PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045685

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045685

Asia-Pacific Mobile Accessories Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

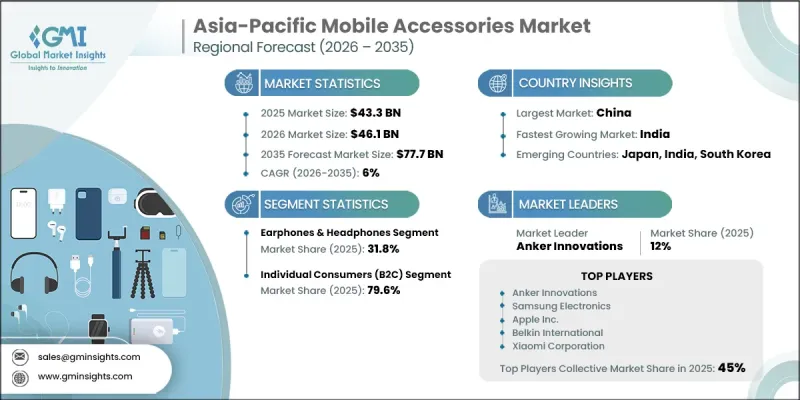

Asia-Pacific Mobile Accessories Market was valued at USD 43.3 billion in 2025 and is estimated to grow at a CAGR of 6% to reach USD 77.7 billion by 2035.

Growth across the Asia-Pacific mobile accessories industry continues to accelerate as smartphone penetration rises and consumers increasingly invest in products that improve device functionality, convenience, and durability. Rising disposable incomes across developed and developing economies are encouraging consumers to purchase premium-quality accessories that complement their digital lifestyles. The growing preference for advanced charging technologies and smart connectivity solutions is also encouraging manufacturers to introduce innovative products tailored to evolving consumer expectations. In addition, the rapid expansion of online retail channels has strengthened product accessibility and market visibility for both established brands and emerging companies operating in the mobile accessories market. Features such as user reviews, product comparisons, and detailed specifications have significantly improved the online shopping experience, further supporting market demand. Another major factor driving industry expansion is the growing emphasis on sustainable, durable materials, as consumers continue to prioritize long-lasting, high-performance mobile accessories.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $43.3 Billion |

| Forecast Value | $77.7 Billion |

| CAGR | 6% |

The earphones and headphones segment held a 31.8% share, reaching USD 13.7 billion in 2025. Demand for these products continues to rise as consumers prioritize superior sound performance, wireless functionality, and advanced audio technologies. The growing popularity of true wireless audio devices has significantly contributed to segment expansion, particularly among users seeking enhanced entertainment and communication experiences. Consumers are increasingly choosing premium audio accessories that deliver convenience, mobility, and improved sound quality for everyday device usage.

The individual consumers segment held a 79.6% share in 2025 with USD 34.4 billion. Strong demand from smartphone users for products related to device protection, charging efficiency, personalization, and entertainment continues to drive this segment forward. Consumers increasingly seek accessories that align with their daily routines, style preferences, and performance expectations. The market also reflects rising demand for a broad range of products, spanning affordable options to technologically advanced premium accessories designed for enhanced user experiences.

China Mobile Accessories Market held a 11.8% share, generating USD 5.1 billion in 2025. China's dominance in the regional market is supported by its extensive smartphone user base, strong domestic consumption, and expanding middle-class population with increasing spending power. The country also benefits from a well-established manufacturing ecosystem and growing consumer preference for high-quality mobile accessories. Demand for technologically advanced and premium products continues to rise as consumers increasingly value convenience, wireless compatibility, and product quality. Frequent smartphone replacement cycles and strong adoption of upgraded mobile technologies continue to create sustained opportunities for accessory manufacturers across the Chinese market.

