PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043949

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043949

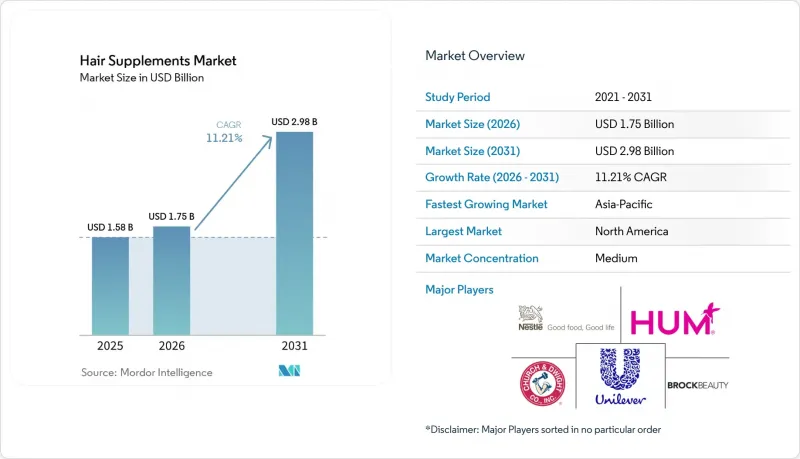

Hair Supplements - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The hair supplements market size is expected to increase from USD 1.58 billion in 2025 to USD 1.75 billion in 2026 and reach USD 2.98 billion by 2031, growing at a CAGR of 11.21% over 2026-2031.

Adults aged 18-34, now expressing hair-loss concerns at double the rate of a decade ago, are driving a significant shift from topical solutions to ingestible, multi-nutrient routines. This demographic increasingly prioritizes holistic approaches to hair health, reflecting broader wellness trends. Platforms like TikTok and Instagram have played a pivotal role in rebranding supplements, positioning them as essential lifestyle staples rather than traditional medications. At the same time, e-commerce subscriptions are simplifying repeat purchases, offering convenience, and fostering the growth of premium brands. Women, disproportionately affected by stress-related telogen effluvium, not only seek treatment more frequently but also tend to make larger purchases and exhibit longer retention rates, highlighting their importance as a key consumer group. Additionally, major global consumer-goods companies are actively consolidating the market by acquiring clinically validated brands. This strategy secures subscription-based revenue streams and garners dermatologist endorsements, further strengthening their market position.

Global Hair Supplements Market Trends and Insights

Rising prevalence of hair thinning and alopecia among millennials

Two in five adults aged 18-34 actively worry about hair loss, with women reporting noticeably higher stress-induced shedding than men. This concern is driven by factors such as lifestyle stress, hormonal imbalances, and environmental conditions. Additionally, 25% of men affected by male pattern baldness begin losing hair before age 21, highlighting the early onset of this condition in a significant portion of the male population. Alopecia areata now impacts over 17 million people worldwide and is projected to climb, broadening the pool beyond androgenetic cases and increasing the demand for effective solutions. Younger consumers display a 69% willingness to try ingestibles, reflecting a growing interest in innovative and convenient hair care options. Declining reliance on finasteride, due to its perceived side effects, is nudging many toward natural alternatives that are considered safer. Oral minoxidil prescriptions are on the rise; however, its side-effect profile continues to drive curiosity for nutraceuticals that blend botanicals with vitamins, offering a holistic approach to hair health. The demographic surge directly feeds the hair supplements market as subscription brands successfully convert early experimentation into habitual use, fostering long-term customer loyalty.

Social-media-fueled "beauty-from-within" trend driving supplement uptake

In mid-2024, U.S. searches for "hair growth" surged past 1.3 million monthly, highlighting a strong digital interest and growing consumer focus on hair health solutions. While influencer endorsements once drove viral sales, heightened FTC scrutiny on undisclosed advertisements has pivoted the strategy towards greater clinical transparency, emphasizing the importance of trust and credibility in marketing. Nutrafol, hailed as the top dermatologist-recommended brand, showcases the power of peer-reviewed data in transforming mere likes into committed purchases by building consumer confidence. By emphasizing both skin elasticity and hair density, Nutrafol elevates its average order value, catering to collagen enthusiasts in search of comprehensive solutions that address multiple concerns. This blend of aspirational marketing and substantiated claims ensures hair supplements remain a staple in the daily feeds of their target audience, reinforcing their relevance in a competitive market.

Patchy global rules on supplement efficacy and labeling

The FDA allows statements like "supports hair health," but bans disease-related claims unless a supplement has drug approval. Europe's EFSA system is more stringent, resulting in most growth claims being left unapproved due to the high level of scientific evidence required for validation. In China, while the imported-product channel facilitates entry, it imposes restrictions on certain botanicals, particularly those with limited safety data or unclear efficacy. Meanwhile, Japan mandates a 60-day dossier submission under its Foods with Function Claims model before any product can be sold, requiring detailed scientific substantiation and regulatory compliance documentation. This regulatory patchwork escalates compliance costs, giving an edge to established players with dedicated regulatory teams who can navigate these complexities more efficiently. As a result, smaller innovators face delays in product launches, which in turn moderates the rapid expansion of the hair supplements market by creating barriers to entry and slowing innovation.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of e-commerce and DTC nutraceutical brands

- Shift toward preventive and holistic self-care

- Heightened consumer skepticism after influencer-led scandals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, vitamins and minerals captured 48.37% of the hair supplements market, underscoring their enduring status as the cornerstone of hair health. Yet, there's a noticeable shift: consumers are moving from standalone ingredients like biotin to more holistic, synergistic blends. Today's formulations are increasingly merging nutrients with functional botanicals. For instance, ashwagandha is being added for its stress-relief properties, while saw palmetto is recognized for its role in DHT regulation, boosting the products' perceived effectiveness. Notably, in 2026, saw palmetto received clinical validation, bolstering consumer trust. This endorsement has prompted formulators to elevate their traditional products into premium, multifunctional offerings. Furthermore, innovative formats like gummies are making waves. Brands like Power Gummies tout a 21-24% boost in hair density in just 90 days, showcasing the tangible results and enhancing consumer adherence.

Collagen and protein blends are on a rapid ascent, with projections indicating a CAGR of 12.25% through 2031. This surge is fueled by a growing consumer inclination towards holistic beauty solutions. Marine-derived collagen peptides, celebrated for their superior bioavailability, are becoming increasingly popular. Users are witnessing tangible hair health improvements within just three months, fostering daily consumption and establishing collagen as an essential ingredient rather than a mere supplement. Brands are capitalizing on this momentum, rolling out hybrid "total beauty" formulations. By blending collagen with ceramides and hyaluronic acid, they're addressing hair, skin, and nail needs in one product. This strategy not only justifies premium pricing but also boosts consumer lifetime value, transitioning users from single-purpose buyers to loyal subscribers.

In 2025, capsules and tablets dominated the hair supplements market, capturing 46.04% of the total share. Their stronghold is bolstered by consumer trust and a perceived clinical efficacy. Pharmacists widely recommend these formats, viewing them as reliable and standardized systems for delivering targeted nutrition. Their convenience, precise dosing, and familiarity keep them in high demand among traditional supplement users. Even with the rise of alternative formats, consumers still gravitate towards capsules and tablets for their straightforward, no-frills approach to supplementation. This enduring preference underscores the established credibility of these formats and their integral role in structured health routines.

Gummies are emerging as the fastest-growing segment, with projections indicating a CAGR of 12.78% through 2031. This surge is primarily fueled by younger consumers, especially Gen Z, who are gravitating towards more enjoyable supplement experiences. Many in this demographic are moving away from traditional pills, citing "pill fatigue." Instead, they are opting for candy-like gummies that boast appealing taste and texture. Furthermore, the bright and aesthetically pleasing packaging of these gummies enhances their visibility on social media, turning product unboxing into a form of organic promotion. Gummies also offer the advantage of higher nutrient intake, such as vitamin C or collagen, without the hassle of multiple doses. Sugar-free variants cater to those with fitness and wellness aspirations. This blend of convenience, taste, and alignment with lifestyle goals is propelling the rapid adoption of gummies, reshaping consumer expectations in the realm of supplement delivery formats.

The Hair Supplements Market Report is Segmented by Product Type (Vitamins and Minerals, Botanical Extracts, and More), Form (Capsules and Tablets, Gummies and Chewables, and More), Distribution Channel (Supermarkets/Hypermarkets, Pharmacies and Drug Stores, and More), End User (Women and Men), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

In 2025, North America accounted for 32.06% of global revenue, buoyed by endorsements from dermatologists and an FDA framework permitting structure-function claims. The U.S. spearheads innovations in gummies and powders, bolstered by direct-to-consumer logistics that streamline refills. While Canada and Mexico lag in sheer numbers, they leverage cross-border e-commerce to access U.S. brands, even in the absence of local manufacturing plants. The region's strong consumer awareness and high disposable income levels further drive market growth. Additionally, the presence of established players and frequent product launches contributes to maintaining North America's dominance.

Asia-Pacific emerges as the fastest-growing region, boasting an 11.93% CAGR. This surge is fueled by China's 250 million consumers prioritizing hair health and India's blend of Ayurvedic traditions with contemporary nutraceuticals. Cross-border platforms empower brands to bypass lengthy local registrations, enabling swift market resonance testing. Increasing urbanization and rising middle-class populations in the region further support market expansion. Moreover, government initiatives promoting health and wellness products are expected to create additional growth opportunities for hair supplements in the Asia-Pacific.

Europe experienced a robust 24% CAGR from 2020 to 2024. France, the U.K., and Germany lead the regional demand, albeit with constraints from EU health claim regulations. The market witnessed gummies and powders outpacing pills, indicative of a trend towards snack and smoothie integrations. The growing popularity of vegan and plant-based supplements is also shaping consumer preferences in the region. Furthermore, advancements in product formulations and packaging innovations are enhancing the appeal of hair supplements across European markets. Southern and Eastern European states are gaining traction, driven by local influencers and competitively priced SKUs. Meanwhile, South America and the Middle East and Africa are still in nascent stages: Brazil, Argentina, the UAE, Saudi Arabia, and South Africa anchor the pharmacy-first markets, yet enhancements in logistics and a rise in disposable incomes signal promising growth for the hair supplements market. The increasing penetration of e-commerce platforms is also facilitating market access in these regions. Additionally, growing awareness campaigns about hair health are expected to boost demand in these emerging markets.

- Unilever Plc

- Church and Dwight Co., Inc. (Viviscal)

- Nestle SA

- Brock Beauty Inc (Hairfinity)

- HUM Nutrition Inc.

- JSHealth

- SugarBearHair

- The Clorox Company (Nutranext)

- Scientific Hair Research LLC (Keranique)

- Amway Corp

- Swisse Wellness

- Wellbel Inc.

- GNC Holdings

- Country Life, LLC

- Vegaboost

- Pharmavite (Nature Made)

- Proempire LLC (Vitamatic)

- Vitabiotics Ltd.

- Aesthetic Nutrition Pvt Ltd (Power Gummies)

- HealthKart

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising prevalence of hair thinning and alopecia in younger cohorts

- 4.2.2 Social-media-fuelled "beauty-from-within" trend driving supplement uptake

- 4.2.3 Expansion of e-commerce and DTC nutraceutical brands

- 4.2.4 Shift toward preventive and holistic self-care

- 4.2.5 Advances in proteomic-based bio-active discovery for hair cycling

- 4.2.6 Advancement in personalized supplement recommendation

- 4.3 Market Restraints

- 4.3.1 Patchy global rules on supplement efficacy and labelling

- 4.3.2 Heightened consumer scepticism after influencer-led scandals

- 4.3.3 Cannabinoid and adaptogen cross-category substitutes stealing share

- 4.3.4 Trace-element toxicity concerns in long-term megadose regimens

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Product Type

- 5.1.1 Vitamins and Minerals

- 5.1.2 Botanical Extracts

- 5.1.3 Collagen and Protein Supplements

- 5.1.4 Other Functional Actives

- 5.2 By Form

- 5.2.1 Capsules and Tablets

- 5.2.2 Gummies and Chewables

- 5.2.3 Powder Mixes

- 5.2.4 Liquid Shots

- 5.2.5 Others

- 5.3 By End User

- 5.3.1 Men

- 5.3.2 Women

- 5.4 By Distribution Channel

- 5.4.1 Supermarkets/Hypermarkets

- 5.4.2 Pharmacies and Drug Stores

- 5.4.3 Specialty Health Stores

- 5.4.4 Online Retail Stores

- 5.4.5 Other Off-Trade Channels

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 France

- 5.5.2.3 United Kingdom

- 5.5.2.4 Spain

- 5.5.2.5 Netherlands

- 5.5.2.6 Italy

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 South Africa

- 5.5.5.3 Saudi Arabia

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Unilever Plc

- 6.4.2 Church and Dwight Co., Inc. (Viviscal)

- 6.4.3 Nestle SA

- 6.4.4 Brock Beauty Inc (Hairfinity)

- 6.4.5 HUM Nutrition Inc.

- 6.4.6 JSHealth

- 6.4.7 SugarBearHair

- 6.4.8 The Clorox Company (Nutranext)

- 6.4.9 Scientific Hair Research LLC (Keranique)

- 6.4.10 Amway Corp

- 6.4.11 Swisse Wellness

- 6.4.12 Wellbel Inc.

- 6.4.13 GNC Holdings

- 6.4.14 Country Life, LLC

- 6.4.15 Vegaboost

- 6.4.16 Pharmavite (Nature Made)

- 6.4.17 Proempire LLC (Vitamatic)

- 6.4.18 Vitabiotics Ltd.

- 6.4.19 Aesthetic Nutrition Pvt Ltd (Power Gummies)

- 6.4.20 HealthKart

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK