PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061359

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061359

North America Forklift Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

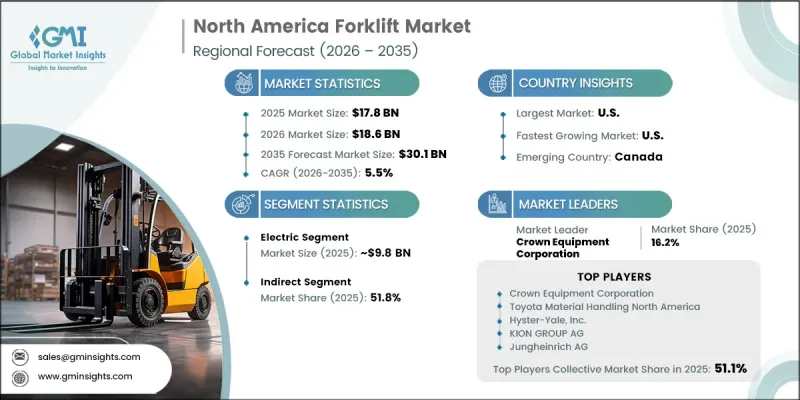

North America Forklift Market was valued at USD 17.8 billion in 2025 and is estimated to grow at a CAGR of 5.5% to reach USD 30.1 billion by 2035.

The regional forklift industry operates within a highly structured business environment, where many manufacturers are associated with industry organizations such as the Industrial Truck Association (ITA). Continuous technological advancement is playing a major role in shaping the market as companies across North America increasingly adopt connected and intelligent material handling systems. The growing implementation of telematics, IoT-integrated forklifts, and autonomous navigation technologies is transforming operational efficiency across warehouses and industrial facilities. Innovation within the regional material handling sector is being driven by the combination of smart industrial technologies and automated power-driven equipment solutions. The rising deployment of autonomous forklifts and automated guided systems in large-scale distribution environments is improving workflow productivity while also enhancing workplace safety standards. In addition, advanced fleet management software integrated with predictive maintenance capabilities is significantly improving equipment monitoring, operational reliability, and asset utilization throughout industrial operations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $17.8 Billion |

| Forecast Value | $30.1 Billion |

| CAGR | 5.5% |

The electric forklift segment generated USD 9.8 billion in 2025 and is anticipated to reach USD 19.3 billion by 2035. The regional market is experiencing a clear transition toward cleaner and more energy-efficient power technologies, reducing dependence on traditional internal combustion engine-powered equipment. This shift is supported by economic advantages, improved equipment performance, and increasingly strict environmental and workplace regulations. Businesses operating in indoor warehouse and logistics environments are showing a growing preference for electric forklifts due to their operational efficiency, reduced emissions, and lower maintenance requirements. The increasing focus on sustainability and energy-efficient industrial operations is also strengthening demand for electric-powered material handling solutions throughout North America.

The indirect sales segment held a 51.8% share in 2025. The regional industry relies heavily on extensive dealership and distributor networks that serve as intermediaries between equipment manufacturers and end users across local markets. Indirect distribution channels continue to maintain a strong market presence due to their ability to provide flexible rental solutions and localized equipment support services. The availability of rental fleets allows businesses to quickly expand operational capacity during periods of increased warehouse and distribution activity. This distribution structure helps industrial operators avoid long procurement lead times associated with purchasing new equipment while ensuring immediate access to replacement units whenever operational demand rises unexpectedly. Strong dealer relationships and after-sales support capabilities continue to strengthen the importance of indirect sales channels across the regional forklift industry.

U.S. Forklift Market accounted for 81.7% share in 2025. Market expansion in the country is being fueled by rapid growth in warehousing infrastructure, logistics operations, and e-commerce fulfillment activities. The increasing development of large-scale distribution facilities has accelerated demand for both electric and automated forklift systems. Companies are prioritizing investments in efficient material handling technologies to support faster inventory movement and improve supply chain productivity. Technological advancements, including lithium-ion battery systems, telematics integration, and semi-autonomous forklift technologies, are further supporting market growth. In addition, growing regulatory emphasis on workplace safety standards and emissions reduction is encouraging businesses to transition toward cleaner and more advanced electric forklift equipment.

Major companies operating in the North America Forklift Market include Big Joe Forklifts, Caterpillar Inc., Clark Material Handling, Combilift, Crown Equipment Corporation, Doosan Bobcat North America Inc., Fox Robotics, Guangxi LiuGong Machinery, Hoist Liftruck Manufacturing, Hubtex, Hyster-Yale, Inc., Hyundai Material Handling, Jungheinrich AG, KION GROUP AG, Manitou Group SA, Mitsubishi Logisnext Co., Ltd., Noblelift Intelligent Equipment, Pettibone LLC, Sellick Equipment Limited, Taylor Forklifts, Toyota Material Handling North America, and Titan Forklifts. Companies participating in the North America forklift industry are adopting several strategic initiatives to strengthen their market position and expand customer reach. Leading manufacturers are increasing investments in electric forklift technologies, automation systems, and connected fleet management platforms to improve operational efficiency and product innovation. Businesses are also focusing on expanding dealership networks and rental service capabilities to strengthen regional distribution and after-sales support. Strategic partnerships, acquisitions, and collaborations with logistics providers and warehouse operators are helping companies improve market penetration and customer retention. In addition, manufacturers are prioritizing research and development activities related to lithium-ion batteries, autonomous navigation systems, and predictive maintenance technologies to enhance equipment performance and reduce operating costs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.9 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Country

- 2.2.2 Product

- 2.2.3 Fuel

- 2.2.4 Class

- 2.2.5 End use

- 2.2.6 Distribution Channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth in e-commerce and warehousing

- 3.2.1.2 Industrial and manufacturing expansion

- 3.2.1.3 Technological advancements

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Regulatory compliance and safety standards

- 3.2.2.2 High initial investment

- 3.2.3 Opportunities

- 3.2.3.1 Robotics-as-a-service (RaaS) models lowering entry barriers

- 3.2.3.2 Retrofit & upgrade market for existing forklift fleets with IoT solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Regulatory landscape

- 3.7 Trade data analysis (HS Code: 8427) (Driven by paid database)

- 3.7.1 Import/export volume & value trends (driven by primary research)

- 3.7.2 Key trade corridors & tariff impact (driven by primary research)

- 3.8 Impact of AI & generative AI on the market

- 3.8.1 AI-driven disruption of existing business models

- 3.8.2 GenAI use cases & adoption roadmap by segment

- 3.8.3 Risks, limitations & regulatory considerations

- 3.9 Pricing Analysis (driven by primary research)

- 3.9.1 Historical price trend analysis (driven by primary research)

- 3.9.2 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Distribution Infrastructure & Channel Penetration Landscape (Driven by Primary Research)

- 3.12.1 Channel Coverage by Region & Format (Modern vs. Traditional Trade) (Driven by Primary Research)

- 3.12.2 Last-Mile Infrastructure Gaps & Emerging Channel Shifts

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By country

- 4.2.1.1 U.S.

- 4.2.1.2 Canada

- 4.2.1 By country

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Warehouse Forklifts

- 5.2.1 Narrow Aisle Trucks

- 5.2.2 Reach Trucks

- 5.2.3 Order Pickers

- 5.3 Counterbalance Forklifts

- 5.3.1 Stand-Up Models

- 5.3.2 Sit-Down Models

- 5.4 Rough Terrain Forklifts

- 5.4.1 Variable Reach (Telescoping Boom)

- 5.4.2 Vertical Mast Type

Chapter 6 Market Estimates & Forecast, By Fuel, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Diesel

- 6.3 Electric

- 6.4 Gasoline & LPG/CNG

Chapter 7 Market Estimates & Forecast, By Class, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Class I

- 7.3 Class II

- 7.4 Class III

- 7.5 Class IV

- 7.6 Class V

- 7.7 Class VI

- 7.8 Class VII

Chapter 8 Market Estimates & Forecast, By End Use, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Chemical

- 8.3 Food & beverages

- 8.4 Industrial

- 8.5 Logistics

- 8.6 Retail & e-commerce

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.2.1 Indirect sales

Chapter 10 Market Estimates & Forecast, By Country, 2022-2035 (USD Billion) (Million units)

- 10.1 Key trends

- 10.2 U.S.

- 10.3 Canada

Chapter 11 Company Profiles

- 11.1 Global Companies

- 11.1.1 Caterpillar Inc.

- 11.1.2 Crown Equipment Corporation

- 11.1.3 Hyster-Yale, Inc.

- 11.1.4 Jungheinrich AG

- 11.1.5 KION GROUP AG

- 11.1.6 Mitsubishi Logisnext Co., Ltd.

- 11.1.7 Toyota Material Handling North America

- 11.2 Regional Companies

- 11.2.1 Big Joe Forklifts

- 11.2.2 Clark Material Handling

- 11.2.3 Doosan Bobcat North America Inc.

- 11.2.4 Hoist Liftruck Manufacturing

- 11.2.5 Pettibone LLC

- 11.2.6 Sellick Equipment Limited

- 11.2.7 Taylor Forklifts

- 11.2.8 Titan Forklifts

- 11.3 Emerging Companies

- 11.3.1 Combilift

- 11.3.2 Fox Robotics

- 11.3.3 Guangxi LiuGong Machinery

- 11.3.4 Hubtex

- 11.3.5 Hyundai Material Handling

- 11.3.6 Manitou Group SA

- 11.3.7 Noblelift Intelligent Equipment