PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959610

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959610

Hair Growth Supplement and Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

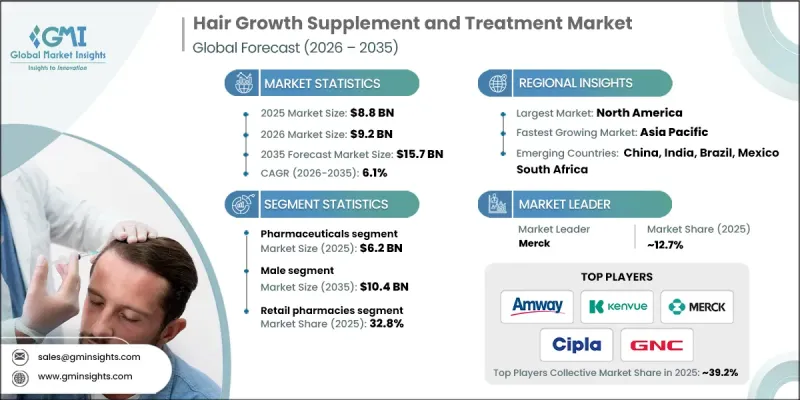

The Global Hair Growth Supplement and Treatment Market was valued at USD 8.8 billion in 2025 and is estimated to grow at a CAGR of 6.1% to reach USD 15.7 billion by 2035.

The market is witnessing strong expansion due to the rising prevalence of hair disorders such as alopecia areata, telogen effluvium, and other scalp conditions, driving consumers to seek effective solutions that enhance appearance and self-confidence. Increasing hair thinning, growing awareness around personal grooming, and the availability of clinically supported over-the-counter and prescription solutions across both retail and online channels are further fueling demand. Consumers are now prioritizing preventive hair care, wellness, and scientifically validated treatments, which has resulted in rising adoption of dietary supplements, topical solutions, and non-invasive therapeutic devices. The convergence of awareness, accessibility, and technological innovation is positioning hair growth supplements and treatments as a core component of modern personal care and healthcare routines.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $8.8 Billion |

| Forecast Value | $15.7 Billion |

| CAGR | 6.1% |

The market includes a broad range of products designed to prevent hair loss, stimulate regrowth, and improve overall scalp health. This encompasses oral supplements containing vitamins, minerals, and botanical extracts, alongside topical and pharmaceutical therapies, which include prescription medications and advanced non-invasive devices.

The pharmaceuticals segment generated USD 6.2 billion in 2025, driven by the growing demand for clinically proven interventions for androgenetic alopecia and other forms of hair loss. Oral medications, topical solutions, injectables, and specialized devices continue to gain traction due to their high efficacy and improved patient outcomes.

The men segment is expected to reach USD 10.4 billion by 2035, growing at a CAGR of 5.9%. Male dominance is largely attributed to the high prevalence of androgenetic alopecia, with nearly half of men affected by age 50 and a significant majority by age 80. The convenience of supplements, coupled with technologically advanced topical treatments and non-invasive devices such as laser caps and scalp stimulators, has strengthened adoption among male consumers, contributing substantially to market growth.

North America Hair Growth Supplement and Treatment Market accounted for 44.3% share in 2025, maintaining leadership due to the region's high hair loss prevalence and strong adoption of innovative treatments. Growth is further supported by advances in pharmaceuticals, dietary supplements, and non-invasive devices, along with rising consumer preference for natural and clinically validated hair care solutions. The combination of accessible healthcare infrastructure, consumer awareness, and regulatory support underpins North America's dominant position.

Key players in the Global Hair Growth Supplement and Treatment Market include GNC Holdings, Cipla Limited, Amway Corporation, Pfizer, Nature's Bounty, HUM Nutrition, ExoCoBio, Eli Lilly and Company, OUAI Healthcare, Merck, Viviscal Limited (Church & Dwight), Kenvue, Lexington International, Curallux, Keranique, and Nutraceutical Wellness. Companies in this market are employing strategies such as investing heavily in R&D to create clinically validated and multi-functional products, expanding product portfolios to target gender-specific and age-specific needs, and leveraging advanced delivery technologies to improve efficacy. Strategic partnerships with dermatologists, wellness influencers, and online health platforms are used to enhance brand credibility and reach. Firms are also focusing on omnichannel distribution, combining e-commerce, retail, and subscription services to boost accessibility and retention, while emphasizing marketing campaigns centered on scientific validation, natural ingredients, and visible results to strengthen their market foothold and consumer trust.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Type trends

- 2.2.3 Gender trends

- 2.2.4 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of hair loss and alopecia

- 3.2.1.2 Rising consumer awareness and self-care trends

- 3.2.1.3 Expansion of e-commerce and direct-to-consumer channels

- 3.2.1.4 Advancements in treatment technologies and clinical research

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Growing availability of alternative treatment options

- 3.2.2.2 Concerns associated with pharmacological treatments

- 3.2.3 Market opportunities

- 3.2.3.1 Rising demand for personalized and precision solutions

- 3.2.3.2 Growth in combination therapies and adjunct solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Pipeline analysis

- 3.6 Pricing analysis

- 3.7 Future market trends

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Supplements

- 5.2.1 By product type

- 5.2.1.1 Single-ingredient supplements

- 5.2.1.2 Multi-ingredient supplements

- 5.2.2 By dosage form

- 5.2.2.1 Powder

- 5.2.2.2 Gummies

- 5.2.2.3 Tablets

- 5.2.2.4 Capsules

- 5.2.2.5 Liquid

- 5.2.2.6 Other dosage forms

- 5.2.1 By product type

- 5.3 Pharmaceuticals

- 5.3.1 Oral medications

- 5.3.2 Topical and injectables

- 5.3.3 Devices

Chapter 6 Market Estimates and Forecast, By Gender, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Male

- 6.3 Female

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospital pharmacies

- 7.3 E-commerce

- 7.3.1 Online retailers

- 7.3.2 Brand-owned websites

- 7.4 Retail pharmacies

- 7.5 Drug stores

- 7.6 Other distribution channels

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Hair supplements

- 9.1.1 Amway Corporation

- 9.1.2 GNC Holdings

- 9.1.3 HUM Nutrition

- 9.1.4 Nature’s Bounty

- 9.1.5 Nutraceutical Wellness

- 9.1.6 OUAI Healthcare

- 9.1.7 Phyto

- 9.1.8 Viviscal Limited (Church & Dwight)

- 9.2 Hair treatment

- 9.2.1 Cipla

- 9.2.2 Curallux

- 9.2.3 Eli Lilly and Company

- 9.2.4 ExoCoBio

- 9.2.5 Keranique

- 9.2.6 Kenvue

- 9.2.7 Lexington International

- 9.2.8 Merck

- 9.2.9 Pfizer