PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038652

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2038652

Asia Pacific Energy as a Service (EaaS) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

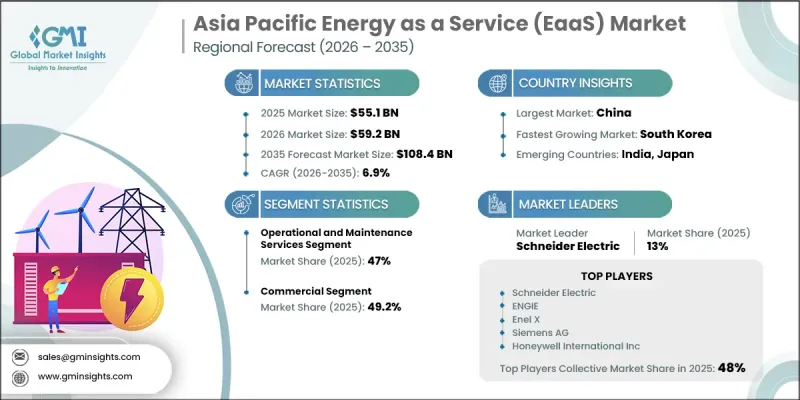

Asia-Pacific Energy as a Service Market was valued at USD 55.1 billion in 2025 and is estimated to grow at a CAGR of 6.9% to reach USD 108.4 billion by 2035.

The Asia Pacific energy as a service industry is gaining strong traction as commercial and industrial users increasingly shift toward flexible, service-driven energy solutions instead of owning infrastructure assets. Organizations are prioritizing financial efficiency as fluctuating electricity costs, rising borrowing rates, and uncertain technology lifespans reduce the appeal of large upfront investments. Energy as a Service transforms capital-intensive projects into predictable operating expenses while transferring performance accountability and maintenance responsibilities to service providers. Regulatory momentum across the region is also accelerating adoption, with governments enforcing stricter efficiency standards and promoting outcome-based energy models. The growing integration of distributed energy resources, including decentralized power systems and advanced energy management technologies, further supports this transition. These systems require continuous monitoring, optimization, and coordination, capabilities often managed more effectively by specialized providers. As operational complexity increases, outsourced energy solutions are becoming essential, enabling improved system reliability, efficiency, and scalability across diverse end-use sectors.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $55.1 Billion |

| Forecast Value | $108.4 Billion |

| CAGR | 6.9% |

The energy supply service segment is expected to grow at a CAGR of 6.6% through 2035, reinforcing its importance within the Asia-Pacific Energy as a Service Market. This segment is gaining momentum as organizations seek reliable and uninterrupted energy delivery across large-scale developments and operational facilities. Service providers are offering structured power supply agreements with defined performance metrics, helping customers mitigate risks associated with supply disruptions and market volatility. The ability to ensure consistent energy availability while reducing procurement uncertainties is driving strong demand for these services across the region.

The utility sector is anticipated to grow at a CAGR of 8.8% through 2035, highlighting its growing role in the Asia-Pacific energy as a service industry. Utilities are increasingly adopting service-based models as the deployment of aggregated distributed energy systems continues to rise. The management of these decentralized assets requires advanced coordination, monitoring, and performance optimization, leading utilities to collaborate with specialized service providers. This shift is supporting more efficient energy distribution and improved system performance, contributing to overall market growth.

China Energy as a Service Market is expected to reach USD 90.1 billion by 2035. Rapid industrial electrification is driving demand for reliable and efficient energy solutions, particularly in high-growth manufacturing sectors that require uninterrupted power and utility services. Service-based energy models enable organizations to secure consistent performance outcomes without the burden of infrastructure ownership. The focus on operational efficiency and energy reliability continues to support widespread adoption across industrial environments.

Key companies operating in the Asia-Pacific Energy as a Service Market include ABB Ltd, Siemens AG, Schneider Electric, Mitsubishi Electric, Hitachi Energy, Honeywell International Inc., Johnson Controls, ENGIE, Enel X, Veolia Energy, Tata Power, Sembcorp Industries, Keppel Corporation, Aggreko, Cleantech Solar, Amplus Solar, Ampotech, BECIS, Energy Capital Global (ECG), and KJTS Group Berhad. Companies in Asia-Pacific Energy as a Service Market are strengthening their competitive position through strategic investments in digital energy platforms, advanced analytics, and integrated service offerings. They are focusing on long-term service contracts that ensure predictable revenue streams while delivering measurable performance outcomes for clients. Partnerships with industrial players, utilities, and infrastructure developers are enabling broader market reach and improved service capabilities. Firms are also expanding their portfolios to include renewable energy integration, energy storage, and smart grid solutions to meet evolving customer needs. Operational efficiency is being enhanced through automation and data-driven monitoring systems.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Type trends

- 2.4 End use trends

- 2.5 Country trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.1.1 Technology provider

- 3.1.2 Equipment manufacturers

- 3.1.3 Digital solution providers

- 3.1.4 Financial enablers

- 3.1.5 Policy & regulatory bodies

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of energy as a service

- 3.8 Impact of AI & generative AI on the market [SOLUTION CORE]

- 3.8.1 Predictive maintenance & fault detection

- 3.8.2 Grid Optimization & Load Forecasting

- 3.8.3 Digital twin simulation & testing

- 3.8.4 Risks, limitations & regulatory considerations

- 3.9 Emerging opportunities & trends

- 3.9.1 Digitalization & IoT integration

- 3.9.2 Emerging market penetration

- 3.10 Investment analysis and future outlook

Chapter 4 Competitive landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by country, 2025

- 4.2.1 China

- 4.2.2 South Korea

- 4.2.3 India

- 4.2.4 Japan

- 4.3 Competitive benchmarking

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans and funding

Chapter 5 Market Size and Forecast, By Type, 2022 - 2035 (USD Billion)

- 5.1 Key trends

- 5.2 Energy supply service

- 5.3 Operational and maintenance services

- 5.4 Energy efficiency and optimization services

Chapter 6 Market Size and Forecast, By End use, 2022 - 2035 (USD Billion)

- 6.1 Key trends

- 6.2 Residential

- 6.3 Commercial

- 6.4 Industrial

- 6.5 Utility

Chapter 7 Market Size and Forecast, By Country, 2022 - 2035 (USD Billion)

- 7.1 Key trends

- 7.2 China

- 7.3 South Korea

- 7.4 India

- 7.5 Japan

Chapter 8 Company Profiles

- 8.1 ABB Ltd

- 8.2 Aggreko

- 8.3 Amplus Solar

- 8.4 Ampotech

- 8.5 BECIS

- 8.6 Cleantech Solar

- 8.7 Enel X

- 8.8 ENGIE

- 8.9 Energy Capital Global (ECG)

- 8.10 Hitachi Energy

- 8.11 Honeywell International Inc

- 8.12 Johnson Controls

- 8.13 Keppel Corporation

- 8.14 KJTS Group Berhad

- 8.15 Mitsubishi Electric

- 8.16 Schneider Electric

- 8.17 Sembcorp Industries

- 8.18 Siemens AG

- 8.19 Tata Power

- 8.20 Veolia Energy