PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073369

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073369

Mobile Accessories - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

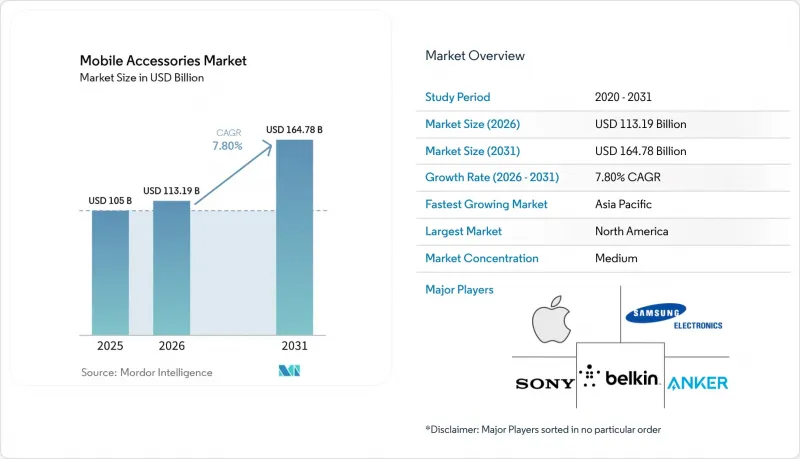

According to Mordor Intelligence, the mobile accessories market size stands at USD 113.19 billion in 2026 and is projected to reach USD 164.78 billion in 2031, advancing at a 7.8% CAGR over the forecast period.

This report is Segmented by Product Type (Headphones/Earbuds, Chargers, Power Banks, Protective Cases, and More), Distribution Channel (Online Retail, Offline Retail, and More), Price Range (Low (Up To USD 20), Mid (USD 21-50), Premium (USD 51 and Above)), Compatibility (Android-Specific, IOS-Specific, and Universal/Multi-platform), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Mobile Accessories Market Trends and Insights

Adoption of GaN Technology Enabling Ultra-Compact Fast Chargers

Gallium-nitride devices switch at frequencies 10-times higher than silicon, allowing designers to shrink magnetic components by 40% while supporting USB Power Delivery 3.1 Extended Power Range up to 240 W. Anker's GaNPrime, launched in 2024, delivers 150 W in a brick 30% smaller than legacy silicon equivalents and captured premium share from bundled chargers. ITU's L.1004 interoperability standard, ratified in 2024, cut certification costs by 20%, helping makers pursue multi-device households. Travelers and airlines value lighter adapters that power laptops, tablets, and phones from one outlet, while yield gains are trimming GaN bill-of-materials by 15-18% per year, protecting margins even as average selling prices soften.

Integration of Sustainable Materials in Accessory Manufacturing

The European Union's Ecodesign for Sustainable Products Regulation phases in a 25% recycled-plastic requirement for accessories by 2027, forcing redesign of supply chains around post-consumer resin. Apple's FineWoven MagSafe case contains 68% recycled content and cuts carbon footprint 45%, yet feedback shows early durability compromises. Peak Design added Fair Trade USA labor certification in 2024, spotlighting social compliance in a price-sensitive category. Brands under USD 50 million sales face per-unit testing costs triple those of multinationals, granting scale players a structural edge and accelerating consolidation in cases and cables where composition dictates Restriction of Hazardous Substances compliance.

Prevalence of Counterfeit Mobile Accessories

US Customs and Border Protection seized USD 20.7 million in fake accessories in Q1 2025, 62% of which imitated Apple cables and earbuds. EUIPO estimates EUR 1.3 billion (USD 1.47 billion) in lost sales across member states in 2024. Amazon's Brand Registry cut complaint rates 25% yet shifted the USD 50 000-200 000 annual policing burden onto brands. Counterfeits anchor consumer price expectations 60-70% lower than genuine items, while legitimate firms divert 8-12% of revenue to authentication tools, nudging them toward owned-web channels where they now capture 35-40% of sales.

Other drivers and restraints analyzed in the detailed report include:

- Growing Adoption of Wireless Audio

- Increasing Smartphone Penetration

- Stricter E-waste Regulations Raising Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Protective cases controlled 26.11% of the mobile accessories market share in 2025, confirming their role as the first add-on after a handset purchase. Wireless chargers, however, are projected to post a 6.96% CAGR that is slightly below the mobile accessories market size baseline, driven by Qi2's Magnetic Power Profile that lifts power from 15 W to 25 W and guarantees coil alignment, trimming energy loss 30%. Headphones and earbuds form the next-largest slice, propelled by TWS features once found only in premium models.

Power banks struggle with cell supply as battery makers prioritize electric vehicles, curbing high-capacity innovation, while screen protectors and car mounts plateau in low-growth territory. Smartwatch bands emerge as a fresh value pool because wearables refresh more often than phones, letting brands levy 40-60% gross margins. Category dynamics thus bifurcate into commoditized protection-and-charging goods where scale wins, versus ecosystem-anchored SKUs such as MagSafe chargers that sustain premium pricing despite limited technical gaps.

Online storefronts captured 54.22% of 2025 revenue and are slated for 7.67% CAGR as brands hunt data and margin by bypassing store rent and staffing costs. Amazon remains the top discovery venue even where final purchase occurs elsewhere, pressuring sellers to accept 15-20% commissions. Physical outlets, holding 45.78% share, fight falling foot traffic and rising rents that drag productivity below USD 400 per square foot.

Carrier shops lose relevance because device subsidies faded and consumers decouple accessory purchases. Brand-owned stores blend showroom flair with premium attachment, generating 35-40% of gross profit from accessories though they supply only a fifth of sales. In emerging markets, wholesale channels still matter but see margins squeezed as brands partner directly with platforms such as Flipkart and Noon. The EU Digital Services Act raised platform liability costs 12-15% yet boosted shopper trust online, accelerating channel polarization between premium owned-web sales and value-driven marketplaces.

Complete Report Scope:

- By Product Type

- Headphones / Earbuds

- Chargers

- Power Banks

- Protective Cases

- Screen Protectors

- Car Mounts

- Selfie Sticks and Gimbals

- Smartwatch Bands and Straps

- Other Product Types

- By Distribution Channel

- Online Retail

- Offline Retail

- Carrier Stores

- Brand-exclusive Stores

- Wholesale and Distributors

- By Price Range

- Low (Greater than or equal to USD 20)

- Mid (USD 21-50)

- Premium (Less than or equal USD 51)

- By Compatibility

- Android-specific Accessories

- iOS-specific Accessories

- Universal / Multi-platform Accessories

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Southeast Asia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- North America

Geography Analysis

Asia-Pacific contributed 39.75% of 2025 value, anchored by Shenzhen's factory network and India's INR 17 000 crore (USD 2.04 billion) production-linked incentives that localize component output. North America's 28% share faces lengthening handset cycles and category saturation, yet large brands benefit from regulatory demands that smaller rivals cannot meet. Europe's roughly 22% slice is reshaped by USB-C and e-waste rules that add USD 0.11-0.57 per unit in fees, favoring firms with in-house recycling.

The Middle East, though single-digit in size, is on track for a 7.77% CAGR as 95% smartphone penetration collides with USD 500 billion digital-infrastructure outlays under Saudi Vision 2030. South America grows mid-single-digits hindered by import duties up to 60%, triggering local assembly to tap Mercosur tariff breaks. Africa focuses on power continuity products like solar banks because grid reliability trumps brand.

Across regions, mature markets monetize through premium ecosystem gear, whereas emerging economies favor sub-USD 20 basics, creating a dual-speed outlook. Asia-Pacific will stay the volume hub while the Middle East and Southeast Asia capture outsized growth as e-commerce fulfillment penetrates secondary cities.

- Apple Inc.

- Samsung Electronics Co., Ltd.

- Sony Group Corporation

- Belkin International, Inc.

- Anker Innovations Ltd.

- Logitech International S.A.

- Western Digital Corporation

- Aukey Technology Co., Ltd.

- Bose Corporation

- Xiaomi Corporation

- Huawei Technologies Co., Ltd.

- BBK Electronics Corporation Ltd.

- ZAGG Inc.

- Otter Products LLC

- Skullcandy Inc.

- GN Audio A/S (Jabra)

- Plantronics, Inc. (Poly)

- Baseus Technology Co., Ltd.

- Ugreen Group Limited

- TP-Link Technology Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Smartphone Penetration

- 4.2.2 Expansion of E-commerce Channels

- 4.2.3 Growing Adoption of Wireless Audio

- 4.2.4 Rising Consumer Spending on Mobile Gaming Accessories

- 4.2.5 Adoption of GaN Technology Enabling Ultra-Compact Fast Chargers

- 4.2.6 Integration of Sustainable Materials in Accessory Manufacturing

- 4.3 Market Restraints

- 4.3.1 Prevalence of Counterfeit Mobile Accessories

- 4.3.2 Saturation in Replacement Accessory Cycles

- 4.3.3 Stricter E-waste Regulations Raising Compliance Costs

- 4.3.4 Supply Constraints in Advanced Battery Cells for High-Capacity Power Banks

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Headphones / Earbuds

- 5.1.2 Chargers

- 5.1.3 Power Banks

- 5.1.4 Protective Cases

- 5.1.5 Screen Protectors

- 5.1.6 Car Mounts

- 5.1.7 Selfie Sticks and Gimbals

- 5.1.8 Smartwatch Bands and Straps

- 5.1.9 Other Product Types

- 5.2 By Distribution Channel

- 5.2.1 Online Retail

- 5.2.2 Offline Retail

- 5.2.3 Carrier Stores

- 5.2.4 Brand-exclusive Stores

- 5.2.5 Wholesale and Distributors

- 5.3 By Price Range

- 5.3.1 Low (Greater than or equal to USD 20)

- 5.3.2 Mid (USD 21-50)

- 5.3.3 Premium (Less than or equal USD 51)

- 5.4 By Compatibility

- 5.4.1 Android-specific Accessories

- 5.4.2 iOS-specific Accessories

- 5.4.3 Universal / Multi-platform Accessories

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Southeast Asia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Kenya

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Apple Inc.

- 6.4.2 Samsung Electronics Co., Ltd.

- 6.4.3 Sony Group Corporation

- 6.4.4 Belkin International, Inc.

- 6.4.5 Anker Innovations Ltd.

- 6.4.6 Logitech International S.A.

- 6.4.7 Western Digital Corporation

- 6.4.8 Aukey Technology Co., Ltd.

- 6.4.9 Bose Corporation

- 6.4.10 Xiaomi Corporation

- 6.4.11 Huawei Technologies Co., Ltd.

- 6.4.12 BBK Electronics Corporation Ltd.

- 6.4.13 ZAGG Inc.

- 6.4.14 Otter Products LLC

- 6.4.15 Skullcandy Inc.

- 6.4.16 GN Audio A/S (Jabra)

- 6.4.17 Plantronics, Inc. (Poly)

- 6.4.18 Baseus Technology Co., Ltd.

- 6.4.19 Ugreen Group Limited

- 6.4.20 TP-Link Technology Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment