PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061321

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061321

North America Mobile Accessories Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

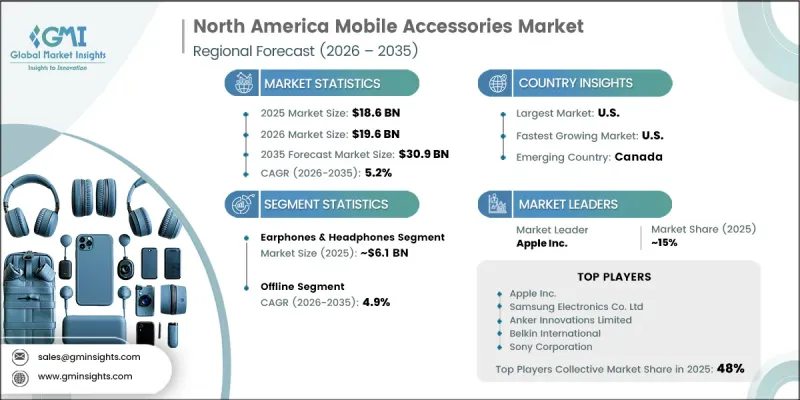

North America Mobile Accessories Market was valued at USD 18.6 billion in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 30.9 billion by 2035.

The market growth is shaped by the rising penetration of smartphones and frequent device upgrade cycles across North America. Consumers increasingly depend on accessories that enhance functionality, improve protection, and elevate overall user experience. Mobile accessories are also viewed as cost-effective solutions that extend device lifespan while improving performance. Growing awareness regarding device safety, charging efficiency, and audio quality continues to stimulate demand across consumer groups. Wireless charging solutions and fast-charging technologies are gaining traction due to convenience and time-saving benefits.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $18.6 Billion |

| Forecast Value | $30.9 Billion |

| CAGR | 5.2% |

Professionals across various industries are also contributing to steady demand, as mobile accessories support both personal and work-related usage needs. The market is further strengthened by evolving lifestyles and rising digital dependence, which require a wide assortment of accessories across retail stores and online platforms. Consumers seek products that protect devices, support efficient charging, and enhance audio experiences. Audio accessories such as earphones and headphones remain widely used for entertainment, communication, and daily activities. Design innovation and ergonomic improvements are enabling users to maximize device utility across different use cases.

The earphones and headphones segment generated USD 6.1 billion in 2025 and is expected to grow at a CAGR of 6% from 2026 to 2035. This segment continues to lead the market due to its essential role in everyday audio consumption, communication, and entertainment. Users rely on audio accessories across multiple scenarios, including travel, fitness activities, work calls, and leisure usage. The category includes a wide variety of products such as wireless earbuds, over-ear designs, in-ear models, and noise-cancelling variants. Continuous innovation in sound quality, battery efficiency, and comfort features is further supporting sustained demand across consumer segments.

The offline distribution channel accounted for 63.6% share in 2025 and is projected to grow at a CAGR of 4.9% from 2026 to 2035. Physical retail continues to dominate due to consumer preference for hands-on evaluation and instant product availability. Brick-and-mortar outlets such as electronics retailers, telecom stores, department stores, and specialized accessory shops provide opportunities for users to assess product compatibility and quality before purchase. In-store experiences allow customers to test accessories directly with their devices, ensuring better decision-making. Retail staff also play an important role in guiding customers through technical specifications and usage requirements.

United States Mobile Accessories Market reached USD 13.8 billion in 2025 and is forecast to grow at a CAGR of 5.7% from 2026 to 2035. Market growth in the U.S. is driven by a large consumer base, strong smartphone adoption, and a growing preference for premium and personalized digital experiences. Consumers across urban and suburban regions actively invest in accessories that support professional productivity, lifestyle convenience, and entertainment needs. Rising awareness about device protection and audio performance continues to drive premium product adoption. A strong retail ecosystem and well-developed e-commerce infrastructure further enhance product accessibility across price segments.

