PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062401

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062401

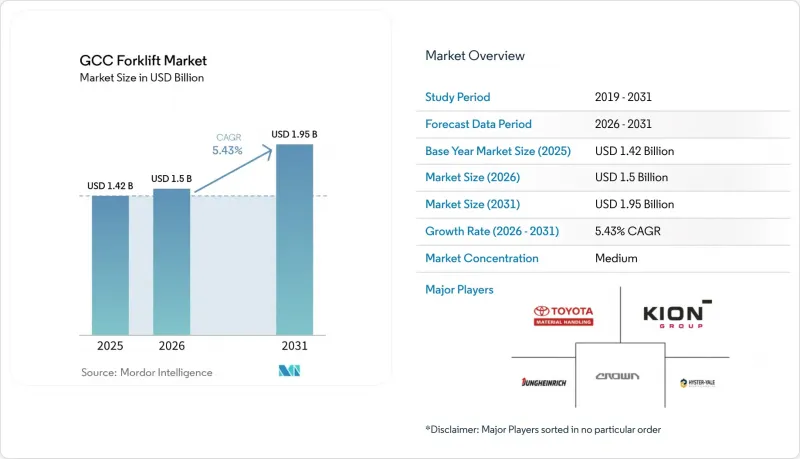

GCC Forklift - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the gCC forklift market size is expected to increase from USD 1.42 billion in 2025 to USD 1.50 billion in 2026 and reach USD 1.95 billion by 2031, growing at a CAGR of 5.43% over 2026-2031.

This report is Segmented by Power Source (Internal Combustion Engine, Electric), Forklift Class (Class 1 - Electric Rider, Class 2 - Electric Narrow-Aisle, and More), Tonnage Capacity (Below 5 Ton, 5-10 Ton, and More), End-User Industry (Logistics and Warehousing, Construction and Infrastructure, and More), Product Type, and Geography. Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

GCC Forklift Market Trends and Insights

Mega GCC Infrastructure Projects (Vision 2030 et al.)

Saudi Arabia's NEOM Port, backed by a significant investment, is set to revolutionize its operations. Phase 1 will see the installation of automated ship-to-shore cranes, complemented by numerous support forklifts. In a significant shift, the port is compressing the typical multi-year equipment replacement cycle into a much shorter purchasing window. Meanwhile, logistics for the Red Sea Project and the construction of the Qiddiya entertainment city are securing multi-year leases with local distributors. This strategy not only ensures uptime commitments but also skews procurement towards original equipment manufacturers (OEMs) that boast in-country service hubs. Furthermore, global brands, with their promise of expedited parts delivery, are seizing this heightened urgency, successfully capturing orders that sidestep the conventional spot purchasing methods historically linked to oil revenue.

E-commerce-led Warehouse Boom

Amazon operates a large fulfillment center in Riyadh, while KEZAD manages an expansive logistics park, both secured under long-term contracts spanning a decade. These contracts shield equipment demand from the volatility of oil prices. With the rising expectations for same-day deliveries, forklift density has significantly increased, making lithium-ion models, especially those with opportunity-charging capabilities, the top choice. As urban land costs climb, there's a pronounced push towards vertical storage. This trend has subsequently boosted the volumes of reach-trucks and order-pickers in the GCC forklift market.

Oil-price CAPEX Cyclicality

Saudi Aramco's decision to reduce its capital budget for 2026 signals a trend: petrochemical and oil-field contractors tend to postpone upgrades whenever Brent prices decline. This shift has extended their replacement cycles to a decade. Meanwhile, OEMs are turning to operating leases tied to crude indices, aiming to bring stability to the GCC forklift market.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Electric and Li-ion Forklifts

- 3PL and Cold-chain Expansion

- Forklift-operator Skills Shortage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electric forklifts held 69.13% share in 2025 and grew at 7.34% through 2031, underscoring the GCC forklift market shift toward lithium-ion economics. At Duqm Port, grid limitations led to the specification of diesel forklifts in 2025, underscoring the continued importance of internal-combustion units in outdoor settings. Battery-swap clauses, which transfer degradation costs to OEMs, help mitigate residual-value risks. Meanwhile, hydrogen fuel-cell trials at KAUST suggest a potential third pathway for the future.

Fleet operators are balancing the penalties of desert heat against capital rebates, favoring suppliers with local battery-refurbishment programs that complete the lifecycle loop. In the GCC forklift market, Chinese brands are gaining a competitive advantage by partnering with Dubatt, effectively reducing midlife replacement costs.

Class 4/5 cushion and pneumatic units retained 43.55% share in 2025, but Class 1 electric riders posted the fastest 8.04% CAGR. Amazon's Riyadh hub deployed several narrow-aisle units to double storage density, underscoring how warehouse layouts influence class selection. Class 3 pallet trucks also rise as labor regulators tighten ergonomic standards, converting manual jacks into powered models.

In port yards, Diesel Class 4/5 units are still essential. NEOM's gravel surfaces and the weights of containers necessitate the use of rough-terrain forklifts. With emission regulations on the horizon in 2027, diesel prices are expected to increase. This potential change is likely to hasten the shift towards electric forklifts in the GCC market.

List of Companies Covered in this Report:

- Toyota Industries Corporation (Toyota Material Handling)

- KION Group AG

- Jungheinrich AG

- Crown Equipment Corporation

- Mitsubishi Logisnext Ltd.

- Hyster-Yale Materials Handling, Inc.

- HD Hyundai Infracore Co., Ltd.

- Hangcha Group

- Anhui Heli Co., Ltd.

- Komatsu Ltd.

- Manitou Group

- Clark Material Handling Company

- Lonking Holdings Limited

- CAT Lift Trucks

- EP Equipment Co., Ltd.

- BYD Company Limited

- Combilift

- LiuGong Machinery

- Landoll Company

- SANY Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mega GCC Infrastructure Projects (Vision 2030 et al.)

- 4.2.2 E-commerce-led Warehouse Boom

- 4.2.3 Shift Toward Electric and Li-ion Forklifts

- 4.2.4 3PL and Cold-chain Expansion

- 4.2.5 Free-zone Port Corridors Driving High-capacity Demand

- 4.2.6 Autonomous Fulfilment Centers Adoption

- 4.3 Market Restraints

- 4.3.1 Oil-price CAPEX Cyclicality

- 4.3.2 Forklift-operator Skills Shortage

- 4.3.3 Harsh Desert Climate Accelerates TCO

- 4.3.4 Fragmented Battery-recycling Rules

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook (Electrification and Automation)

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size and Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Power Source

- 5.1.1 Internal Combustion Engine (ICE)

- 5.1.2 Electric

- 5.2 By Forklift Class

- 5.2.1 Class 1 - Electric Rider

- 5.2.2 Class 2 - Electric Narrow-aisle

- 5.2.3 Class 3 - Electric Hand/Rider

- 5.2.4 Class 4/5 - ICE Cushion and Pneumatic

- 5.3 By Tonnage Capacity

- 5.3.1 Below 5 Ton

- 5.3.2 5 - 10 Ton

- 5.3.3 Above 10 Ton

- 5.4 By End-user Industry

- 5.4.1 Logistics and Warehousing

- 5.4.2 Construction and Infrastructure

- 5.4.3 Manufacturing (Discrete and Process)

- 5.4.4 Retail and Wholesale

- 5.4.5 Oil and Gas/Petrochemicals

- 5.4.6 Others (Food-cold Chain, Airports)

- 5.5 By Product Type

- 5.5.1 Counterbalanced Forklifts

- 5.5.2 Warehouse Trucks (Reach, Order-picker, Pallet)

- 5.6 By Geography

- 5.6.1 Saudi Arabia

- 5.6.2 United Arab Emirates

- 5.6.3 Qatar

- 5.6.4 Kuwait

- 5.6.5 Oman

- 5.6.6 Bahrain

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Toyota Industries Corporation (Toyota Material Handling)

- 6.4.2 KION Group AG

- 6.4.3 Jungheinrich AG

- 6.4.4 Crown Equipment Corporation

- 6.4.5 Mitsubishi Logisnext Ltd.

- 6.4.6 Hyster-Yale Materials Handling, Inc.

- 6.4.7 HD Hyundai Infracore Co., Ltd.

- 6.4.8 Hangcha Group

- 6.4.9 Anhui Heli Co., Ltd.

- 6.4.10 Komatsu Ltd.

- 6.4.11 Manitou Group

- 6.4.12 Clark Material Handling Company

- 6.4.13 Lonking Holdings Limited

- 6.4.14 CAT Lift Trucks

- 6.4.15 EP Equipment Co., Ltd.

- 6.4.16 BYD Company Limited

- 6.4.17 Combilift

- 6.4.18 LiuGong Machinery

- 6.4.19 Landoll Company

- 6.4.20 SANY Group

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment