepressants

- 5.6 Other drug types

Chapter 6 Market Estimates and Forecast, By Disease Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Spastic cerebral palsy

- 6.2.1 Hemiplegia

- 6.2.2 Diplegia

- 6.2.3 Quadriplegia

- 6.3 Dyskinetic cerebral palsy

- 6.4 Ataxic cerebral palsy

- 6.5 Mixed cerebral palsy

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Injectable

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Retail pharmacy

- 8.3 Hospital pharmacy

- 8.4 Online pharmacy

Chapter 9 Market Estimates and Forecast, By Zone, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 East North Central

- 9.2.1 Illinois

- 9.2.2 Indiana

- 9.2.3 Michigan

- 9.2.4 Ohio

- 9.2.5 Wisconsin

- 9.3 West South Central

- 9.3.1 Arkansas

- 9.3.2 Louisiana

- 9.3.3 Oklahoma

- 9.3.4 Texas

- 9.4 South Atlantic

- 9.4.1 Delaware

- 9.4.2 Florida

- 9.4.3 Georgia

- 9.4.4 Maryland

- 9.4.5 North Carolina

- 9.4.6 South Carolina

- 9.4.7 Virginia

- 9.4.8 West Virginia

- 9.4.9 Washington, D.C.

- 9.5 Northeast

- 9.5.1 Connecticut

- 9.5.2 Maine

- 9.5.3 Massachusetts

- 9.5.4 New Hampshire

- 9.5.5 Rhode Island

- 9.5.6 Vermont

- 9.5.7 New Jersey

- 9.5.8 New York

- 9.5.9 Pennsylvania

- 9.6 East South Central

- 9.6.1 Alabama

- 9.6.2 Kentucky

- 9.6.3 Mississippi

- 9.6.4 Tennessee

- 9.7 West North Central

- 9.7.1 Iowa

- 9.7.2 Kansas

- 9.7.3 Minnesota

- 9.7.4 Missouri

- 9.7.5 Nebraska

- 9.7.6 North Dakota

- 9.7.7 South Dakota

- 9.8 Pacific Central

- 9.8.1 Alaska

- 9.8.2 California

- 9.8.3 Hawaii

- 9.8.4 Oregon

- 9.8.5 Washington

- 9.9 Mountain States

- 9.9.1 Arizona

- 9.9.2 Colorado

- 9.9.3 Utah

- 9.9.4 Nevada

- 9.9.5 New Mexico

- 9.9.6 Idaho

- 9.9.7 Montana

- 9.9.8 Wyoming

Chapter 10 Company Profiles

- 10.1 AbbVie

- 10.2 amneal

- 10.3 CHEPLAPHARM

- 10.4 Dr. Reddy's

- 10.5 GSK

- 10.6 IPSEN

- 10.7 Merz Pharmaceuticals

- 10.8 Novartis

- 10.9 Roche

- 10.10 Teva

- 10.11 UCB

- 10.12 VIATRIS