PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038482

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038482

Cars Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

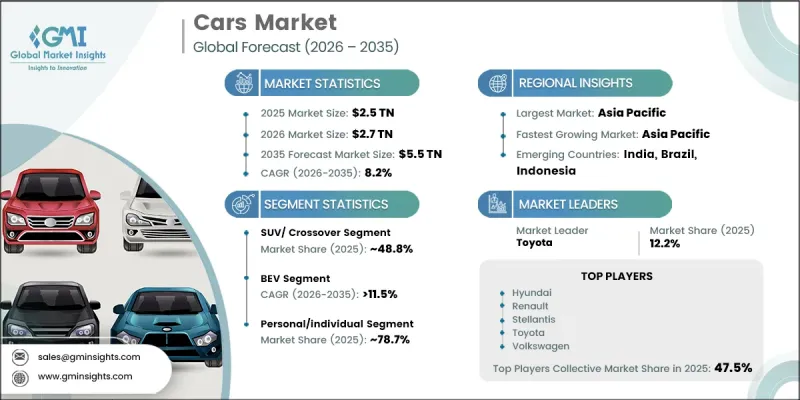

The Global Cars Market was valued at USD 2.5 trillion in 2025 and is estimated to grow at a CAGR of 8.2% to reach USD 5.5 trillion by 2035.

Market growth is driven by rising global urbanization, increasing disposable incomes, and a steady shift in consumer preference toward personal mobility solutions. Expanding middle-class populations are significantly contributing to higher automobile adoption, particularly as consumers transition away from shared and two-wheeler transport options toward private vehicle ownership. Improved financial capacity is also enabling stronger demand for premium and feature-rich vehicles. At the same time, the automotive sector is undergoing a structural transformation with growing emphasis on electrification and sustainable mobility. Increasing awareness of environmental concerns is accelerating interest in low-emission vehicles, while stricter emission regulations are pushing manufacturers toward cleaner technologies. Continuous innovation in vehicle design, safety systems, and connectivity features is further enhancing product appeal. Government-backed incentives and supportive policy frameworks are also playing a key role in accelerating market expansion by encouraging the adoption of advanced mobility solutions across both developed and emerging economies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.5 Trillion |

| Forecast Value | $5.5 Trillion |

| CAGR | 8.2% |

The SUV and crossover segment held a 48.8% share, generating USD 1.2 trillion in 2025. Demand continues to shift strongly toward these vehicle types, as they remain the preferred choice for both family and everyday commuting needs. Compact and mid-size models account for the highest sales volumes, while premium variants contribute significantly to overall profitability. Features and technologies initially introduced in high-end models are increasingly being integrated into mid-tier offerings, reshaping consumer expectations across segments and enhancing overall product competitiveness.

The luxury and premium segment is projected to grow at a CAGR of 9.2% from 2026 to 2035. Rising disposable income levels are a major factor supporting this growth, particularly as consumers in developed markets gain greater purchasing power. Increasing financial capacity among middle and upper-middle income groups is driving higher demand for luxury vehicles equipped with advanced performance capabilities and modern technologies. This shift reflects a growing preference for comfort, innovation, and brand value within the automotive sector.

United States Cars Market reached USD 185.3 billion in 2025 and is expected to grow at a CAGR of 8.2% between 2026 and 2035. The country remains one of the largest automotive markets globally, supported by strong consumer demand for both conventional vehicles and electric models. Market expansion is influenced by rising income levels, strong preference for SUVs and pickup vehicles, and increasing adoption of hybrid and electric cars. The transition toward electric mobility is further reinforced by supportive policy measures and incentives aimed at encouraging cleaner transportation solutions.

Key companies operating in the Global Cars Industry include Toyota, Volkswagen, Ford, Hyundai, GM, Honda, BYD, Stellantis, Renault, and Suzuki. Companies in the Global Cars Market are strengthening their competitive position through rapid electrification strategies, investment in advanced vehicle technologies, and expansion of global production capabilities. Automakers are focusing on developing electric and hybrid models to align with tightening emission standards and rising environmental awareness. Strong emphasis is being placed on research and development to enhance battery performance, vehicle range, and autonomous driving features. Strategic partnerships with technology firms are helping accelerate innovation in connected and smart mobility solutions. Manufacturers are also expanding their dealership and distribution networks to improve market reach. Cost optimization, platform sharing, and localized production are being adopted to improve profitability while meeting diverse regional demand patterns across global automotive markets.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Propulsion

- 2.2.4 Vehicle class

- 2.2.5 Transmission

- 2.2.6 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry Impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing disposable income in emerging economies

- 3.2.1.2 Government incentives and subsidies for electric vehicles

- 3.2.1.3 Expansion of ride-sharing and mobility-as-a-service (MaaS)

- 3.2.1.4 Growing middle-class population in the emerging markets

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Supply chain disruptions in automotive components

- 3.2.2.2 High initial cost of electric and advanced vehicles

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in electric and hybrid vehicle adoption

- 3.2.3.2 Development of autonomous vehicle technology

- 3.2.3.3 Expansion of sustainable and green manufacturing practices

- 3.2.1 Growth drivers

- 3.3 Technology trends & innovation ecosystem

- 3.3.1 Current technologies

- 3.3.1.1 Powertrain technology

- 3.3.1.2 ADAS & safety technology

- 3.3.1.3 Connectivity & infotainment system

- 3.3.2 Emerging technologies

- 3.3.2.1 Next-generation battery technology

- 3.3.2.2 Autonomous driving technology

- 3.3.2.3 Vehicle-to-everything (V2X) communication

- 3.3.1 Current technologies

- 3.4 Growth potential analysis

- 3.5 Pricing Analysis (Driven by Primary Research)

- 3.5.1 Historical Price Trend Analysis

- 3.5.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.1.1 US - Corporate Average Fuel Economy (CAFE) Standards

- 3.6.1.2 US - Clean Air Act Vehicle Emission Standards

- 3.6.1.3 Canada - Transport Canada

- 3.6.2 Europe

- 3.6.2.1 Germany - Euro 6 / Euro 7 Emission Standards

- 3.6.2.2 EU - WLTP (Worldwide Harmonized Light Vehicles Test Procedure)

- 3.6.3 Asia Pacific

- 3.6.3.1 China - New Energy Vehicle (NEV) Mandate Policy

- 3.6.3.2 India - BS-VI Emission Standards

- 3.6.4 Latin America

- 3.6.4.1 Brazil - PROCONVE Emission Control Program

- 3.6.4.2 Mexico - NOM-163 Fuel Economy Standards

- 3.6.5 Middle East & Africa

- 3.6.5.1 Saudi Arabia - SASO Vehicle Safety and Emission Standards

- 3.6.5.2 UAE - Green Vehicle Initiative Regulations

- 3.6.1 North America

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Patent analysis (Driven by Primary Research)

- 3.10 Trade Data Analysis (Driven by Paid Database)

- 3.10.1 Import/Export Volume & Value Trends

- 3.10.2 Key Trade Corridors & Tariff Impact

- 3.11 Capacity & Production Landscape (Driven by Primary Research)

- 3.11.1 Installed Capacity by Region & Key Producer

- 3.11.2 Capacity Utilization Rates & Expansion Pipelines

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon Footprint Considerations

- 3.13 Cost breakdown analysis

- 3.13.1 Direct Material Procurement Cost

- 3.13.2 Production & Assembly Line Cost

- 3.13.3 Labor & Workforce Cost

- 3.13.4 Overhead & Facility Cost

- 3.13.5 Compliance, Quality & Warranty Cost

- 3.14 EV charging infrastructure landscape

- 3.14.1 Public vs Private charging networks

- 3.14.2 Charging speed technology evolution

- 3.14.3 Home charging solutions & adoption barriers

- 3.14.4 Workplace & destination charging growth

- 3.15 Impact of AI & Generative AI on the Market

- 3.15.1 AI-driven disruption of existing business models

- 3.15.2 GenAI use cases & adoption roadmap by segment

- 3.15.3 Risks, limitations & regulatory considerations

- 3.16 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.16.1 Base Case - key macro & industry variables driving CAGR

- 3.16.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.16.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Vehicle, 2022- 2035 ($Bn, Thousand Units)

- 5.1 Key trends

- 5.2 Hatchback

- 5.3 Sedan

- 5.4 SUV/ Crossover

- 5.5 Coupe

- 5.6 MPV

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Propulsion, 2022- 2035 ($Bn, Thousand Units)

- 6.1 Key trends

- 6.2 Internal Combustion Engine (ICE)

- 6.3 Hybrid Electric Vehicles (HEV)

- 6.4 Battery Electric Vehicles (BEV)

- 6.5 Fuel Cell Electric Vehicles (FCEV)

- 6.6 Plug-in Hybrid Electric Vehicles (PHEV)

Chapter 7 Market Estimates & Forecast, By Vehicle class, 2022- 2035 ($Bn, Thousand Units)

- 7.1 Key trends

- 7.2 Economy/Entry level

- 7.3 Mid-range

- 7.4 Luxury/Premium

Chapter 8 Market Estimates & Forecast, By Transmission, 2022- 2035 ($Bn, Thousand Units)

- 8.1 Key trends

- 8.2 Manual Transmission

- 8.3 Automatic Transmission

Chapter 9 Market Estimates & Forecast, By End Use, 2022- 2035 ($Bn, Thousand Units)

- 9.1 Key trends

- 9.2 Personal/Individual Use

- 9.3 Commercial

- 9.3.1 Corporate fleet

- 9.3.2 Rental car services

- 9.3.3 Corporate fleet

- 9.3.4 Government/public sector fleet

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Netherlands

- 10.3.7 Sweden

- 10.3.8 Poland

- 10.3.9 Belgium

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Indonesia

- 10.4.7 Thailand

- 10.4.8 Malaysia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Chile

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Toyota Motor

- 11.1.2 Volkswagen

- 11.1.3 Hyundai Motor

- 11.1.4 Ford Motor

- 11.1.5 General Motors (GM)

- 11.1.6 Stellantis

- 11.1.7 Honda Motor

- 11.1.8 Renault

- 11.1.9 BMW

- 11.1.10 Mercedes-Benz

- 11.2 Regional players

- 11.2.1 Maruti Suzuki

- 11.2.2 Tata Motors Passenger Vehicles

- 11.2.3 Mahindra & Mahindra

- 11.2.4 SAIC Motor

- 11.2.5 BAIC

- 11.2.6 Tesla

- 11.2.7 Chery Automobile

- 11.3 Emerging players

- 11.3.1 BYD Auto

- 11.3.2 XPeng

- 11.3.3 Li Auto