PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071222

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071222

Urban Air Mobility (UAM) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

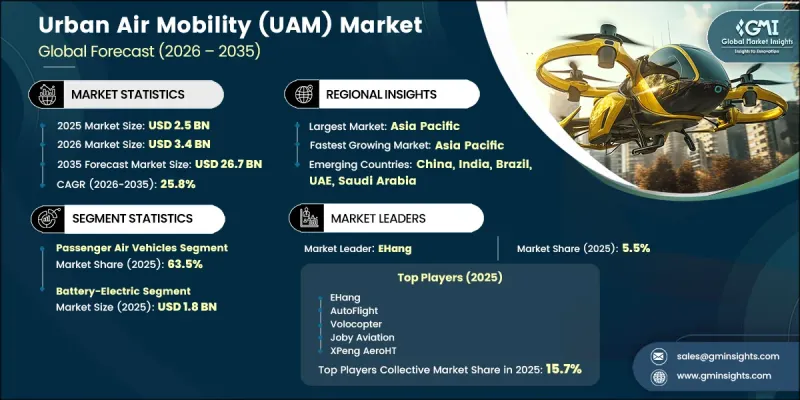

The Global Urban Air Mobility Market was valued at USD 2.5 billion in 2025 and is estimated to grow at a CAGR of 25.8% to reach USD 26.7 billion by 2035.

The rapid evolution of advanced aerial transportation solutions is creating significant growth opportunities across the urban air mobility industry. Increasing demand for faster transportation alternatives in congested metropolitan areas is encouraging the adoption of innovative air mobility platforms designed to improve travel efficiency and reduce transit times. Advancements in next-generation aviation technologies, coupled with supportive regulatory frameworks, are accelerating the path toward commercial deployment. Growing financial investments and strategic collaborations among industry participants are further strengthening market development by supporting technology maturation and operational readiness. The industry is also benefiting from rising emphasis on sustainable transportation solutions and reduced environmental impact, encouraging the adoption of cleaner mobility technologies. As urban transportation systems continue to evolve, stakeholders are increasingly investing in infrastructure, vehicle development, and ecosystem integration initiatives that support long-term commercialization. The convergence of technological innovation, favorable policy support, and increasing demand for efficient mobility services is expected to drive sustained growth across the global urban air mobility market throughout the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.5 Billion |

| Forecast Value | $26.7 Billion |

| CAGR | 25.8% |

The urban air mobility market is gaining momentum as rising traffic congestion and growing pressure on urban transportation networks increase demand for alternative mobility solutions. Market expansion is being supported by the ongoing development of the infrastructure required to enable large-scale deployment of advanced air transportation services. Continued investments in operational ecosystems are facilitating the transition from development stages to commercial implementation. Collaboration among aerospace companies, technology providers, infrastructure developers, and regulatory stakeholders is accelerating technology advancement, improving deployment efficiency, and strengthening confidence in emerging mobility platforms. Increasing capital investment and industry-wide partnerships continue to play a critical role in scaling urban air mobility operations and supporting long-term market growth. Infrastructure development remains one of the most influential trends shaping the industry, as dedicated facilities and supporting networks become essential for integrating air mobility services into broader transportation systems. The expansion of these capabilities is expected to enhance operational efficiency and support wider adoption over the coming years.

The passenger air vehicles segment held a 63.5% share in 2025. Strong demand for advanced passenger transportation solutions continues to drive growth within this segment as cities seek more efficient ways to address increasing mobility challenges. Passenger-focused air vehicles are receiving significant attention from operators and public authorities due to their potential to improve transportation efficiency and reduce travel times. Their growing incorporation into interconnected transportation networks and increasing focus on commercial passenger operations continue to strengthen the segment's leading market position.

The hydrogen fuel cell segment is projected to grow at a CAGR of 29% during 2026-2035. The segment's growth is being driven by its capability to deliver greater energy efficiency and extended operational range compared to alternative propulsion technologies. Hydrogen-based systems support longer-duration operations while accommodating increased payload requirements, making them well suited for a broader range of mobility applications. Growing interest in clean energy technologies and sustainable aviation solutions is further accelerating adoption, positioning hydrogen fuel cells as an important technology segment within the evolving urban air mobility landscape.

