PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071194

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071194

Automotive Battery Rebuild Service Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

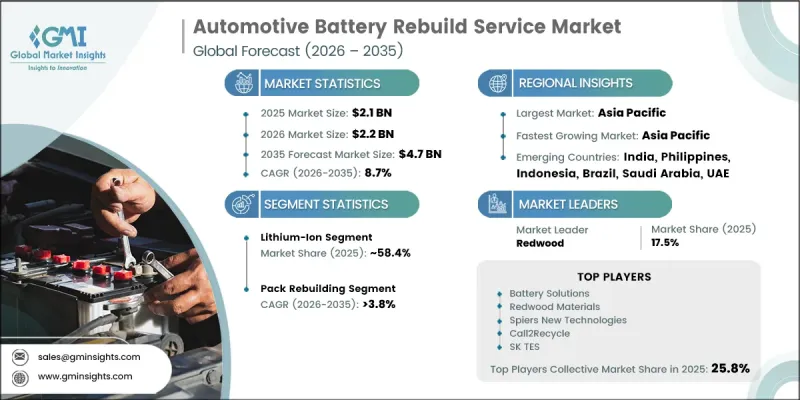

The Global Automotive Battery Rebuild Service Market was valued at USD 2.1 billion in 2025 and is estimated to grow at a CAGR of 8.7% to reach USD 4.7 billion by 2035.

The market is gaining momentum as the automotive sector continues to embrace advanced technologies across hybrid and electric vehicles. As electric vehicle batteries represent a substantial ownership expense and play a critical role in vehicle performance and reliability, industry participants are increasingly focusing on solutions that maximize battery lifespan and reduce replacement costs. The growing preference for battery restoration and lifecycle optimization services is reshaping the aftermarket landscape. Market demand is being supported by the need to improve battery durability, lower long-term operating expenses, and promote more sustainable vehicle ownership. As battery replacement remains a costly option, rebuilding services are emerging as an economical alternative for vehicle owners and fleet operators. The industry is also benefiting from stronger cooperation among vehicle manufacturers, battery producers, service specialists, and battery recovery organizations, which is fostering innovation and creating growth opportunities for engineering and technology-focused businesses operating within the automotive battery ecosystem.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.1 Billion |

| Forecast Value | $4.7 Billion |

| CAGR | 8.7% |

The Automotive Battery Rebuild Service Market is witnessing increasing demand for specialized battery restoration solutions that focus on extending battery usability and maintaining performance standards. Service offerings encompass battery cell replacement, battery module restoration, battery management system repairs, and thermal management system refurbishment. These solutions are helping vehicle owners improve battery efficiency while supporting sustainability initiatives through reduced resource consumption and extended product lifecycles. The increasing emphasis on battery health management is driving wider adoption of rebuilding services across the automotive sector.

The lithium-ion segment held a 58.4% share in 2025 and is anticipated to grow at a CAGR of 9.4% through 2035. Market growth within this segment is being driven by the widespread deployment of lithium-ion batteries in modern electric and hybrid vehicles. As the installed base of these vehicles continues to expand, demand for cost-effective battery restoration services is expected to rise steadily. The ability to restore battery functionality while avoiding full replacement expenses is encouraging greater utilization of rebuilding solutions.

The battery pack rebuilding segment accounted for 27.1% share in 2025 and is forecast to grow at a CAGR of 3.8% between 2026 and 2035. This segment maintains a substantial market share as vehicle owners and fleet managers seek practical solutions to restore battery performance and preserve driving range. Battery pack rebuilding activities focus on cell balancing, module restoration, and optimization of thermal management systems. The growing popularity of these services is closely linked to sustainability objectives and efforts to minimize electronic waste while maximizing battery utilization.

China Automotive Battery Rebuild Service Market is expected to record substantial growth from 2026-2035 period. Market expansion is being supported by the rapid adoption of electric vehicles, increasing awareness regarding battery lifespan extension, and rising demand for economical battery refurbishment services. The country's extensive electric vehicle population and developing aftermarket infrastructure continue to generate strong demand for battery diagnostics, repair services, cell replacement solutions, and battery pack restoration activities. In addition, China's well-established manufacturing ecosystem and reliable access to battery materials are enabling efficient rebuilding operations and supporting the expansion of large-scale service networks.

The leading companies operating in the Global Automotive Battery Rebuild Service Market include LKQ, Clarios, Battery Solutions, Redwood Materials, Spiers New Technologies, Call2Recycle, and SK TES. Companies operating in the Automotive Battery Rebuild Service Market are strengthening their market position through strategic partnerships, technology investments, and service network expansion. Many industry participants are collaborating with automakers, battery manufacturers, and aftermarket service providers to enhance battery rebuilding capabilities and improve customer access to refurbishment solutions. Businesses are investing in advanced diagnostic technologies, battery testing systems, and automated repair processes to improve service quality and operational efficiency.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Battery

- 2.2.3 Service

- 2.2.4 Battery Capacity

- 2.2.5 Application

- 2.2.6 Propulsion

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global adoption of electric passenger and commercial vehicles

