PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1871212

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1871212

Automotive Cybersecurity Semiconductors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

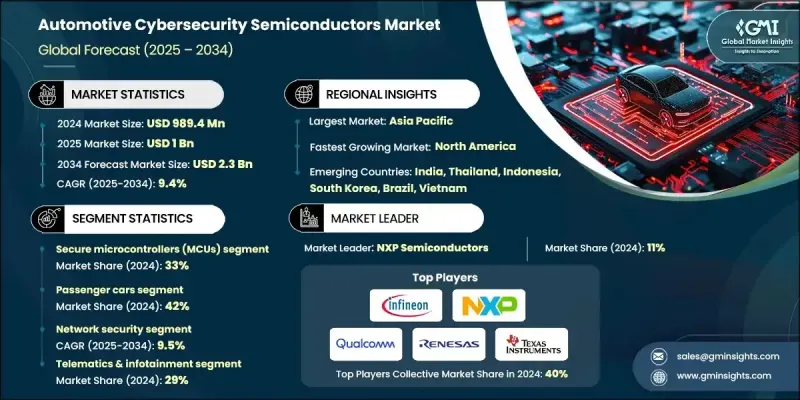

The Global Automotive Cybersecurity Semiconductors Market was valued at USD 989.4 million in 2024 and is estimated to grow at a CAGR of 9.4% to reach USD 2.3 Billion by

2034.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $989.4 Million |

| Forecast Value | $2.3 Billion |

| CAGR | 9.4% |

As vehicles become increasingly software-driven and connected, the demand for semiconductors with built-in security features is rising. These chips are essential for protecting automotive systems against cyber threats as automakers transition to electrified and software-defined architectures. The growing presence of advanced driver assistance systems and the shift toward autonomous mobility are accelerating the integration of secure hardware components. Automakers are embedding secure network elements, encryption-enabled processors, and trusted platforms to ensure secure communications, over-the-air updates, and real-time intrusion detection. These enhancements align with evolving regulatory frameworks, supporting compliance with international cybersecurity standards while strengthening vehicle data protection and system integrity.

With the rise in hybrid and electric mobility, there is a growing demand for safety-focused semiconductors that support secure battery monitoring, charging, and propulsion control systems. Next-generation vehicles require highly scalable and intelligent integrated circuits that offer seamless security across infotainment, diagnostics, and remote software management functions. Chipmakers are investing in AI-enabled cyber threat detection and improving the thermal endurance and ruggedness of semiconductor products to meet automotive-grade reliability. Vendors are expanding portfolios to address both passenger and commercial vehicle applications while also focusing on modularity, energy optimization, and compliance to drive value across the industry.

The secure microcontrollers (MCUs) segment held a 33% share in 2024 and is expected to grow at a 9.5% CAGR between 2025 and 2034. These MCUs provide essential hardware-based protections for communication interfaces, control units, and vehicle electronics by integrating secure boot, authentication, and encryption capabilities. With the rise in connected, electrified, and automated vehicle platforms, demand for secure MCUs is scaling rapidly. Regulatory mandates around automotive cybersecurity are compelling OEMs and suppliers to adopt tamper-resistant and cryptography-enabled components, making secure MCUs foundational to modern vehicle architectures.

The passenger cars segment held a 42% share in 2024 and is forecasted to grow at a CAGR of 9.8% through 2034. The growing shift toward connected and software-defined vehicles is prompting automakers to deploy advanced semiconductor-based protection systems across infotainment, ADAS, and vehicle-to-everything communications. Secure boot functions, hardware-based encryption, and embedded intrusion detection systems are being integrated into electronic control units to safeguard vehicle networks. As personal vehicles adopt more sophisticated digital platforms, the need for onboard cybersecurity continues to increase.

Asia Pacific Automotive Cybersecurity Semiconductors Market held a 42% share in 2024, with China generating USD 176.1 million. Strong digitalization trends, rapid deployment of ADAS features, and increasing EV production are propelling regional growth. Asia Pacific is witnessing significant advancements due to high R&D spending, localized semiconductor manufacturing, and stronger alliances between OEMs and cybersecurity technology providers. China's growth is particularly robust, backed by supportive policy frameworks and increasing adoption of secure communication modules across connected and autonomous mobility ecosystems.

Major companies in the Automotive Cybersecurity Semiconductors Market include Samsung Electronics, Microchip Technology, NXP Semiconductors, Infineon Technologies, Texas Instruments, STMicroelectronics, Renesas Electronics, Continental, Qualcomm Technologies, and ON Semiconductor. Companies operating in the automotive cybersecurity semiconductors sector are prioritizing innovation in hardware-based security features such as secure boot mechanisms, real-time intrusion detection, and cryptographic modules. Strategic investments in AI-driven threat detection engines are enhancing the resilience of chip architectures. Leading firms are aligning their portfolios with global cybersecurity compliance standards and developing scalable platforms for both passenger and commercial vehicles.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Vehicles

- 2.2.4 Security

- 2.2.5 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1.1 Growth drivers

- 3.2.1.2 Rising connectivity and digitalization of vehicles

- 3.2.1.3 Expansion of autonomous and ADAS technologies

- 3.2.1.4 Adoption of software-defined and centralized vehicle architecture

- 3.2.1.5 Growth in electric and connected vehicles (EVs and HEVs)

