PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061474

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2061474

Antibody Therapy Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

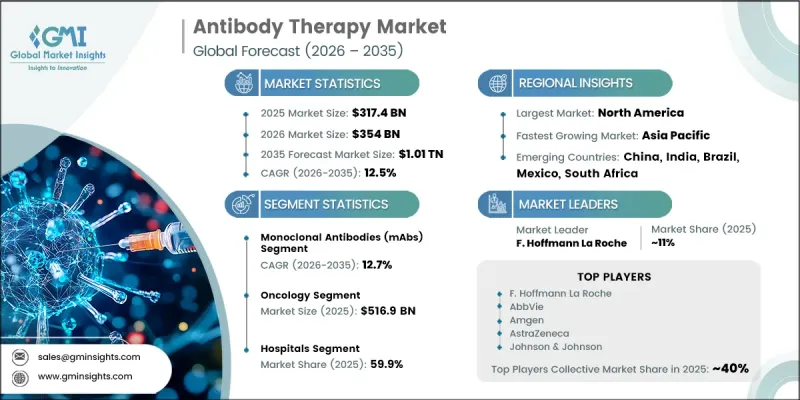

The Global Antibody Therapy Market was valued at USD 317.4 billion in 2025 and is estimated to grow at a CAGR of 12.5% to reach USD 1.01 trillion by 2035.

The market is experiencing substantial growth due to the increasing commercialization and regulatory approval of advanced antibody-based treatments across multiple therapeutic areas, including oncology, autoimmune disorders, infectious diseases, and neurological conditions. Growing demand for targeted biologic therapies, combined with rapid innovation in monoclonal antibodies, bispecific antibodies, and antibody-drug conjugates (ADCs), is significantly accelerating industry expansion. The strong clinical pipeline for antibody therapeutics, along with rising investments in biologics research and pharmaceutical innovation, continues to create lucrative opportunities for market participants. In addition, favorable regulatory support and the increasing number of approved antibody therapies are reinforcing market development globally. As healthcare providers increasingly prioritize precision medicine and targeted treatment strategies, antibody therapies are becoming a critical component of modern disease management. Technological advancements in recombinant biotechnology, protein engineering, and next-generation biologic platforms are also enhancing treatment effectiveness, improving patient outcomes, and strengthening long-term market potential.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $317.4 Billion |

| Forecast Value | $1.01 Trillion |

| CAGR | 12.5% |

Antibody therapy represents a highly targeted treatment approach that uses monoclonal antibodies to identify and attach to specific antigens linked to disease-causing cells or pathogens. These therapies are extensively utilized across cancer treatment, inflammatory diseases, autoimmune conditions, and infectious disease management because of their precision, therapeutic efficiency, and improved safety profile. By selectively targeting abnormal cells while reducing damage to healthy tissues, antibody-based therapies have become an essential element of precision medicine and advanced biologic treatment approaches. The growing focus on personalized healthcare solutions and targeted therapeutic interventions is further supporting widespread adoption of antibody therapies across global healthcare systems.

The monoclonal antibodies segment is anticipated to register a CAGR of 12.7% during 2025. Segment growth is largely driven by the expanding use of monoclonal antibodies in treating chronic illnesses, including cancer, autoimmune diseases, infectious disorders, and genetic conditions. Monoclonal antibodies provide highly precise therapeutic activity while generating strong immune-mediated responses that improve treatment effectiveness and clinical outcomes. Ongoing developments in recombinant DNA technologies, antibody engineering, protein modification techniques, and advanced biologic manufacturing platforms are accelerating the introduction of next-generation monoclonal antibody therapies. These innovations continue to support strong growth within the segment while increasing the clinical relevance of antibody-based therapeutics across healthcare applications.

The oncology segment is projected to reach USD 516.9 billion by 2035. The segment continues to dominate the antibody therapy market due to increasing use of monoclonal antibodies, antibody-drug conjugates, and bispecific antibodies in cancer treatment. Rising global cancer incidence and growing demand for highly targeted therapies with improved safety and efficacy profiles are driving widespread adoption of antibody-based oncology treatments. Significant investments in oncology research and development, rapid expansion of cancer-focused clinical pipelines, and continuous regulatory approvals for innovative biologic therapies are further strengthening segment growth. In addition, advancements in biomarker-based treatment approaches and precision oncology are improving the effectiveness and utilization of antibody therapies within cancer care settings.

North America Antibody Therapy Market accounted for 41.5% share in 2025. Regional growth is supported by strong investment in biologics research, a favorable regulatory environment, and increasing development of innovative antibody therapeutics by major biotechnology and pharmaceutical companies. The presence of advanced healthcare infrastructure, strong reimbursement frameworks, and rapid adoption of advanced biologic treatments continues to reinforce North America's leadership position in the market. Additionally, the increasing prevalence of chronic diseases, cancer, autoimmune disorders, and inflammatory conditions throughout the region is contributing to sustained demand for antibody-based therapies.

Major companies operating in the Global Antibody Therapy Market include Pfizer, AstraZeneca, AbbVie, Bristol Myers Squibb Company, Eli Lilly and Company, Regeneron Pharmaceuticals, Novartis, Johnson & Johnson, Takeda Pharmaceutical Company, Merck & Co., GlaxoSmithKline, F. Hoffmann La Roche, Amgen, Sanofi, and Seagen. Companies operating in the antibody therapy market are adopting multiple strategic initiatives to strengthen their competitive position and expand their global presence. Leading pharmaceutical and biotechnology firms are increasing investments in research and development to accelerate the discovery of next-generation antibody therapies, including bispecific antibodies and antibody-drug conjugates. Strategic collaborations, licensing agreements, and acquisitions are being widely utilized to strengthen product pipelines and expand technological capabilities. Many companies are also focusing on expanding manufacturing capacity and improving biologics production efficiency to meet growing global demand. In addition, organizations are prioritizing precision medicine strategies, biomarker-driven therapies, and advanced clinical trial programs to improve treatment outcomes and regulatory success rates.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Type trends

- 2.2.3 Application trends

- 2.2.4 Source trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic and infectious disease worldwide

- 3.2.1.2 Growing R&D activities

- 3.2.1.3 High rate of adoption and approval in the U.S. and Europe

- 3.2.1.4 Booming biologics industry

- 3.2.1.5 Rising applications of antibody therapy

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High cost of some monoclonal antibody therapeutics

- 3.2.2.2 Complex manufacturing processes and logistical challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into next-generation antibody formats

- 3.2.3.2 Growth opportunities in emerging and underpenetrated markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology and innovation landscape (Driven by Primary Research)

- 3.5.1 Current technological trends

- 3.5.1.1 Monoclonal antibody (mAb) engineering and optimization

- 3.5.1.2 Antibody-drug conjugate (ADC) platform technologies

- 3.5.2 Emerging technologies

- 3.5.2.1 Bispecific and multispecific antibody platforms

- 3.5.2.2 Radiolabeled and advanced targeted antibody therapeutics

- 3.5.1 Current technological trends

- 3.6 Pipeline products (Driven by Primary Research)

- 3.6.1 Monoclonal antibodies

- 3.6.2 Antibody drug conjugates

- 3.7 Pricing analysis

- 3.8 Impact of AI and Gen AI on the market

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 ($ Mn)

- 5.1 Key trends

- 5.2 Monoclonal antibodies (mAbs)

- 5.3 Antibody-drug conjugates (ADCs)

- 5.4 Other types

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 ($ Mn)

- 6.1 Key trends

- 6.2 Oncology

- 6.3 Infectious diseases

- 6.4 Neurological diseases

- 6.5 Autoimmune & inflammatory diseases

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By Sources, 2022-2035 ($ Mn)

- 7.1 Key trends

- 7.2 Chimeric

- 7.3 Murine

- 7.4 Fully human

- 7.5 Humanized

Chapter 8 Market Estimates and Forecast, By End Use, 2022-2035 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Specialty centers

- 8.4 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East & Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AbbVie

- 10.2 Amgen

- 10.3 AstraZeneca

- 10.4 Bristol Myers Squibb Company

- 10.5 Eli Lilly and Company

- 10.6 F. Hoffmann La Roche

- 10.7 GlaxoSmithKline

- 10.8 Johnson & Johnson

- 10.9 Merck & Co.

- 10.10 Novartis

- 10.11 Pfizer

- 10.12 Regeneron Pharmaceuticals

- 10.13 Sanofi

- 10.14 Seagen

- 10.15 Takeda Pharmaceutical Company