PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071247

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071247

Commercial On-Demand Vehicle Repair Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

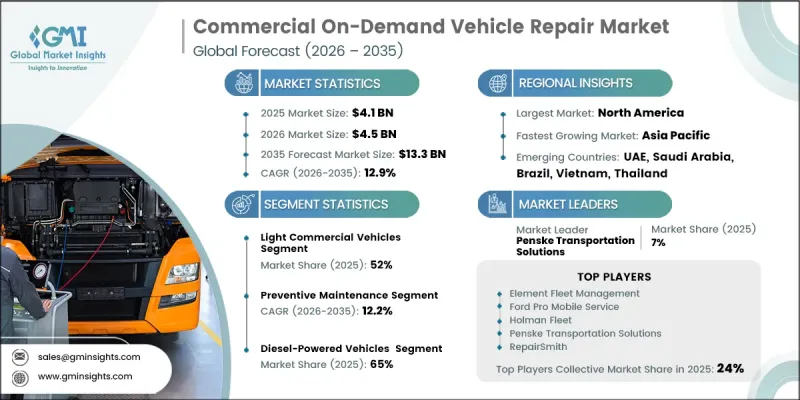

The Global Commercial On-Demand Vehicle Repair Market was valued at USD 4.1 billion in 2025 and is estimated to grow at a CAGR of 12.9% to reach USD 13.3 billion by 2035.

The industry is undergoing a significant transformation as maintenance services shift from reactive breakdown support toward digitally managed, scheduled repair solutions delivered directly to vehicle locations. This evolution is gaining momentum across fleet depots, distribution centers, parking facilities, and other operational sites where minimizing downtime is critical. Growth is particularly strong among commercial fleet operators that rely on high vehicle utilization and cannot afford extended service interruptions. The primary driver behind adoption is the increasing focus on fleet availability and operational efficiency. Every reduction in maintenance-related delays contributes to improved productivity, lower operating costs, and enhanced service performance. Traditional workshop-based maintenance often requires vehicle transportation, appointment scheduling, and prolonged idle periods, all of which impact revenue-generating activities. Mobile repair services address these challenges by bringing technicians, diagnostic equipment, and replacement parts directly to the vehicle, enabling faster service completion and reducing operational disruptions. As commercial transportation networks become increasingly time-sensitive, the commercial on-demand vehicle repair market is emerging as a strategic solution for fleet optimization and maintenance efficiency.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.1 Billion |

| Forecast Value | $13.3 Billion |

| CAGR | 12.9% |

The continued expansion of e-commerce activity and urban distribution networks is generating substantial demand for mobile repair services across metropolitan regions. Rapid growth in commercial delivery operations has increased the need for dependable vehicle maintenance solutions capable of supporting intensive daily usage patterns. Frequent vehicle operation under demanding conditions contributes to higher maintenance requirements, increasing demand for accessible service models that minimize downtime and improve fleet productivity. As logistics operators seek greater operational flexibility, on-demand repair services are becoming an increasingly attractive alternative to conventional maintenance channels.

The light commercial vehicles segment accounted for 52% share in 2025 and is projected to grow at a CAGR of 13.1% through 2035. This segment includes a broad range of vehicles commonly utilized for transportation, distribution, service operations, and urban logistics activities. The category remains highly significant due to its central role in commercial mobility and city-based delivery ecosystems. Distinct operating patterns, regulatory classifications, and utilization rates contribute to strong demand for flexible maintenance solutions specifically tailored to light commercial vehicle fleets.

The preventive maintenance segment held a 38% share in 2025 and is forecast to grow at a CAGR of 12.2% through 2035. The segment encompasses routine service activities designed to maintain vehicle performance, improve safety, and reduce the likelihood of unexpected mechanical failures. Scheduled maintenance programs continue to gain importance among fleet operators seeking to maximize asset utilization and control long-term operating expenses. Mobile service delivery is particularly well-suited for preventive maintenance because service requirements are predictable, scheduling can be planned in advance, and operational disruptions can be minimized. As fleet management strategies become increasingly data-driven, demand for preventive maintenance services is expected to remain strong throughout the forecast period.

Europe Commercial On-Demand Vehicle Repair Market held a 27% share in 2025 and is projected to grow at a CAGR of 11.4% through 2035. Market growth across Europe is supported by a strong transportation infrastructure, extensive commercial vehicle activity, and rising emphasis on fleet efficiency. Increasing adoption of mobile maintenance solutions is driven by efforts to improve vehicle availability, optimize operational performance, and meet evolving transportation requirements across major regional economies.

Key companies operating in the Global Commercial On-Demand Vehicle Repair Market include Geotab, Pitstop, Ford Pro Mobile Service, TRUCKUP, Cafler, Wrench, Penske Transportation Solutions, Element Fleet Management, RepairSmith, FixMyCar, Cox Fleet, Holman, GoMechanic, CarPass, FleetNation, Yoshi, AutoFix, ClickMechanic, Fixico, Spiffy, and Trimble Transportation. Companies operating within the commercial on-demand vehicle repair industry are pursuing multiple strategies to strengthen their market presence and enhance competitive positioning. Leading participants are investing in digital service platforms, predictive maintenance technologies, fleet analytics, and mobile workforce management solutions to improve operational efficiency and customer experience. Strategic partnerships with fleet operators, logistics providers, vehicle manufacturers, and technology companies are helping expand service networks and increase customer acquisition. Market players are also focusing on geographic expansion, technician network growth, and service diversification to address a wider range of commercial vehicle requirements. Investments in real-time diagnostics, connected vehicle technologies, and automated scheduling systems are improving service responsiveness and reducing repair turnaround times.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Service

- 2.2.2 Vehicle

- 2.2.3 Service Mode

- 2.2.4 Fuel

- 2.2.5 Provider

- 2.2.6 Booking Channel

- 2.2.7 Application

- 2.2.8 End use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Replacement parts & consumables

- 3.1.1.2 Diagnostic hardware & software providers

- 3.1.1.3 Aftermarket component manufacturers

- 3.1.1.4 On-demand mobile repair operators

- 3.1.1.5 Distribution Channel

- 3.1.1.6 End Use

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Vertical integration trends

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising fleet uptime optimization requirements

- 3.2.1.2 Growth of e-commerce & last-mile delivery fleets

- 3.2.1.3 Increasing telematics & connected vehicle adoption

- 3.2.1.4 Labor shortages in conventional repair workshops

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Fragmented service provider ecosystem

- 3.2.2.2 Limited skilled mobile technician availability

- 3.2.3 Market opportunities

- 3.2.3.1 AI-enabled predictive maintenance scheduling

- 3.2.3.2 Growth of OEM-authorized mobile service networks

- 3.2.3.3 Increasing adoption of app-based service booking

- 3.2.3.4 Remote diagnostics and virtual assistance integration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pricing Analysis (Driven by Primary Research)

- 3.4.1 Historical Price Trend Analysis

- 3.4.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.1.1 US: FMCSA Hours of Service (HOS) for Mobile Technicians

- 3.5.1.2 Canada: OSHA Mobile Workplace Safety Standards

- 3.5.2 Europe

- 3.5.2.1 Germany: EU Mobile Workforce & Working Time Directive

- 3.5.2.2 UK: REACH & Hazardous Material Transport for Mobile Repairs

- 3.5.2.3 France: NF C15-100 (V2G Addendum)

- 3.5.2.4 Netherlands: PTP-2025 (Smart Charging & V2G)

- 3.5.3 Asia-Pacific

- 3.5.3.1 Japan: Road Transport Vehicle Act for Mobile Services

- 3.5.3.2 China: Heavy Vehicle National Law (HVNL) Mobile Repair Provisions

- 3.5.3.3 South Korea: KEMCO V2G Certification

- 3.5.3.4 Australia: AS/NZS 4777.2 (2020+)

- 3.5.4 Latin America

- 3.5.4.1 Brazil: Mobile Automotive Repair Service Registration

- 3.5.4.2 Chile: PROFECO Consumer Protection for Mobile Repairs

- 3.5.5 Middle East & Africa

- 3.5.5.1 UAE: Municipal Mobile Service Vehicle Permits

- 3.5.5.2 Saudi Arabia: Retail Motor Industry (RMI) Mobile Workshop Accreditation

- 3.5.1 North America

- 3.6 Technology and Innovation landscape

- 3.6.1 Current technologies

- 3.6.2 Emerging technologies

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Patent analysis (Driven by Primary Research)

- 3.10 Impact of AI & generative AI on the market

- 3.10.1 AI-Driven Disruption of Existing Business Models

- 3.10.2 Automated design optimization

- 3.10.3 Supply chain AI for demand forecasting

- 3.10.4 GenAI use cases & adoption roadmap by segment

- 3.10.5 Risks, Limitations & Regulatory Considerations

- 3.11 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.11.1 Base Case - key macro & industry variables driving CAGR

- 3.11.2 Optimistic Scenarios - Favorable Macro and Industry Tailwinds

- 3.11.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia-Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans and funding

- 4.5 Company tier benchmarking

- 4.5.1 Tier classification criteria & qualifying thresholds

- 4.5.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Service, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Preventive Maintenance Services

- 5.2.1 Oil & filter changes

- 5.2.2 Fluid replacements

- 5.2.3 Belt & hose replacements

- 5.2.4 Filter replacements

- 5.2.5 Others

- 5.3 Corrective repair services

- 5.3.1 Brake system repairs

- 5.3.2 Engine & drivetrain repairs

- 5.3.3 Suspension & steering repairs

- 5.3.4 Electrical system repair

- 5.3.5 Others

- 5.4 Diagnostic services

- 5.4.1 Check engine light & OBD-II diagnostics

- 5.4.2 No-start diagnostics

- 5.4.3 Pre-purchase vehicle inspections

- 5.4.4 Others

- 5.5 Emergency & roadside assistance

- 5.5.1 Battery jump-start services

- 5.5.2 Flat tire repair & replacement

- 5.5.3 Emergency fuel delivery

- 5.5.4 Others

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Light commercial vehicles (LCV)

- 6.3 Medium commercial vehicles (MCV)

- 6.4 Heavy commercial vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Service Mode, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 On-site/mobile service

- 7.3 Pickup and return service

- 7.4 Remote diagnosis and assistance

Chapter 8 Market Estimates & Forecast, By Fuel, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 Gasoline

- 8.3 Diesel

- 8.4 All-electric

- 8.4.1 PHEV

- 8.4.2 HEV

- 8.4.3 FCEV

Chapter 9 Market Estimates & Forecast, By Provider, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 Platform-based aggregators

- 9.3 Independent mobile mechanics

- 9.4 OEM-authorized mobile service networks

- 9.5 Franchise-based mobile service providers

Chapter 10 Market Estimates & Forecast, By Booking Channel, 2022 - 2035 ($Mn)

- 10.1 Key trends

- 10.2 Mobile applications

- 10.3 Websites and web portals

- 10.4 Call centers and phone booking

- 10.5 Telematics and OBD-II auto-booking

- 10.6 OEM in-car integration

Chapter 11 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn)

- 11.1 Key trends

- 11.2 Logistics & Transportation

- 11.3 E-commerce & Last-Mile Delivery

- 11.4 Construction & Infrastructure

- 11.5 Field Services

- 11.6 Corporate & Government Fleets

- 11.7 Others

Chapter 12 Market Estimates & Forecast, By End use, 2022 - 2035 ($Mn)

- 12.1 Key trends

- 12.2 B2B

- 12.3 B2C

Chapter 13 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 13.1 North America

- 13.1.1 US

- 13.1.2 Canada

- 13.2 Europe

- 13.2.1 UK

- 13.2.2 Germany

- 13.2.3 France

- 13.2.4 Italy

- 13.2.5 Spain

- 13.2.6 Belgium

- 13.2.7 Netherlands

- 13.2.8 Sweden

- 13.2.9 Russia

- 13.3 Asia Pacific

- 13.3.1 China

- 13.3.2 India

- 13.3.3 Japan

- 13.3.4 Australia

- 13.3.5 Singapore

- 13.3.6 South Korea

- 13.3.7 Vietnam

- 13.3.8 Indonesia

- 13.3.9 Thailand

- 13.4 Latin America

- 13.4.1 Brazil

- 13.4.2 Mexico

- 13.4.3 Argentina

- 13.5 MEA

- 13.5.1 South Africa

- 13.5.2 Saudi Arabia

- 13.5.3 UAE

- 13.5.4 Turkey

Chapter 14 Company Profiles

- 14.1 Global players

- 14.1.1 ClickMechanic

- 14.1.2 Element Fleet Management

- 14.1.3 Fixter

- 14.1.4 Holman

- 14.1.5 Penske Truck Leasing

- 14.1.6 RepairSmith (AutoNation)

- 14.1.7 Spiffy

- 14.1.8 Road Rescue Network

- 14.1.9 Wrench (YourMechanic)

- 14.1.10 Yoshi

- 14.2 Regional players

- 14.2.1 AutoFix

- 14.2.2 Cafler

- 14.2.3 CarPass

- 14.2.4 Instant Car Fix

- 14.2.5 FixMyCar

- 14.2.6 GoMechanic

- 14.2.7 Jrop

- 14.3 Emerging players

- 14.3.1 Cox Fleet

- 14.3.2 FleetNation

- 14.3.3 TRUCKUP