- 3.2.1.2 Increase in government incentives, subsidies, and EV infrastructure investments

- 3.2.1.3 Expansion of battery refurbishment facilities and localized service infrastructure

- 3.2.1.4 Growing electrification of logistics, public transport, and fleet vehicles

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost and technical complexity of battery rebuilding operations

- 3.2.2.2 Limited large-scale battery recycling and end-of-life infrastructure

- 3.2.3 Market opportunities

- 3.2.3.1 Rise in adoption of advanced battery diagnostics and next-generation battery technologies

- 3.2.3.2 Increase in domestic battery refurbishment supported by sustainability and localization policies

- 3.2.3.3 Surge in demand for advanced battery management systems and predictive maintenance solutions

- 3.2.3.4 Growth in second-life battery applications and battery recycling ecosystems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pricing Analysis (Driven by Primary Research)

- 3.4.1 Historical Price Trend Analysis

- 3.4.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.1.1 U.S.: Environmental Protection Agency (EPA) Regulations for Automotive Battery Rebuild and Recycling Services

- 3.5.1.2 Canada: Canadian Environmental Protection Regulations for Automotive Battery Reconditioning Services

- 3.5.2 Europe

- 3.5.2.1 UK: UK Waste Batteries and Accumulators Regulations for Automotive Battery Rebuild Services

- 3.5.2.2 Germany: Germany Battery Act (BattG) Regulations for Automotive Battery Rebuild Services

- 3.5.2.3 France: France Extended Producer Responsibility Regulations for Automotive Battery Refurbishment Services

- 3.5.3 Asia-Pacific

- 3.5.3.1 China: China New Energy Vehicle Battery Recycling Regulations for Automotive Battery Rebuild Services

- 3.5.3.2 India: India Battery Waste Management Rules for Automotive Battery Rebuild Services

- 3.5.3.3 Japan: Japan Act on Promotion of Effective Resource Utilization for Automotive Battery Rebuild Services

- 3.5.4 Latin America

- 3.5.4.1 Brazil: Brazil National Solid Waste Policy Regulations for Automotive Battery Reconditioning Services

- 3.5.5 MEA

- 3.5.5.1 Saudi Arabia: Saudi Arabia Environmental Waste Management Regulations for Automotive Battery Rebuild Services

- 3.5.1 North America

- 3.6 Technology and Innovation Landscape

- 3.6.1 Current technologies

- 3.6.2 Emerging technologies

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Patent analysis (Driven by Primary Research)

- 3.10 Impact of AI & generative AI on the market

- 3.10.1 AI-Driven Disruption of Existing Business Models

- 3.10.2 Automated design optimization

- 3.10.3 Supply chain AI for demand forecasting

- 3.10.4 GenAI use cases & adoption roadmap by segment

- 3.10.5 Risks, Limitations & Regulatory Considerations

- 3.11 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.11.1 Base Case - key macro & industry variables driving CAGR

- 3.11.2 Optimistic Scenarios - Favorable Macro and Industry Tailwinds

- 3.11.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Battery, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Lithium-Ion Batteries

- 5.3 Nickel Metal Hydride (NiMH) Batteries

- 5.4 Lead-Acid Batteries

- 5.5 Solid-State Batteries

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Service, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 Diagnostics & Testing

- 6.3 Cell Replacement

- 6.4 Pack Rebuilding

- 6.5 Module Refurbishment

- 6.6 Management System (BMS) Repair

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Battery Capacity, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 Below 20 kWh

- 7.3 20-50 kWh

- 7.4 50-100 kWh

- 7.5 Above 100 kWh

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 Private Passenger Vehicles

- 8.3 Commercial Passenger Services

- 8.4 Public Transit Fleets

- 8.5 Commercial Freight & Logistics

- 8.6 Construction & Mining Equipment

- 8.7 Agricultural Vehicles

- 8.8 Industrial & Warehouse Equipment

- 8.9 Others

Chapter 9 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 Internal Combustion Engine (ICE) Vehicles

- 9.3 Hybrid Vehicles

- 9.4 Battery Electric Vehicles (BEVs)

- 9.5 Plug-in Hybrid Electric Vehicles (PHEVs)

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordic

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Philippines

- 10.4.7 Indonesia

- 10.4.8 Singapore

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 LKQ

- 11.1.2 Clarios

- 11.1.3 Redwood Materials

- 11.1.4 TES

- 11.1.5 Battery Solutions

- 11.1.6 Spiers New Technologies

- 11.1.7 Li-Cycle

- 11.1.8 Umicore

- 11.1.9 Contemporary Amperex Technology

- 11.1.10 Ecobat

- 11.2 Regional Players

- 11.2.1 Electron Automotive

- 11.2.2 Greentec Auto

- 11.2.3 Hybrid Battery 911

- 11.2.4 Best Hybrid Batteries

- 11.2.5 Battrixx

- 11.2.6 Ace Green Recycling

- 11.2.7 4R Energy

- 11.2.8 Connected Energy

- 11.2.9 Renewance

- 11.2.10 BatX Energies