PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071233

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071233

Latin America Water Purifier Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

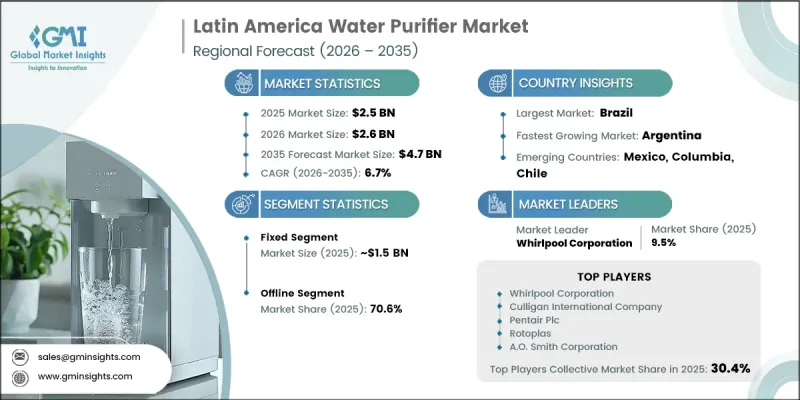

Latin America Water Purifier Market was valued at USD 2.5 billion in 2025 and is estimated to grow at a CAGR of 6.7% to reach USD 4.7 billion by 2035.

Growth is fueled by worsening freshwater contamination caused by industrial discharge and agricultural runoff, which continues to strain already limited municipal water treatment systems. As a result, households are increasingly turning to independent purification solutions to ensure safe drinking water access. Rising health awareness among consumers is also reshaping purchasing behavior, positioning water purifiers as essential household necessities rather than optional appliances. Rapid urbanization across major cities is further intensifying pressure on infrastructure, creating sustained demand for point-of-use filtration systems as municipal expansion struggles to keep pace with population growth. These combined structural factors are reinforcing long-term market expansion across both urban and semi-urban regions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.5 Billion |

| Forecast Value | $4.7 Billion |

| CAGR | 6.7% |

The fixed water purifier segment generated USD 1.5 billion in 2025 and is forecast to reach USD 2.8 billion by 2035. This category remains the leading product type due to its advanced filtration efficiency and multi-stage purification capabilities. Fixed systems commonly integrate technologies such as reverse osmosis, ultraviolet treatment, and activated carbon filtration, making them highly effective for residential applications requiring consistent water quality improvement.

The offline distribution channel accounted for 70.6% share in 2025, maintaining its leading position. Consumers continue to prefer physical retail outlets for water purification systems due to the technical nature of the product. Buyers often evaluate build quality, installation requirements, and product dimensions firsthand before making a purchase decision, particularly for long-term household investments where performance reliability is critical.

Brazil Water Purifier Market held a 44.1% share in 2025. Its leadership is supported by a large population base and a growing urban middle class that is increasingly investing in household water purification solutions. Rising concerns about water contamination in major urban centers, combined with inconsistent municipal water supply quality, have significantly increased adoption rates. Strong distribution networks and the presence of both domestic and international manufacturers further strengthen market accessibility and penetration.

Key companies operating in the Latin America water purifier market include Xylem Inc., Whirlpool Corporation, LG Electronics Inc., Pentair Plc, Veolia Water Technologies, Culligan International Company, A.O. Smith Corporation, Brita LP, Amway Corporation (eSpring brand), Helen of Troy Limited (PUR brand), Panasonic Corporation, Grupo Rotoplas S.A.B. de C.V., 3M Company, Watts Water Technologies Inc., Aquatech International, Electrolux do Brasil S.A., Ulfer Ind. e Com. de Filtros Ltda., Europa Filtros (Brasfilter), PURA Mexico, Remote Waters S.A., and Acuario (acuario.io). Market participants are strengthening their position through product innovation, expanding distribution networks, and localized manufacturing strategies. Companies are focusing on advanced filtration technologies that enhance water safety, improve energy efficiency, and extend product lifespan. Strategic partnerships with retail distributors and service providers are helping firms improve market reach across urban and semi-urban regions. Manufacturers are also investing in awareness campaigns to educate consumers on water quality risks, thereby driving product adoption. In addition, firms are offering flexible pricing models and bundled maintenance services to increase affordability and customer retention.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Country

- 2.2.2 Product Type

- 2.2.3 Technology

- 2.2.4 Capacity

- 2.2.5 Price

- 2.2.6 Application

- 2.2.7 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising awareness about purified water

- 3.2.1.2 Increasing industrial activities

- 3.2.1.3 Rising concerns about contaminants and waterborne diseases

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High maintenance cost of filters

- 3.2.2.2 Lack of awareness in rural areas

- 3.2.3 Opportunities

- 3.2.3.1 Rental/service model expansion across Brazil & Mexico

- 3.2.3.2 Demand for smart & IoT-enabled purifiers among urban consumers

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory framework

- 3.4.1 National Standards & Compliance Requirements

- 3.4.2 Regional Regulatory Harmonization Trends

- 3.4.3 Certification Standards (NSF/ANSI, ABNT, NOM)

- 3.4.4 Government Water Safety Initiatives (Brazil "Water for All" - BRL 30.8B, CONAGUA Mexico)

- 3.4.5 Impact of Regulatory Changes on Market Entry

- 3.5 Major market trends and disruptions

- 3.6 Technology/innovation landscape

- 3.6.1 Current trends

- 3.6.2 Emerging trends

- 3.7 Pricing Analysis (driven by primary research)

- 3.7.1 Historical price trend analysis (driven by primary research)

- 3.7.2 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.8 Future market trends

- 3.9 Trade data analysis (driven by paid database) (HS Code- 8421)

- 3.9.1 Import/export volume & value trends (driven by primary research)

- 3.9.2 Key trade corridors & tariff impact (driven by primary research)

- 3.10 Impact of AI & Generative AI on the Market

- 3.10.1 AI-driven disruption of existing business models

- 3.10.2 Gen-AI use cases & adoption roadmap by segment

- 3.10.3 Risks, limitations & regulatory considerations

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

- 3.13 Distribution infrastructure & channel penetration landscape (driven by primary research)

- 3.13.1 Channel coverage by country & format (modern vs traditional trade)

- 3.13.2 Last-mile infrastructure gaps & emerging channel shifts

- 3.14 Consumer behaviour analysis

- 3.14.1 Purchasing patterns

- 3.14.2 Preference analysis

- 3.14.3 Regional variations in consumer behaviour

- 3.14.4 Impact of e-commerce on buying decision

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By country

- 4.2.1.1 Brazil

- 4.2.1.2 Mexico

- 4.2.1.3 Argentina

- 4.2.1.4 Chile

- 4.2.1.5 Colombia

- 4.2.1.6 Rest of Latin America

- 4.2.1 By country

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Fixed

- 5.2.1 Wall-Mounted Systems

- 5.2.2 Under-the-Sink / Countertop Systems

- 5.2.3 Whole-Building/Commercial Fixed Units

- 5.3 Portable

- 5.3.1 Pitcher & Gravity-Fed Units

- 5.3.2 Personal/Bottle Portable Purifiers

- 5.3.3 Outdoor & Emergency Portable System

Chapter 6 Market Estimates & Forecast, By Technology, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 UV (Ultraviolet) Latin America Water Purifiers

- 6.3 RO (Reverse Osmosis) Latin America Water Purifiers

- 6.4 Gravity-Based Latin America Water Purifiers

- 6.5 Activated Carbon Filters

- 6.6 Ultrafiltration (UF) Systems

- 6.7 Others (Distillation, Nanofiltration, Multi-Stage Hybrid)

Chapter 7 Market Estimates & Forecast, By Capacity, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Small (Below 5L)

- 7.3 Medium (5L to 10L)

- 7.4 High (Above 10L)

Chapter 8 Market Estimates & Forecast, By Price, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Low

- 8.3 Medium

- 8.4 High

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial

- 9.4 Industrial

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Offline

- 10.3 Online

Chapter 11 Market Estimates & Forecast, By Country, 2022-2035 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 Brazil

- 11.3 Mexico

- 11.4 Argentina

- 11.5 Chile

- 11.6 Colombia

- 11.7 Rest of LA

Chapter 12 Company Profiles

- 12.1 Global Companies

- 12.1.1 3M Company

- 12.1.2 A.O. Smith Corporation

- 12.1.3 Culligan International Company

- 12.1.4 LG Electronics Inc.

- 12.1.5 Panasonic Corporation

- 12.1.6 Pentair Plc

- 12.1.7 Whirlpool Corporation

- 12.2 Regional Companies

- 12.2.1 Aquatech International

- 12.2.2 Electrolux do Brasil S.A.

- 12.2.3 Grupo Rotoplas S.A.B. de C.V.

- 12.2.4 Helen of Troy Limited (PUR brand)

- 12.2.5 Veolia Water Technologies

- 12.2.6 Watts Water Technologies Inc.

- 12.2.7 Xylem Inc.

- 12.3 Emerging Companies

- 12.3.1 Acuario

- 12.3.2 Amway Corporation (eSpring brand)

- 12.3.3 Brita LP

- 12.3.4 Europa Filtros (Brasfilter)

- 12.3.5 PURA Mexico

- 12.3.6 Remote Waters S.A.

- 12.3.7 Ulfer Ind. e Com. de Filtros Ltda.