PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072862

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072862

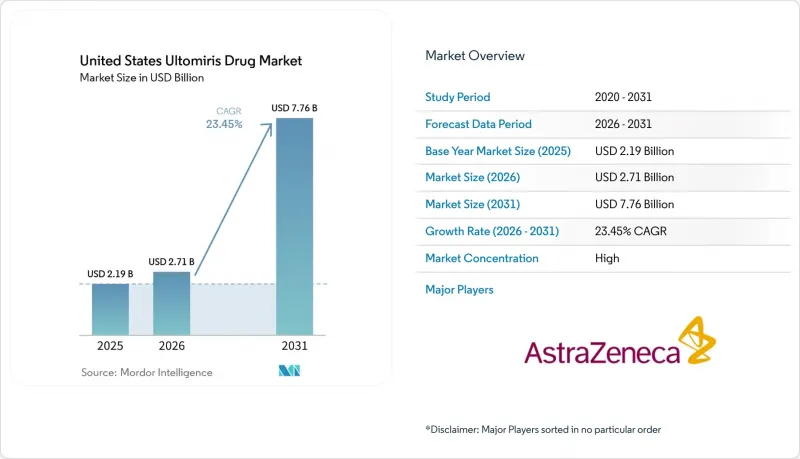

United States Ultomiris Drug - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states ultomiris drug market size was valued at USD 2.19 billion in 2025 and is estimated to grow from USD 2.71 billion in 2026 to reach USD 7.76 billion by 2031, at a CAGR of 23.45% during the forecast period (2026-2031).

This report is Segmented by Indication (Paroxysmal Nocturnal Hemoglobinuria, Atypical Hemolytic Uremic Syndrome, Generalized Myasthenia Gravis, Neuromyelitis Optica Spectrum Disorder), End Use (Adult, Pediatric), and Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, Other Distribution Channels). The Market Forecasts are Provided in Terms of Value (USD).

United States Ultomiris Drug Market Trends and Insights

Extended Dosing Interval and Lower Treatment Burden

The United States Ultomiris drug market benefits from ravulizumab's every-8-week intravenous maintenance schedule, which reduces annual treatment visits to 6 to 7 compared with 26 for eculizumab under a biweekly approach. That change matters in daily practice because fewer visits reduce scheduling strain for patients, caregivers, infusion centers, and physician offices that already manage rare and complex cases. In the United States Ultomiris drug market, this lower treatment burden supports persistence, which is especially important in diseases where therapy is long term and discontinuation can have serious clinical consequences. The value of that convenience is stronger in working-age populations, and the claims-based U.S. analysis placed the median age for treated PNH patients at 40 years. The dosing advantage has therefore moved from being a product attribute to a practical benchmark for how new C5 therapies are judged in routine care.

Expanding Approved Indications in Hematology and Neurology

The United States Ultomiris drug market is supported by 4 active FDA-approved indications, PNH, aHUS, gMG, and NMOSD, which gives ravulizumab broader label coverage than any other single C5 inhibitor in the country. This breadth matters because growth in ultra-rare biologics depends more on moving into adjacent indications than on underlying epidemiology alone. In gMG, post-approval uptake is being reinforced by ongoing real-world registry updates that remain consistent with the durable outcomes seen in the CHAMPION MG clinical program. In NMOSD, trial results showed a 98.9% relative relapse risk reduction versus placebo, which gives prescribers and payers a strong rationale in a condition where a single relapse can cause lasting disability. Across the United States Ultomiris drug market, the combined hematology and neurology label now acts as the main engine for future patient additions.

