PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061322

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061322

Passenger Vehicle Fleet Maintenance and Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

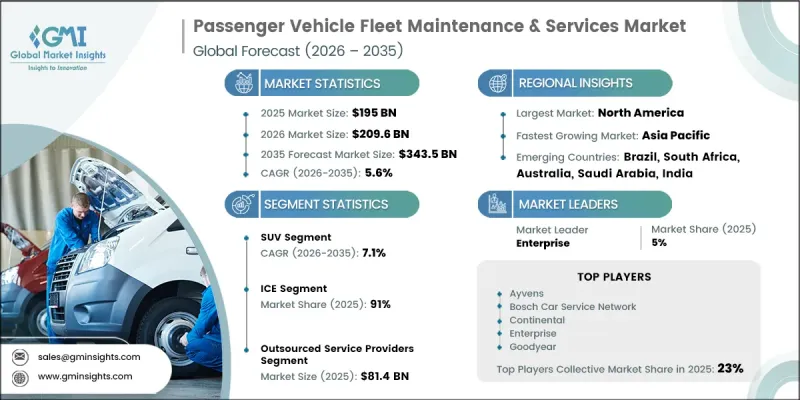

The Global Passenger Vehicle Fleet Maintenance & Services Market was valued at USD 195 billion in 2025 and is estimated to grow at a CAGR of 5.6% to reach USD 343.5 billion by 2035.

The market is rapidly evolving into a technology-driven and software-enabled ecosystem as fleet operators increasingly focus on maximizing vehicle uptime, improving cost efficiency, and ensuring regulatory compliance. Traditional scheduled servicing approaches are gradually being replaced by predictive and condition-based maintenance systems supported by telematics, IoT-enabled sensors, and AI-powered diagnostic technologies. This transition is particularly prominent across logistics, utility, and delivery fleets where vehicle downtime can significantly impact operational performance and profitability. The industry is also witnessing accelerated market consolidation and strategic acquisitions aimed at strengthening telematics capabilities and integrated fleet service platforms. Increasing adoption of AI-enabled safety technologies and real-time fleet monitoring tools is enhancing driver behavior analysis, operational visibility, and accident prevention. Advanced systems such as intelligent dash cameras, predictive alerts, and video telematics are helping operators reduce risks, lower insurance costs, and improve compliance management. As a result, fleet maintenance services are increasingly becoming part of a fully connected digital ecosystem that combines maintenance operations, repairs, claims management, and fleet analytics within a unified framework.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $195 Billion |

| Forecast Value | $343.5 Billion |

| CAGR | 5.6% |

The SUV segment accounted for 37% share in 2025 and is expected to grow at a CAGR of 7.1% from 2026 to 2035. Growth in this segment is primarily driven by the rising use of SUVs across corporate fleets, ride-hailing services, and premium mobility operations. The increasing complexity associated with servicing larger vehicles is generating higher demand for flexible and mobile maintenance solutions designed to reduce downtime and improve operational convenience. Mobile servicing models are becoming increasingly important in urban fleet management strategies due to their ability to enhance service accessibility and efficiency.

The ICE segment held a 91% share in 2025 and is forecast to grow at a CAGR of 4.6% through 2035. Internal combustion engine vehicles continue to maintain a strong market position due to the large global volume of gasoline and diesel-powered fleets operating across passenger and commercial transportation sectors. Service providers are increasingly focusing on integrated maintenance ecosystems, expanding service accessibility, and introducing convenience-driven maintenance solutions to improve customer retention and operational effectiveness.

United States Passenger Vehicle Fleet Maintenance & Services Market generated USD 82.2 billion in 2025. The region represents one of the most advanced and mature markets globally, supported by extensive fleet operations, established third-party maintenance networks, sophisticated fleet management systems, and favorable pricing structures that support strong profitability for service providers.

Major companies operating in the Global Passenger Vehicle Fleet Maintenance & Services Industry include Ayvens, Bosch Car Service Network, Bridgestone, Continental, Dana Incorporated, DENSO, Element Fleet Management, Enterprise, Goodyear, and Holman. Companies operating in the passenger vehicle fleet maintenance & services market are implementing several strategic initiatives to strengthen their competitive position and expand market presence. A major focus area involves investing in advanced telematics platforms, AI-powered diagnostics, and predictive maintenance technologies to improve operational efficiency and reduce vehicle downtime. Service providers are also expanding mobile maintenance capabilities and on-site servicing models to enhance customer convenience and improve response times. Strategic mergers, acquisitions, and partnerships are helping companies strengthen digital fleet management capabilities and broaden service portfolios. In addition, organizations are integrating real-time monitoring systems, safety analytics, and connected vehicle technologies to deliver comprehensive fleet solutions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Vehicle

- 2.2.2 Service

- 2.2.3 Fleet Ownership

- 2.2.4 Propulsion

- 2.2.5 Service Delivery

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material suppliers

- 3.1.1.2 Component suppliers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Service providers

- 3.1.1.5 Distribution channel

- 3.1.1.6 End Use

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Vertical integration trends

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising commercial-use passenger vehicle parc

- 3.2.1.2 Higher vehicle utilization & mileage intensity

- 3.2.1.3 Aging global passenger vehicle fleet

- 3.2.1.4 Growth of outsourcing in fleet maintenance

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High informal servicing in emerging markets

- 3.2.2.2 OEM warranty and bundled service contracts

- 3.2.3 Market opportunities

- 3.2.3.1 Predictive maintenance & telematics adoption

- 3.2.3.2 Growth of mobility service fleets

- 3.2.3.3 Electrification of fleet vehicles

- 3.2.3.4 Mobile and on-demand maintenance services

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pricing Analysis (Driven by Primary Research)

- 3.4.1 Historical Price Trend Analysis

- 3.4.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.1.1 ACT Regulation

- 3.5.1.2 EPA Phase 3

- 3.5.2 Europe

- 3.5.2.1 CO2 Emission Standards

- 3.5.2.2 Euro 6/Next Generation Standards

- 3.5.3 Asia-Pacific

- 3.5.3.1 Emission Reduction Targets

- 3.5.3.2 China-6 Standard

- 3.5.4 Latin America

- 3.5.4.1 Brazil Proconve P8

- 3.5.4.2 Mexico EPA-Aligned Standards

- 3.5.5 MEA

- 3.5.5.1 Saudi Vision 2030 Green Initiatives

- 3.5.5.2 South Africa EV Tax Rebates

- 3.5.1 North America

- 3.6 Technology and Innovation landscape

- 3.6.1 Current technologies

- 3.6.2 Emerging technologies

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

- 3.9 Patent analysis (Driven by Primary Research)

- 3.10 Capacity & production landscape (Driven by Primary Research)

- 3.10.1 Installed capacity by region & key producer

- 3.10.2 Capacity utilization rates & expansion pipelines

- 3.11 Trade data analysis (Driven by Paid Research)

- 3.11.1 Intra Trade Flows - Volume & Value Trends

- 3.11.2 Import/Export Corridor Analysis

- 3.12 Impact of AI & generative AI on the market

- 3.12.1 AI-Driven Disruption of Existing Business Models

- 3.12.2 Automated design optimization

- 3.12.3 Supply chain AI for demand forecasting

- 3.12.4 GenAI use cases & adoption roadmap by segment

- 3.12.5 Risks, Limitations & Regulatory Considerations

- 3.13 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.13.1 Base Case - key macro & industry variables driving CAGR

- 3.13.2 Optimistic Scenarios - Favorable Macro and Industry Tailwinds

- 3.13.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly Initiatives

- 3.14.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia-Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans and funding

- 4.5 Company tier benchmarking

- 4.5.1 Tier classification criteria & qualifying thresholds

- 4.5.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 SUV

- 5.3 Sedan

- 5.4 Hatchback

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Service, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Preventive Maintenance

- 6.3 Telematics-driven Diagnostics

- 6.4 Body-shop Collision Repairs

- 6.5 Emergency/Corrective Repairs

- 6.6 Tires, Brakes, Batteries & Lubricants

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Fleet Ownership, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Private Corporate Fleets

- 7.3 Government Fleets

- 7.4 Rental and Leasing Companies

- 7.5 Mobility Service Providers

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 ICE

- 8.3 Electric

- 8.4 Hybrid

Chapter 9 Market Estimates & Forecast, By Service Delivery, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 In-House/Captive Workshops

- 9.3 Outsourced Service Providers

- 9.4 Mobile/On-Site Services

- 9.5 Hybrid Models

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 10.1 North America

- 10.1.1 US

- 10.1.2 Canada

- 10.2 Europe

- 10.2.1 UK

- 10.2.2 Germany

- 10.2.3 France

- 10.2.4 Italy

- 10.2.5 Spain

- 10.2.6 Belgium

- 10.2.7 Netherlands

- 10.2.8 Sweden

- 10.2.9 Russia

- 10.3 Asia Pacific

- 10.3.1 China

- 10.3.2 India

- 10.3.3 Japan

- 10.3.4 Australia

- 10.3.5 Singapore

- 10.3.6 South Korea

- 10.3.7 Vietnam

- 10.3.8 Indonesia

- 10.3.9 Thailand

- 10.4 Latin America

- 10.4.1 Brazil

- 10.4.2 Mexico

- 10.4.3 Argentina

- 10.5 MEA

- 10.5.1 South Africa

- 10.5.2 Saudi Arabia

- 10.5.3 UAE

- 10.5.4 Turkey

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 ARI (Holman Fleet Management)

- 11.1.2 Bosch Car Service

- 11.1.3 Bridgestone

- 11.1.4 Continental

- 11.1.5 Dana Incorporated

- 11.1.6 DENSO

- 11.1.7 Element Fleet Management

- 11.1.8 Enterprise Holdings

- 11.1.9 LeasePlan

- 11.1.10 The Goodyear Tire & Rubber Company

- 11.1.11 Wheels, Inc.

- 11.1.12 ZF Friedrichshafen AG

- 11.2 Regional players

- 11.2.1 Castrol Auto Service

- 11.2.2 Eurorepar Car Service

- 11.2.3 Firestone Complete Auto Care

- 11.2.4 Inchcape

- 11.2.5 Midas

- 11.2.6 Pep Boys

- 11.3 Emerging players

- 11.3.1 Tmall Car Maintenance

- 11.3.2 Tuhu Car Maintenance