PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959659

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959659

Antibiotic Resistance Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

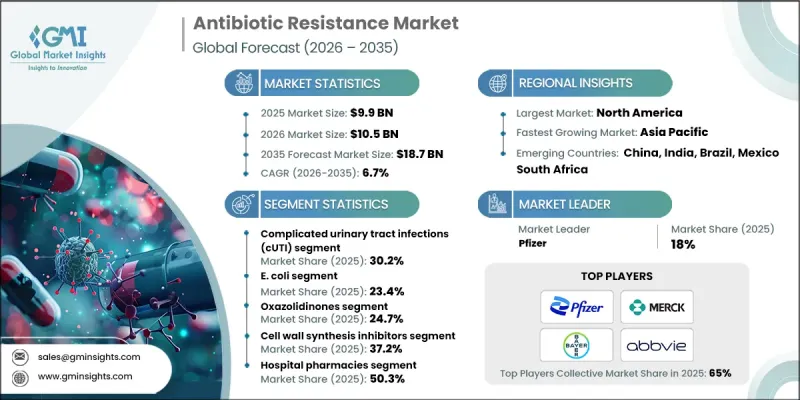

The Global Antibiotic Resistance Market was valued at USD 9.9 billion in 2025 and is estimated to grow at a CAGR of 6.7% to reach USD 18.7 billion by 2035.

The market is fueled by the escalating global crisis of antimicrobial resistance (AMR), which has become a major concern for healthcare systems worldwide. The increasing incidence of multidrug-resistant infections has created a pressing demand for novel antibiotics, rapid diagnostic solutions, and innovative treatment options. Misuse and overuse of antibiotics, the prevalence of hospital-acquired infections, and the emergence of resistant pathogens are driving research and investment into new therapies. The growing elderly population, higher surgical interventions, and the rising prevalence of chronic diseases are heightening infection risks, emphasizing patient safety and healthcare cost management. Governments, health authorities, and pharmaceutical firms are promoting stewardship programs, regulatory incentives, and funding initiatives, while increased awareness among healthcare professionals and patients supports the market's expansion.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $9.9 Billion |

| Forecast Value | $18.7 Billion |

| CAGR | 6.7% |

The complicated urinary tract infections (cUTIs) segment accounted for 30.2% share in 2025, reflecting their high prevalence and clinical complexity. Patients with underlying health conditions such as diabetes or kidney disorders are particularly vulnerable, which boosts the demand for advanced antibiotic therapies. cUTIs often involve multidrug-resistant pathogens, necessitating broad-spectrum treatments to reduce hospital stays and minimize complications. Clinical guidelines and research initiatives continue to shape effective treatment protocols, driving the adoption of newer therapies capable of addressing resistant strains efficiently.

The Escherichia coli (E. coli) segment captured 23.4% share in 2025 and is anticipated to see substantial growth. E. coli infections pose significant public health challenges, often resulting in severe gastrointestinal illness and complications that can escalate healthcare costs. Rising outbreaks and the associated healthcare burden are motivating increased investment in therapies and diagnostics that specifically target multidrug-resistant E. coli strains, highlighting the critical role of this segment within the broader antibiotic resistance market.

U.S Antibiotic Resistance Market reached USD 3.7 billion in 2025. The country represents one of the most advanced markets globally, supported by a robust healthcare infrastructure, stringent surveillance systems, and significant investment in antimicrobial stewardship programs. The high prevalence of multidrug-resistant pathogens, including resistant Staphylococcus aureus and Pseudomonas aeruginosa strains, continues to drive demand for rapid diagnostics and innovative therapies, positioning the U.S. as a key growth driver in the global market.

Major players in the Global Antibiotic Resistance Market include Wockhardt, Johnson & Johnson, AbbVie, Pfizer, Paratek Pharmaceuticals, Bayer AG, Melinta Therapeutics, Shionogi & Co., Ltd., Tetraphase Pharmaceuticals, and Basilea Pharmaceutical. Companies in the antibiotic resistance market are employing several strategies to strengthen their presence and market position. They are investing heavily in research and development to discover novel antibiotics and therapies capable of combating multidrug-resistant pathogens. Strategic partnerships and collaborations with healthcare institutions, academic organizations, and government bodies help accelerate clinical trials and regulatory approvals. Firms are also focusing on expanding their global footprint, particularly in regions with high AMR prevalence. Investments in rapid diagnostic technologies and companion therapies enhance treatment efficacy and patient outcomes.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Disease trends

- 2.2.2 Pathogen trends

- 2.2.3 Drug class trends

- 2.2.4 Mechanism of action trends

- 2.2.5 Distribution channel trends

- 2.2.6 Regional trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of antibiotic-resistant infections

- 3.2.1.2 Increasing investments for research and development of novel antibiotics

- 3.2.1.3 Growing need for new antibiotic therapies

- 3.2.1.4 Increasing global public health concern and awareness

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Rapid emergence of resistance to new drugs

- 3.2.2.2 Complex regulatory and development process

- 3.2.3 Market opportunities

- 3.2.3.1 Development of next-generation antibiotics and alternative therapies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Patent analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Disease, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Complicated urinary tract infections

- 5.3 Complicated intra-abdominal infections

- 5.4 Bloodstream infections

- 5.5 Acute bacterial skin and skin-structure infections

- 5.6 Community-acquired bacterial pneumonia

- 5.7 Hospital-acquired bacterial pneumonia

Chapter 6 Market Estimates and Forecast, By Pathogen, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 E. coli - Escherichia coli

- 6.3 K. pneumoniae - Klebsiella pneumoniae

- 6.4 P. aeruginosa - Pseudomonas aeruginosa

- 6.5 S. aureus - Staphylococcus aureus

- 6.6 Baumannii - Acinetobacter baumannii

- 6.7 S. pneumoniae - Streptococcus pneumoniae

- 6.8 H. influenzae

Chapter 7 Market Estimates and Forecast, By Drug Class, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Oxazolidinones

- 7.3 Cephalosporin

- 7.4 Lipoglycopeptides

- 7.5 Combination therapies

- 7.6 Tetracyclines

- 7.7 Other drug classes

Chapter 8 Market Estimates and Forecast, By Mechanism of Action, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Cell wall synthesis inhibitors

- 8.3 Protein synthesis inhibitors

- 8.4 DNA synthesis inhibitors

- 8.5 RNA synthesis inhibitors

- 8.6 Other mechanism of actions

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Hospital pharmacies

- 9.3 Retail pharmacies

- 9.4 Online pharmacies

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 AbbVie

- 11.2 Basilea Pharmaceutical

- 11.3 Bayer AG

- 11.4 Merck and Co.

- 11.5 Melinta Therapeutics

- 11.6 Johnson & Johnson

- 11.7 Paratek Pharmaceuticals

- 11.8 Pfizer

- 11.9 Shionogi & Co., Ltd.

- 11.10 Tetraphase Pharmaceuticals

- 11.11 Wockhardt