Key companies operating in the Asia-Pacific Mobile Accessories Market include Anker Innovations, Apple Inc., Aukey Technology, Baseus, Belkin International, Huawei Technologies, OPPO, Portronics, Remax, Rock Space, Samsung Electronics, Sony Corporation, Spigen Inc., UGREEN Group, and Xiaomi Corporation. Companies operating in the Asia-Pacific mobile accessories market are focusing on several strategic initiatives to strengthen their market position and expand their customer base. Leading manufacturers are increasing investments in product innovation, particularly in wireless technologies, fast-charging solutions, and premium audio accessories to address changing consumer preferences. Many companies are also expanding their online retail presence through partnerships with major e-commerce platforms to improve product accessibility and brand visibility. Businesses are emphasizing sustainable manufacturing practices and durable materials to attract environmentally conscious consumers. In addition, brands are introducing diversified product portfolios across multiple price ranges to target both budget-conscious and premium buyers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product Type

- 2.2.2 Compatibility

- 2.2.3 Price Range

- 2.2.4 End-User

- 2.2.5 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing smartphone adoption and device upgrade cycles

- 3.2.1.2 Rising demand for wireless and fast-charging solutions

- 3.2.1.3 Innovation in audio technology and protective materials

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 Competition from low-cost alternatives and counterfeit products

- 3.2.2.2 Rising raw material costs and supply chain complexities

- 3.2.3 Opportunities

- 3.2.3.1 Expansion of online retail and direct-to-consumer channels

- 3.2.3.2 Integration of smart features and sustainability

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing Analysis (Driven by Primary Research)

- 3.6.1 Historical Price Trend Analysis (2020-2024) (Driven by Primary Research)

- 3.6.2 Pricing Strategy by Player Type (Premium/Mid-Range/Value) (Driven by Primary Research)

- 3.6.3 Price Comparison: Proprietary Brands vs. Partnership Brands vs. Generic

- 3.6.4 Retailer Margin Structures & Wholesale Pricing Dynamics

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Trade Data Analysis (Driven by Primary Research)

- 3.10.1 Import/Export Volume & Value Trends (2020-2024) (Driven by Primary Research)

- 3.10.2 Key Trade Corridors & Origin Countries (China, Vietnam, South Korea) (Driven by Primary Research)

- 3.10.3 Tariff Impact & Trade Agreement Implications

- 3.11 Impact of AI & Generative AI on the Market

- 3.11.1 AI-Driven Disruption of Existing Business Models

- 3.11.2 GenAI Use Cases & Adoption Roadmap (Smart Assistants in Audio Accessories, Personalized Recommendations)

- 3.11.3 AI-Enabled Features in Next-Gen Accessories (Adaptive Noise Cancellation, Health Monitoring)

- 3.11.4 Risks, Limitations & Regulatory Considerations

- 3.12 Distribution Infrastructure & Channel Penetration Landscape (Driven by Primary Research)

- 3.12.1 Channel Coverage by Region & Format (Modern Trade vs. Traditional Trade) (Driven by Primary Research)

- 3.12.2 Last-Mile Infrastructure Gaps & Emerging Channel Shifts (E-commerce Fulfillment, Dark Stores) (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Earphones & headphones

- 5.3 Chargers & cables

- 5.4 Power bank

- 5.5 Protective cases

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Compatibility, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Universal/Multi-Platform Accessories

- 6.3 iOS-Specific Accessories

- 6.4 Android-Specific Accessories

Chapter 7 Market Estimates & Forecast, By Price Range, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Low (Less than $50)

- 7.3 Mid Range ($50 to $100)

- 7.4 Premium (More than $100)

Chapter 8 Market Estimates & Forecast, By End-User, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Individual Consumers (B2C)

- 8.3 Commercial (B2B)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Online

- 9.2.1 E-commerce

- 9.2.2 Brand Websites

- 9.3 Offline

- 9.3.1 Brand-owned Stores

- 9.3.2 Electronics Retailers

- 9.3.3 Hypermarkets & Supermarkets

- 9.3.4 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 China

- 10.3 Japan

- 10.4 India

- 10.5 South Korea

- 10.6 Indonesia

Chapter 11 Company Profiles

- 11.1 Top Global Player

- 11.1.1 Apple Inc.

- 11.1.2 Samsung Electronics

- 11.1.3 Xiaomi Corporation

- 11.1.4 Anker Innovations

- 11.1.5 Sony Corporation

- 11.1.6 Huawei Technologies

- 11.1.7 OPPO

- 11.1.8 Belkin International

- 11.2 Regional Player

- 11.2.1 Remax

- 11.2.2 Baseus

- 11.2.3 Portronics

- 11.2.4 UGREEN Group

- 11.3 Emerging Players

- 11.3.1 Aukey Technology

- 11.3.2 Spigen Inc.

- 11.3.3 Rock Space