- 3.2.1.6 Increasing frequency and sophistication of cyber threats

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High complexity of cybersecurity integration across multiple ECUs and domains

- 3.2.2.2 Evolving and fragmented global cybersecurity regulations

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with connected and autonomous vehicle platforms

- 3.2.3.2 Growing adoption of electric and hybrid vehicles (EVs & HEVs)

- 3.2.3.3 Advancements in AI-driven and quantum-resistant security technologies

- 3.2.3.4 Rising demand for secure over-the-air (OTA) updates and cloud connectivity

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing analysis & cost structure dynamics

- 3.8.1 Historical price trend analysis (2021-2024)

- 3.8.2 Cost breakdown by component

- 3.8.3 Manufacturing cost structure analysis

- 3.8.4 R&D investment impact on pricing

- 3.8.5 Volume-based pricing strategies

- 3.9 Regional Price Variations & Influencing Factors

- 3.10 Patent analysis

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly Initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Macro-economic dynamics impact analysis

- 3.12.1 Global semiconductor shortage impact (2021-2024)

- 3.12.2 Inflation & raw material cost pressures

- 3.12.3 Geopolitical trade tensions & supply chain disruptions

- 3.12.4 Currency fluctuation impact on global pricing

- 3.12.5 Economic recession impact on automotive demand

- 3.12.6 Interest rate changes & capital investment decisions

- 3.13 Micro-economic dynamics & industry-specific factors

- 3.13.1 Automotive production volume fluctuations

- 3.13.2 Technology adoption rate variations by OEM

- 3.13.3 Competitive pricing pressure analysis

- 3.13.4 Customer bargaining power & procurement strategies

- 3.13.5 Supplier concentration & market power dynamics

- 3.13.6 Product lifecycle & technology refresh cycles

- 3.14 Threat landscape & industry response analysis

- 3.14.1 Emerging cybersecurity threat vectors

- 3.14.2 Nation-state & advanced persistent threats

- 3.14.3 Supply chain attack vulnerabilities

- 3.14.4 Zero-day exploit risks & mitigation strategies

- 3.14.5 Quantum computing threat timeline

- 3.14.6 Industry collaborative defense initiatives

- 3.15 Company strategic response & adaptation strategies

- 3.15.1 Vertical integration vs partnership strategies

- 3.15.2 Geographic diversification & nearshoring trends

- 3.15.3 Technology portfolio expansion strategies

- 3.15.4 Regulatory compliance investment strategies

- 3.15.5 Talent acquisition & retention challenges

- 3.15.6 Customer relationship & lock-in strategies

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 (USD Mn, Units)

- 5.1 Key trends

- 5.2 Hardware security modules (HSMs)

- 5.3 Secure microcontrollers (MCUs)

- 5.4 Trusted platform modules (TPMs)

- 5.5 Crypto processors / co-processors

- 5.6 Network security chips

- 5.7 Trusted execution environments (TEE)

Chapter 6 Market Estimates & Forecast, By Vehicles, 2021 - 2034 (USD Mn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchbacks

- 6.2.2 Sedans

- 6.2.3 SUVs

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles

- 6.3.2 Medium commercial vehicles

- 6.3.3 Heavy commercial vehicles

- 6.4 Electric vehicles

- 6.5 Autonomous vehicles

Chapter 7 Market Estimates & Forecast, By Security, 2021 - 2034 (USD Mn, Units)

- 7.1 Key trends

- 7.2 Network security

- 7.3 Application security

- 7.4 Cloud security

- 7.5 Endpoint security

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Mn, Units)

- 8.1 Key trends

- 8.2 Telematics & infotainment

- 8.3 ADAS & autonomous systems

- 8.4 Powertrain & EV systems

- 8.5 Vehicle-to-everything (V2X)

- 8.6 Gateway & zonal controllers

- 8.7 Over-the-Air (OTA) updates

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.3.8 Portugal

- 9.3.9 Croatia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Singapore

- 9.4.7 Thailand

- 9.4.8 Indonesia

- 9.4.9 Vietnam

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Turkey

Chapter 10 Company Profiles

- 10.1 Contract Manufacturers

- 10.1.1 GlobalFoundries

- 10.1.2 Samsung Electronics

- 10.1.3 Taiwan Semiconductor Manufacturing Company (TSMC)

- 10.1.4 United Microelectronics

- 10.2 Integrated Device Manufacturers

- 10.2.1 Analog Devices

- 10.2.2 Continental

- 10.2.3 Infineon Technologies

- 10.2.4 Microchip Technology

- 10.2.5 NXP Semiconductors

- 10.2.6 ON Semiconductor

- 10.2.7 Renesas Electronics

- 10.2.8 STMicroelectronics

- 10.2.9 Texas Instruments

- 10.3 Fabless Semiconductor Companies

- 10.3.1 Broadcom

- 10.3.2 Marvell Technology

- 10.3.3 Qualcomm Technologies

- 10.4 IP Providers

- 10.4.1 ARM Holdings

- 10.4.2 Cadence Design Systems

- 10.4.3 Imagination Technologies

- 10.4.4 Synopsys