PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982363

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982363

Barge Transportation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

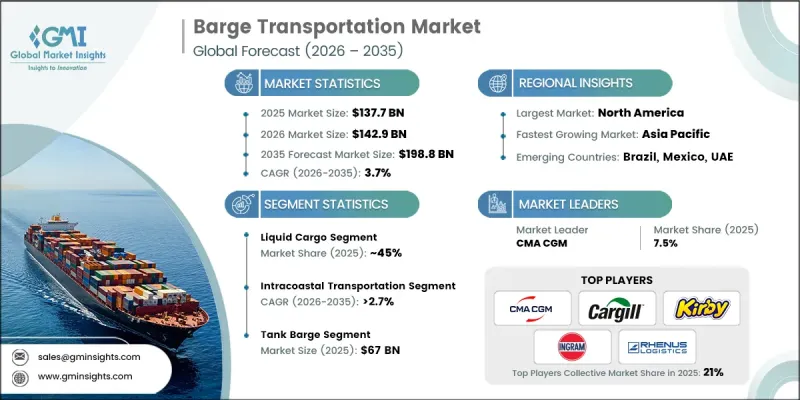

The Global Barge Transportation Market was valued at USD 137.7 billion in 2025 and is estimated to grow at a CAGR of 3.7% to reach USD 198.8 billion by 2035.

The market is expanding as demand for inland waterway transport rises alongside global trade volumes and the need for efficient, safe, and environmentally sustainable cargo movement. Regulatory incentives promoting low-emission transport, sustainability mandates, and government policies in North America, Europe, and Asia Pacific are encouraging fleet owners, logistics providers, and barge operators to adopt advanced fleet management, predictive maintenance, and operational optimization solutions. Pressure to maximize vessel uptime, improve fuel efficiency, and meet strict safety and environmental standards is driving investment in engine diagnostics, hull maintenance, auxiliary system checks, automated navigation, and emission control technologies. Fleet modernization, expansion of inland shipping corridors, and adoption of containerized and bulk cargo barges further support the uptake of high-efficiency, data-driven solutions, while IoT-enabled monitoring, telematics, and integrated performance platforms are transforming traditional barge operations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $137.7 Billion |

| Forecast Value | $198.8 Billion |

| CAGR | 3.7% |

The liquid cargo segment held a 45% share and is expected to grow at a CAGR of 2.9% through 2035. Liquid cargo dominates because transporting petroleum, chemicals, and other bulk liquids via inland waterways and coastal barge routes remains critical for global trade, energy supply, and industrial activities. The high commercial value, steady demand, and strict regulatory handling requirements ensure that barge fleets are consistently utilized by shipping companies and logistics providers.

The intracoastal transportation segment accounted for 60% share in 2025 and is projected to grow at a CAGR of 2.7% through 2035. Intracoastal routes support high-volume cargo movement between ports, industrial hubs, and commercial centers, handling bulk liquids, petroleum products, chemicals, and containerized goods. Operators are standardizing vessel operations, safety protocols, and cargo handling to ensure reliable, efficient, and compliant transport along these corridors.

US Barge Transportation Market held an 83% share, generating USD 38.3 billion in 2025. The region benefits from a mature inland waterway network, extensive fleet operations, and advanced port infrastructure. Well-developed river systems, fleet management adoption, and predictive maintenance technologies strengthen North America's leadership in safe, high-capacity barge transportation.

Key players operating in the Global Barge Transportation Market include Kirby Corporation, Cargill Marine & Terminal, American Commercial Barge Line, Marquette Transportation, McAllister Towing & Transportation, CMA CGM Group, Contargo, SEACOR, Rhenus Group, and Ingram Barge Company. Companies in the barge transportation market are employing multiple strategies to enhance their presence and strengthen their market foothold. Operators are investing in fleet modernization and adopting predictive maintenance solutions to maximize uptime and minimize operational costs. Integration of IoT, telematics, and automated navigation systems improves fuel efficiency, route optimization, and cargo monitoring. Strategic partnerships with logistics providers, port authorities, and industrial clients help expand route coverage and operational reach. Firms are focusing on specialized vessels for liquid and bulk cargo, compliance with safety and environmental regulations, and sustainability initiatives to gain a competitive edge.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Cargo

- 2.2.3 Barge Fleet

- 2.2.4 Barging Activity

- 2.2.5 Size

- 2.2.6 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for inland waterway transport