High Annual Therapy Cost and Payer Scrutiny

Cost remains a direct brake on the United States Ultomiris drug market because treated patients generate very high annual spending under both public and commercial coverage. The analysis reported total PNH-related costs of USD 660,533 in year 1 and USD 633,984 in subsequent years, which shows how drug, monitoring, and care intensity combine into a difficult payer burden. Commercial plans are responding by tightening utilization controls, and UnitedHealthcare's 2026 complement inhibitor policy places biosimilar eculizumab products inside the decision path for new treatment starts. That does not eliminate class demand, but it can delay therapy initiation and shift the timing of revenue recognition inside a plan year. The United States Ultomiris drug market therefore faces a ceiling from payer affordability even while underlying clinical demand remains strong.

Other drivers and restraints analyzed in the detailed report include:

- Conversion From Soliris to Ultomiris in Established Patients

- SC Self-Administration Expands Site-of-Care Flexibility

- Serious Meningococcal Infection Risk and REMS Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PNH held 48.31% of the indication mix in 2025, which gave it the largest position in the United States Ultomiris drug market share at the indication level. That lead reflects the longest reimbursement history, the deepest prescriber familiarity, and the most established treatment workflows for complement inhibition. The analysis also described a diagnosed prevalent U.S. PNH population of 6,200 cases and noted that only 30% of insured patients had historically been captured on complement inhibitor therapy, which shows why PNH revenue remains driven by price per treated patient rather than by large patient numbers. Within the United States Ultomiris drug industry, that concentration leaves PNH commercially important but also more exposed to biosimilar-related payer pressure than newer uses.

Generalized myasthenia gravis is projected to record the fastest indication growth at a 24.38% CAGR from 2026 to 2031, and that pace reflects broader eligibility and growing neurologist familiarity after FDA approval. The United States Ultomiris drug market size for gMG is rising because real-world registry updates continue to support durable outcomes aligned with the clinical program AAN2025. NMOSD remains smaller on patient volume because treatment is limited to AQP4 antibody-positive disease, yet its clinical severity gives the product a strong value case when relapse prevention can preserve long-term function. Across the United States Ultomiris drug industry, orphan exclusivity and the lack of near-term biosimilar competition in gMG and NMOSD support continued expansion of neurology-based revenue.

Complete Report Scope:

- By Indication

- Paroxysmal Nocturnal Hemoglobinuria

- Atypical Hemolytic Uremic Syndrome

- Generalized Myasthenia Gravis

- Neuromyelitis Optica Spectrum Disorder

- By End Use

- Adult

- Pediatric

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Other Distribution Channels

List of Companies Covered in this Report:

- AstraZeneca

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Extended Dosing Interval and Lower Treatment Burden

- 4.2.2 Expanding Approved Indications in Hematology and Neurology

- 4.2.3 Conversion From Soliris to Ultomiris in Established Patients

- 4.2.4 SC Self-Administration Expands Site-of-Care Flexibility

- 4.2.5 Broader Diagnostic Capture in Rare Complement-Mediated Diseases

- 4.2.6 Near-Term Pipeline Readouts Could Expand Nephrology Use Cases

- 4.3 Market Restraints

- 4.3.1 High Annual Therapy Cost and Payer Scrutiny

- 4.3.2 Serious Meningococcal Infection Risk and REMS Burden

- 4.3.3 Small Patient Pool Across Approved Orphan Indications

- 4.3.4 Infusion and Prior Authorization Friction in Specialty Care

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Indication

- 5.1.1 Paroxysmal Nocturnal Hemoglobinuria

- 5.1.2 Atypical Hemolytic Uremic Syndrome

- 5.1.3 Generalized Myasthenia Gravis

- 5.1.4 Neuromyelitis Optica Spectrum Disorder

- 5.2 By End Use

- 5.2.1 Adult

- 5.2.2 Pediatric

- 5.3 By Distribution Channel

- 5.3.1 Hospital Pharmacies

- 5.3.2 Retail Pharmacies

- 5.3.3 Online Pharmacies

- 5.3.4 Other Distribution Channels

6 Competitive Landscape

- 6.1 Pipeline Analysis

- 6.2 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Products, Recent Developments)

- 6.2.1 AstraZeneca PLC

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment