PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019159

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019159

Ultrasonic Cooling Meters Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

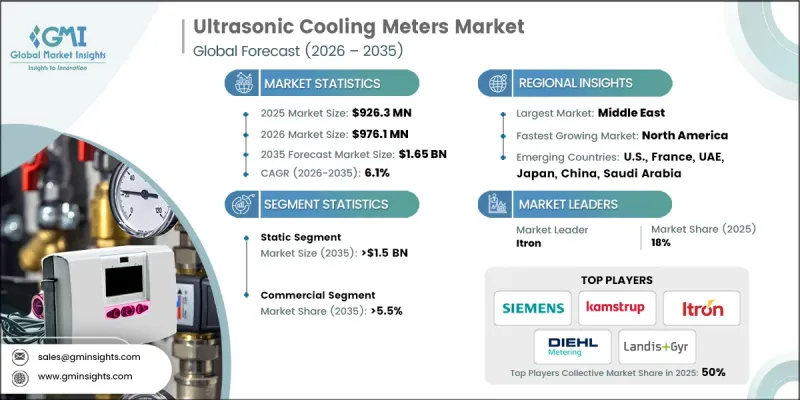

The Global Ultrasonic Cooling Meters Market was valued at USD 926.3 million in 2025 and is estimated to grow at a CAGR of 6.1% to reach USD 1.65 billion by 2035.

The market expansion is fueled by increasing demand for energy-efficient cooling solutions in commercial, industrial, and residential systems. Ultrasonic cooling meters provide precise measurement of energy usage in water- or liquid-based cooling systems by transmitting and receiving sound waves, enabling operators to optimize energy consumption and reduce operational costs. Governments' stringent energy efficiency regulations and building energy codes are driving adoption, as these devices ensure compliance with reporting and efficiency standards. Integration with smart metering platforms allows real-time monitoring and remote data access, supporting IoT-enabled building management systems. Rapid urbanization, digitalization, and the adoption of district cooling systems in developing regions are also creating significant growth opportunities. As organizations and municipalities aim to reduce carbon footprints and improve sustainability, ultrasonic cooling meters have become central to energy management strategies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $926.3 Million |

| Forecast Value | $1.65 Billion |

| CAGR | 6.1% |

The static ultrasonic cooling meters segment is expected to reach USD 1.5 billion by 2035, driven by their high accuracy in measuring flow and energy consumption, which is critical for district cooling applications. Precision is essential because even minor inaccuracies can lead to significant financial losses and operational inefficiencies. Static meters offer superior reliability and longer operational life compared to mechanical alternatives, providing consistent and accurate data over extended periods. These advantages make them ideal for large-scale installations requiring precise monitoring, supporting the market's robust growth trajectory.

The commercial segment is projected to grow at a 5.5% CAGR through 2035. Cooling systems constitute a major portion of energy expenditure in commercial buildings, and ultrasonic cooling meters provide precise data to optimize HVAC performance, reduce energy wastage, and lower operating costs. Their deployment in energy audits helps identify system inefficiencies, enabling equipment upgrades or adjustments to enhance overall energy performance. Integration into smart building platforms further amplifies their value by enabling automated control, data-driven decision-making, and continuous performance monitoring, strengthening the adoption of these meters across commercial infrastructure.

U.S. Ultrasonic Cooling Meters Market is expected to reach USD 425 million by 2035. Growth in the region is supported by strict energy efficiency regulations and the enforcement of building codes that mandate accurate metering in commercial and residential projects. Integration with smart building management systems allows facility managers to monitor energy consumption in real time, optimize system performance, and implement automated controls. Additionally, the rise of IoT technologies has accelerated the adoption of smart meters, including ultrasonic cooling meters, enhancing operational efficiency and energy savings. This focus on energy optimization and sustainability continues to drive robust market growth across the United States.

Prominent players in the Global Ultrasonic Cooling Meters Market include Kamstrup A/S, Itron Inc., Landis+Gyr, Schneider Electric, Axioma Metering, BMETERS Srl, Sontex SA, Zelsius GmbH, ZENNER International GmbH & Co. KG, Danfoss, Techem GmbH, Honeywell International Inc., Engelmann Sensor GmbH, Secure Meters Ltd., Diehl Stiftung & Co. KG, Ista Energy Solutions, Siemens AG, and QUNDIS GmbH. These companies focus on innovation, reliability, and digital integration to drive growth and maintain a competitive advantage. Companies operating in the Ultrasonic Cooling Meters Market are leveraging strategies such as technological innovation, strategic partnerships, and enhanced service offerings to solidify their market position. Key initiatives include developing advanced ultrasonic sensors with improved accuracy and reliability, integrating meters with smart building and IoT platforms, and offering turnkey solutions with installation, calibration, and maintenance support. Firms are also pursuing partnerships with HVAC contractors, utilities, and energy management companies to expand market reach. Emphasis on R&D for cost-effective, energy-efficient, and durable meters strengthens competitiveness, while geographic expansion and participation in sustainability programs enhance brand presence.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & Confidence Scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates & calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Technology trends

- 2.4 Application trends

- 2.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis

- 3.8 Price trend analysis, 2022-2035

- 3.8.1 By Application

- 3.8.2 By Region

- 3.9 Emerging opportunities & trends

- 3.9.1 Digitalization & IoT integration

- 3.10 Investment analysis & future outlook

Chapter 4 Competitive landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans & funding

Chapter 5 Market Size and Forecast, By Technology, 2022 - 2035 (USD Million & MW)

- 5.1 Key trends

- 5.2 Mechanical

- 5.3 Static

Chapter 6 Market Size and Forecast, By Application, 2022 - 2035 (USD Million & MW)

- 6.1 Key trends

- 6.2 Residential

- 6.3 Commercial

- 6.3.1 College/University

- 6.3.2 Office Building

- 6.3.3 Government Building

- 6.3.4 Others

- 6.4 Industrial

Chapter 7 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & MW)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 Poland

- 7.3.3 Sweden

- 7.3.4 Italy

- 7.3.5 France

- 7.3.6 Finland

- 7.3.7 Austria

- 7.3.8 Norway

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 South Korea

- 7.4.4 Singapore

- 7.5 Middle East

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 Oman

- 7.5.5 Kuwait

Chapter 8 Company Profiles

- 8.1 Axioma Metering

- 8.2 BMETERS Srl

- 8.3 Diehl Stiftung & Co. KG

- 8.4 Danfoss

- 8.5 Engelmann Sensor GmbH

- 8.6 Honeywell International Inc.

- 8.7 Ista Energy Solutions

- 8.8 Itron Inc.

- 8.9 Kamstrup A/S

- 8.10 Landis+Gyr

- 8.11 QUNDIS GmbH

- 8.12 Secure Meters Ltd.

- 8.13 Schneider Electric

- 8.14 Siemens AG

- 8.15 Sontex SA

- 8.16 Techem GmbH

- 8.17 Wasion Group

- 8.18 Zenner International GmbH & Co. KG

- 8.19 Zelsius GmbH

- 8.20 Diehl Metering