- 3.2.1.2 Fleet modernization and digitalization

- 3.2.1.3 Regulatory support for sustainable transport

- 3.2.1.4 Expansion of trade corridors

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High operational and maintenance costs

- 3.2.2.2 Infrastructure limitations

- 3.2.3 Market opportunities

- 3.2.3.1 Green and hybrid propulsion technologies

- 3.2.3.2 Predictive maintenance and AI-driven fleet management

- 3.2.3.3 Intermodal & containerized transport

- 3.2.3.4 Advanced predictive maintenance services

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.: EPA, U.S. Coast Guard, Clean Water Act, NTSB

- 3.4.1.2 Canada: Transport Canada, CMVSS 305

- 3.4.2 Europe

- 3.4.2.1 Germany: BMDV, Euro 6/7

- 3.4.2.2 France: Ministry of Transport, Euro 6/7

- 3.4.2.3 UK: Department for Transport, Euro 6/7

- 3.4.2.4 Italy: Ministry of Infrastructure & Transport

- 3.4.3 Asia Pacific

- 3.4.3.1 China: MIIT, China 6/7 Standards

- 3.4.3.2 Japan: MLIT, JIS Emission Regulations

- 3.4.3.3 South Korea: MOLIT, KS Emission Standards

- 3.4.3.4 India: MoRTH, BS6 Norms

- 3.4.4 Latin America

- 3.4.4.1 Brazil: DENATRAN, CONAMA Standards

- 3.4.4.2 Mexico: Ministry of Communications & Transport, NOM Emission Regulations

- 3.4.5 Middle East and Africa

- 3.4.5.1 UAE: RTA, ESMA Emission Regulations

- 3.4.5.2 Saudi Arabia: Ministry of Transport, SASO Emission Standards

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and Environmental Aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Use case scenarios

- 3.13 Inland Waterway Infrastructure & Capacity Assessment

- 3.14 Intermodal Connectivity & Modal Shift Dynamics

- 3.15 Fleet Age Profile & Replacement Cycle Analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Cargo, 2022 - 2035 ($Bn, Million tons)

- 5.1 Key trends

- 5.2 Liquid Cargo

- 5.3 Gaseous Cargo

- 5.4 Dry Cargo

Chapter 6 Market Estimates & Forecast, By Barge Fleet, 2022 - 2035 ($Bn, Million tons)

- 6.1 Key trends

- 6.2 Covered Barge

- 6.3 Opened Barge

- 6.4 Tank Barge

Chapter 7 Market Estimates & Forecast, By Barging Activity, 2022 - 2035 ($Bn, Million tons)

- 7.1 Key trends

- 7.2 Intracoastal Transportation

- 7.3 Inland Water Transport

Chapter 8 Market Estimates & Forecast, By Size, 2022 - 2035 ($Bn, Million tons)

- 8.1 Key trends

- 8.2 140ft to 180ft

- 8.3 195ft to 250ft

- 8.4 260ft to 300ft

- 8.5 300ft and above

Chapter 9 Market Estimates & Forecast, By Application , 2022 - 2035 ($Bn, Million tons)

- 9.1 Key trends

- 9.2 Coal

- 9.3 Crude & Petroleum Products

- 9.4 Liquid Chemicals

- 9.5 Food Pulp & Other Liquid

- 9.6 Agricultural Products

- 9.7 Metal Ores and Fabricated Metal Products

- 9.8 Pharmaceuticals

- 9.9 Dry & Gaseous Chemicals

- 9.10 LPG, CNG, and Other Gaseous Products

- 9.11 Electronics & Digital Equipment

- 9.12 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Million tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Belgium

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 Singapore

- 10.4.6 South Korea

- 10.4.7 Vietnam

- 10.4.8 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Global Player

- 11.1.1 American Commercial Barge Line

- 11.1.2 Cargill Marine & Terminal

- 11.1.3 CMA CGM

- 11.1.4 Contargo

- 11.1.5 Ingram Barge

- 11.1.6 Kirby

- 11.1.7 Marquette Transportation

- 11.1.8 McAllister Towing & Transportation

- 11.1.9 Rhenus

- 11.1.10 SEACOR

- 11.2 Regional Player

- 11.2.1 HGK Shipping

- 11.2.2 Danser

- 11.2.3 Argosy International

- 11.2.4 Blessey Marine Services

- 11.2.5 Ergon

- 11.2.6 Haeger and Schmidt Logistics

- 11.2.7 Heartland Barge Management

- 11.2.8 Livingston International

- 11.2.9 Maritime

- 11.2.10 Waalhaven