Major companies operating in the North America mobile accessories market include Apple Inc., Samsung Electronics Co., Ltd., Google LLC, Sony Corporation, Bose Corporation, Logitech International, Belkin International, Anker Innovations Limited, OtterBox, Casetify, Mophie, Spigen Inc., UGREEN Group Limited, PopSockets LLC, and JBL. Companies operating in the North America mobile accessories market are adopting strategies such as continuous product innovation, expanding wireless and fast-charging portfolios, and integrating advanced technologies like AI-driven audio enhancements. Many brands are strengthening distribution through omnichannel retail expansion, combining strong e-commerce presence with physical retail partnerships. Strategic collaborations with smartphone manufacturers and telecom operators are helping improve product compatibility and visibility. Firms are also focusing on premiumization through design upgrades, durability improvements, and sustainability-driven materials. Aggressive marketing campaigns and influencer-led promotions are increasing brand engagement.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product Type

- 2.2.2 Compatibility

- 2.2.3 Price Range

- 2.2.4 End-User

- 2.2.5 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing smartphone adoption and device upgrade cycles

- 3.2.1.2 Rising demand for wireless and fast-charging solutions

- 3.2.1.3 Innovation in audio technology and protective materials

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Intense price competition from low-cost manufacturers

- 3.2.2.2 Rapid technology changes requiring frequent product updates

- 3.2.3 Opportunities

- 3.2.3.1 Expansion of sustainable and eco-friendly accessory designs

- 3.2.3.2 Increasing adoption of multi-device charging solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis - North America (Driven by Primary Research)

- 3.6.1 Historical Price Trend Analysis- North America (Driven by Primary Research)

- 3.6.2 Pricing Strategy by Player Type (Premium/Value/Cost-plus) (Driven by Primary Research)

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Trade Data Analysis- North America (Driven by Paid Database)

- 3.10.1 U.S. Import/Export Volume & Value Trends (Driven by Primary Research)

- 3.10.2 Canada Import/Export Volume & Value Trends (Driven by Primary Research)

- 3.10.3 Key Trade Corridors & Tariff Impact (Driven by Primary Research)

- 3.11 Impact of AI & Generative AI on the Market

- 3.11.1 AI-Driven Disruption of Existing Business Models

- 3.11.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.11.3 Risks, Limitations & Regulatory Considerations

- 3.12 Distribution Infrastructure & Channel Penetration Landscape (Driven by Primary Research)

- 3.12.1 Channel Coverage by Region & Format (Modern vs. Traditional Retail) (Driven by Primary Research)

- 3.12.2 Last-Mile Infrastructure Gaps & Emerging Channel Shifts (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 U.S.

- 4.2.2 Canada

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Earphones & headphones

- 5.3 Chargers & cables

- 5.4 Power bank

- 5.5 Protective cases

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Compatibility, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Universal/Multi-Platform Accessories

- 6.3 iOS-Specific Accessories

- 6.4 Android-Specific Accessories

Chapter 7 Market Estimates & Forecast, By Price Range, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Low (Less than $50)

- 7.3 Mid Range ($50 to $100)

- 7.4 Premium (More than $100)

Chapter 8 Market Estimates & Forecast, By End-User, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Individual Consumers (B2C)

- 8.3 Commercial (B2B)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Online

- 9.2.1 E-commerce

- 9.2.2 Brand Websites

- 9.3 Offline

- 9.3.1 Brand-owned Stores

- 9.3.2 Electronics Retailers

- 9.3.3 Hypermarkets & Supermarkets

- 9.3.4 Others

Chapter 10 Market Estimates and Forecast, By Country, 2022 - 2035 (USD Billion) (Thousand Unit)

- 10.1 Key trends

- 10.2 U.S.

- 10.3 Canada

Chapter 11 Company Profiles

- 11.1 Top Global Player

- 11.1.1 Apple Inc.

- 11.1.2 Samsung Electronics Co., Ltd.

- 11.1.3 Anker Innovations Limited

- 11.1.4 Belkin International (Foxconn)

- 11.1.5 Sony Corporation

- 11.2 Regional Player

- 11.2.1 Bose Corporation

- 11.2.2 JBL

- 11.2.3 Google LLC

- 11.2.4 Logitech International

- 11.2.5 OtterBox

- 11.2.6 Mophie

- 11.3 Emerging Players

- 11.3.1 PopSockets LLC

- 11.3.2 UGREEN Group Limited

- 11.3.3 Spigen Inc.

- 11.3.4 Casetify