PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038317

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038317

Hopper Railcar Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

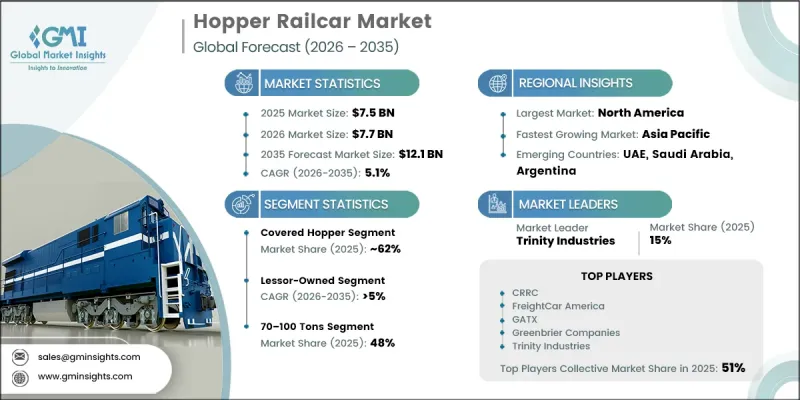

The Global Hopper Railcar Market was valued at USD 7.5 billion in 2025 and is estimated to grow at a CAGR of 5.1% to reach USD 12.1 billion by 2035.

Strong growth in bulk commodity movement continues to drive demand for efficient rail solutions tailored for large-volume handling. Hopper railcars are increasingly favored for their ability to streamline loading processes, minimize material loss, and enhance operational turnaround compared to alternative transport modes. Expanding trade routes and logistics networks are contributing to the steady procurement of both new units and replacement fleets across international markets. Technological upgrades, including lighter materials, higher load-bearing capabilities, and digital monitoring systems, are improving efficiency and reducing long-term operating costs. Leasing models are gaining traction as they offer financial flexibility while enabling access to modern equipment. In parallel, policy initiatives encouraging modal shifts from road to rail are supporting market expansion by emphasizing environmental sustainability, reduced congestion, and cost-effective long-haul transportation. Investments in rail infrastructure and freight corridors are further strengthening supply chain efficiency and encouraging broader industrial adoption of hopper railcars.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.5 Billion |

| Forecast Value | $12.1 Billion |

| CAGR | 5.1% |

The covered hopper segment accounted for 62% share in 2025 and is anticipated to grow at a CAGR of 4.5% through 2035. Increasing demand for transporting sensitive bulk materials has fueled the need for enclosed railcars that protect against environmental exposure and contamination. Industries handling processed goods and export shipments are placing higher emphasis on maintaining product integrity during transit. Additionally, the movement of dry industrial inputs that require controlled environments has supported the continued adoption of covered hopper designs. These railcars also enable more precise unloading mechanisms, reducing material waste and operational inefficiencies.

The lessor-owned fleets segment held 47% share in 2025 and is forecast to grow at a CAGR of 5% between 2026 and 2035. The significant capital investment required for purchasing new railcars has led many operators to prefer leasing arrangements as a more flexible and cost-efficient alternative. Leasing provides access to updated equipment without large upfront expenditures, allowing companies to maintain liquidity and adapt to changing market conditions. Demand fluctuations across industries have further reinforced the appeal of leasing, as it allows businesses to scale capacity based on operational needs without the risk of asset underutilization.

U.S. Hopper Railcar Market accounted for 89% share of USD 2.4 billion in 2025. The country's extensive freight rail infrastructure continues to support high demand for bulk transportation solutions. Strong network connectivity enables efficient long-distance movement, sustaining consistent requirements for fleet modernization and expansion. Large-scale agricultural output remains a key contributor to hopper railcar utilization, with recurring seasonal cycles driving ongoing demand for optimized transport capacity and advanced handling equipment.

Key companies operating in the Global Hopper Railcar Market include BESCO, CRRC, FreightCar America, GATX Corporation, Greenbrier Companies, Jekay International, National Steel Car, Touax Texmaco, Trinity Industries, and VTG. Companies in the Hopper Railcar Market are strengthening their position through a combination of innovation, strategic partnerships, and asset optimization. Manufacturers are focusing on developing lightweight and high-capacity railcars integrated with advanced telematics and predictive maintenance technologies to enhance performance and reduce lifecycle costs. Leasing firms are expanding their fleets to meet rising demand while offering flexible contract structures to attract a broader customer base. Market players are also investing in geographic expansion and collaborations with logistics providers to improve service reach and efficiency. Additionally, continuous upgrades to existing fleets and emphasis on sustainability are helping companies align with regulatory requirements and evolving customer expectations.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.2 Sources, by region

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Load Capacity

- 2.2.4 Material Transported

- 2.2.5 Ownership

- 2.2.6 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for bulk commodity transportation

- 3.2.1.2 Expansion of rail freight networks

- 3.2.1.3 Growth in agricultural exports

- 3.2.1.4 Technological advancements in railcar design

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High capital investment

- 3.2.2.2 Volatility in commodity demand

- 3.2.2.3 Maintenance and lifecycle costs

- 3.2.2.4 Competition from alternative transport modes

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in emerging economies

- 3.2.3.2 Modernization of freight rail fleets

- 3.2.3.3 Digitalization and smart railcars

- 3.2.3.4 Expansion of mining and construction sectors

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Environmental Protection Agency (EPA) Rail Emission Standards

- 3.4.1.2 Federal Railroad Administration (FRA) Safety Compliance Regulations

- 3.4.1.3 Pipeline and Hazardous Materials Safety Administration (PHMSA) Freight Transport Rules

- 3.4.1.4 Occupational Safety and Health Administration (OSHA) Rail Yard Safety Standards

- 3.4.1.5 Transport Canada Rail Safety Act Requirements

- 3.4.2 Europe

- 3.4.2.1 European Union Railway Safety Directive

- 3.4.2.2 Technical Specifications for Interoperability (TSI) Rail Freight Standards

- 3.4.2.3 European Chemicals Agency (ECHA) Cargo Handling Regulations

- 3.4.2.4 European Railway Agency (ERA) Operational Compliance Framework

- 3.4.2.5 National Rail Freight Certification Requirements

- 3.4.3 Asia Pacific

- 3.4.3.1 China State Railway Group Freight Wagon Standards

- 3.4.3.2 Indian Railways Rolling Stock Safety and Design Codes

- 3.4.3.3 Japan Railway Technical Service Standards (JRTS)

- 3.4.3.4 ASEAN Rail Transport Harmonization Guidelines

- 3.4.3.5 Australian Rail Track Corporation (ARTC) Freight Compliance Standards

- 3.4.4 Latin America

- 3.4.4.1 Brazil National Land Transport Agency (ANTT) Rail Freight Regulations

- 3.4.4.2 Brazilian Rail Safety and Interoperability Standards

- 3.4.4.3 Mexico Federal Railway Transport Agency Norms

- 3.4.4.4 Regional Rail Infrastructure Certification Requirements

- 3.4.4.5 Andean Community Rail Freight Transport Guidelines

- 3.4.5 Middle East & Africa

- 3.4.5.1 GCC Railway Authority Freight Wagon Standards

- 3.4.5.2 Saudi Railway Company (SAR) Operational Regulations

- 3.4.5.3 Saudi Standards, Metrology and Quality Organization (SASO) Rail Compliance

- 3.4.5.4 South African Rail Safety Regulator (RSR) Standards

- 3.4.5.5 African Railway Union Freight Transport Guidelines

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price analysis (Driven by Primary Research)

- 3.8.1 Historical Price Trend Analysis

- 3.8.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.9 Trade data analysis (Driven by Paid Research)

- 3.9.1 Import/export volume & value trends

- 3.9.2 Key trade corridors & tariff impact

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis (Driven by Primary Research)

- 3.12 Impact of AI & generative AI on the market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 GenAI use cases & adoption roadmap by segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Capacity & production landscape (Driven by Primary Research)

- 3.13.1 Installed capacity by region & key producer

- 3.13.2 Capacity utilization rates & expansion pipelines

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly Initiatives

- 3.14.5 Carbon footprint considerations

- 3.15 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.15.1 Base Case - key macro & industry variables driving CAGR

- 3.15.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.15.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Product, 2022 - 2035 ($Mn, Fleet Size)

- 5.1 Key trends

- 5.2 Covered hopper

- 5.3 Open-top hopper

Chapter 6 Market Estimates & Forecast, By Load Capacity, 2022 - 2035 ($Mn, Fleet Size)

- 6.1 Key trends

- 6.2 Below 70 Tons

- 6.3 70-100 Tons

- 6.4 Above 100 Tons

Chapter 7 Market Estimates & Forecast, By Material Transported, 2022 - 2035 ($Mn, Fleet Size)

- 7.1 Key trends

- 7.2 Coal

- 7.3 Grain

- 7.4 Cement

- 7.5 Aggregates & Sand

- 7.6 Minerals & Ores

- 7.7 Fertilizers

- 7.8 Chemicals

- 7.9 Others

Chapter 8 Market Estimates & Forecast, By Ownership, 2022 - 2035 ($Mn, Fleet Size)

- 8.1 Key trends

- 8.2 Lessor-Owned

- 8.3 Railroad-Owned

- 8.4 Shipper-Owned

- 8.5 Pool/Shared Fleet

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn, Fleet Size)

- 9.1 Key trends

- 9.2 Mining

- 9.3 Agriculture

- 9.4 Construction Materials

- 9.5 Industrial Manufacturing

- 9.6 Energy & Utilities

- 9.7 Chemicals & Fertilizers

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Fleet Size)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Southeast Asia

- 10.4.6 ANZ

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Argentina

- 10.5.3 Mexico

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 CRRC

- 11.1.2 FreightCar America

- 11.1.3 GATX

- 11.1.4 Procor

- 11.1.5 Texmaco Rail & Engineering

- 11.1.6 Greenbrier Companies

- 11.1.7 Touax

- 11.1.8 Trinity Industries

- 11.1.9 VTG

- 11.2 Regional Players

- 11.2.1 BESCO

- 11.2.2 Everest Railcar Services

- 11.2.3 Jekay International

- 11.2.4 National Steel Car

- 11.2.5 Pacific Railcar Leasing

- 11.2.6 Railcar Leasing & Logistics

- 11.2.7 RESIDCO

- 11.2.8 TCIX Rail

- 11.2.9 Union Pacific Railroad

- 11.3 Emerging Players

- 11.3.1 Creative Railcar Marketing Services

- 11.3.2 Rapido Trains

- 11.3.3 Southwest Rail Industries