North America Urban Air Mobility Market accounted for 36.5% share in 2025. Regional growth is being supported by the presence of established aerospace innovators and ongoing progress toward the commercial deployment of advanced aerial transportation platforms. Continued testing activities, certification advancements, and alignment with aviation safety requirements are helping accelerate the transition from development to operational implementation. The market is also benefiting from strong governmental support and coordinated efforts focused on advancing air mobility initiatives. Regulatory guidance, infrastructure planning efforts, and airspace management programs are contributing to a more streamlined commercialization pathway, strengthening North America's position as a leading market for urban air mobility technologies.

Key companies operating in the Global Urban Air Mobility Market include Archer Aviation, Joby Aviation, Vertical Aerospace, EHang, Beta Technologies, Volocopter, Wisk Aero, AutoFlight, XPeng AeroHT, SkyDrive, and Electra.aero, Overair, Elroy Air, Dronamics, Pipistrel, TCab Tech, Volant Aerotech, Doroni Aerospace, Apeleon, Aergility, Natilus, and Jump Aero. Companies participating in the urban air mobility industry are pursuing a variety of strategic initiatives to strengthen their market position and expand their competitive advantage. Research and development investments remain a primary focus as manufacturers work to enhance aircraft performance, operational safety, energy efficiency, and commercial viability. Strategic collaborations with aerospace organizations, infrastructure developers, technology providers, and regulatory stakeholders are helping accelerate product development and market entry. Companies are also prioritizing certification milestones and operational readiness programs to support commercialization efforts. Expanding production capabilities, strengthening supply chain networks, and developing integrated mobility ecosystems are further supporting growth strategies. In addition, organizations are investing in advanced propulsion technologies, digital flight systems, and infrastructure partnerships to improve service scalability.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Platform type trends

- 2.2.2 Propulsion type trends

- 2.2.3 Operation mode trends

- 2.2.4 Operational range trends

- 2.2.5 End User trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing urban congestion and demand for faster transportation

- 3.2.1.2 Advancements in eVTOL and autonomous light technologies

- 3.2.1.3 Growing government support and regulatory development

- 3.2.1.4 Rising investments and strategic partnerships

- 3.2.1.5 Increasing focus on sustainable and low-emission transportation

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High infrastructure development and operational costs

- 3.2.2.2 Regulatory uncertainty and airspace integration complexity

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption in logistics and emergency services

- 3.2.3.2 Expansion of inter-city and regional air mobility services

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Platform Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Passenger air vehicles

- 5.2.1 Air taxis

- 5.2.2 Air shuttles

- 5.2.3 Personal air vehicles

- 5.3 Cargo air vehicles

- 5.3.1 Last-mile delivery vehicles

- 5.3.2 Heavy cargo UAVs

- 5.4 Specialized service vehicles

- 5.4.1 Air ambulance

- 5.4.2 Emergency/disaster support

Chapter 6 Market Estimates and Forecast, By Propulsion Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Battery-electric

- 6.3 Hybrid-electric

- 6.4 Hydrogen fuel cell

Chapter 7 Market Estimates and Forecast, By Operation Mode, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Piloted operations

- 7.3 Semi-autonomous / remotely supervised operations

- 7.4 Fully autonomous operations

Chapter 8 Market Estimates and Forecast, By Operational Range, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Short range (0-50km)

- 8.3 Medium range (50-150km)

- 8.4 Long range (150-300km)

Chapter 9 Market Estimates and Forecast, By End User, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Commercial mobility operators

- 9.3 Logistics operators

- 9.4 Medical & emergency agencies

- 9.5 Private/corporate operators

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 EHang

- 11.1.2 AutoFlight

- 11.1.3 Volocopter

- 11.1.4 Joby Aviation

- 11.1.5 XPeng AeroHT

- 11.2 Regional key players

- 11.2.1 North America

- 11.2.1.1 Wisk Aero

- 11.2.1.2 Archer Aviation

- 11.2.1.3 Beta Technologies

- 11.2.1.4 Electra.aero

- 11.2.1.5 Overair

- 11.2.1.6 Elroy Air

- 11.2.1.7 Doroni Aerospace

- 11.2.1.8 Jump Aero

- 11.2.1.9 Natilus

- 11.2.2 Asia Pacific

- 11.2.2.1 SkyDrive

- 11.2.2.2 TCab Tech

- 11.2.2.3 Volant Aerotech

- 11.2.3 Europe

- 11.2.3.1 Vertical Aerospace

- 11.2.3.2 Pipistrel

- 11.2.3.3 Dronamics

- 11.2.4 Middle East & Africa

- 11.2.4.1 Apeleon

- 11.2.4.2 Aergility

- 11.2.1 North America