PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062055

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062055

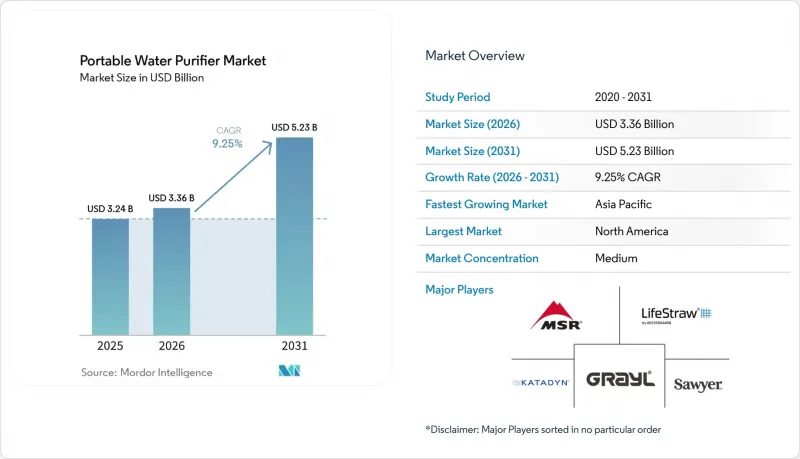

Portable Water Purifier - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the portable water purifier market size is projected to expand from USD 3.24 billion in 2025 and USD 3.36 billion in 2026 to USD 5.23 billion by 2031, registering a CAGR of 9.25% between 2026 and 2031.

This report is Segmented by Product Type (Extrusion, Pump, Suction Water Purifier, and More), Technology (Gravity, UV, RO Purifier, and More), End-User (Residential, Commercial), Distribution Channel (B2C/Retail and B2B/Directly From Manufacturers), and Geography (North America, South America, Asia-Pacific, Europe, Middle East & Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Portable Water Purifier Market Trends and Insights

Rising Adventure Tourism and Off-Grid Activities Drive Demand for Portable Water Purifiers

Outdoor spending rose as travelers returned to multi-day hiking, overlanding, paddling, and car-camping itineraries in 2025 and into 2026. These trips require dependable, compact treatment that adapts to variable water sources across changing terrain. LifeStraw's Peak Series 3-in-1 kit reflects this use-case shift, enabling straw, squeeze, or gravity configurations with a reported flow rate of 3 liters per minute and up to 2,000 liters of membrane life, improving pack efficiency for solo and small groups. This category convergence favors modular systems that expand capability without adding bulk, supporting both trek-ready and basecamp needs in one SKU. The portable water purifier market benefits as buyers standardize on one kit that travels from local day hikes to international excursions. As retailers highlight versatility, buyers weigh flow rate, service life, and virus removal more than brand legacy, intensifying product comparisons and narrowing choices to certified offerings.

Emergency Preparedness and Disaster Response Funding Prioritizes Portable Treatment

Government allocations for disaster stockpiles have increased following high-profile water-main failures, hurricane-driven contamination events, and wildfire disruptions to municipal treatment plants. Katadyn's September 2025 Aquifer 3000 desalination system, designed for two-person carry and MIL-STD-810H compliance, addresses this procurement shift by delivering 3,000 gallons per day from seawater or brackish sources without grid electricity, a specification unattainable by earlier-generation pump filter. The portable water purifier market is tightening its compliance posture to address bid criteria that emphasize microbiological performance and ruggedization over consumer aesthetics. Buyers increasingly evaluate total time to potable output and the resources required to maintain throughput during multi-day outages. This channel's growth is reinforced by resilience planning that treats purified water access as a critical service to be restored early in incident response. As preparedness programs broaden, suppliers that demonstrate certification depth and reliable supply for replacement parts are moving up procurement shortlists.

Flow Rate and Clogging Tradeoffs Limit Repeat Use

Users face slower flow as pore sizes tighten to capture smaller organisms, which raises the likelihood of clogging in sediment-rich sources. Pump purifiers with self-cleaning features can help preserve throughput, and some models maintain reported flow rates while extending service life through backflush cycles that purge trapped contaminants. Gravity systems without automated cleaning require more frequent maintenance, which deters casual users who expect appliance-like reliability. Complaints linked to slow flow or rapid clogging after turbid source exposure point to a knowledge gap about pre-filters and rinse protocols. Suppliers and retailers are addressing this through clearer maintenance guidance and by integrating field-cleanable elements that support extended service life. Ceramic and hollow fiber technologies remain susceptible to freeze damage, which further complicates winter use and underscores the need for user education about cold-weather handling.

Other drivers and restraints analyzed in the detailed report include:

- Rising Awareness of Backcountry Pathogens and Boil-Water Advisories

- PFAS Regulation and Chemical Contaminant Concerns Elevate Demand for Certified Claims

- Many Filters do not Address Viruses or PFAS, Creating Trust Gaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The extrusion water purifier segment held a 34.6% share in 2025, while UV pen purifiers are expanding at 11.4% CAGR through 2031. This split reflects two distinct use cases in the portable water purifier market. Extrusion designs appeal to users who want mechanical simplicity with direct pressure via squeeze, pump, or plunger actions. These systems are valued for durability and compatibility with dirty sources, which makes them staples for extended trips that draw from variable water bodies. Ultralight hikers and frequent flyers are driving UV pen adoption due to its small form factor and speed. This group prioritizes minimal pack weight and rapid treatment in clear sources where UV can work as intended. As labels highlight certifications and maintenance intervals, shoppers compare lifetime cost alongside flow and weight, which nudges the portable water purifier market toward modular systems with replaceable stages.

UV pen purifiers have improved ergonomics and battery management, which increases appeal for travel and backup roles. SteriPEN's Ultralight and Ultra models present quick treatment cycles and are positioned for use in clear water, with guidance to pre-filter turbid sources before UV exposure to maintain efficacy. Users value fast cycles and lack of consumable filters, while understanding cold weather effects on lithium-ion performance. The portable water purifier industry is refining product lines to match these preferences by adding simple water sensing safeguards, readable status displays, and consistent USB charging. At the same time, squeeze and pump variants retain share among users who want virus-rated stages or in-line carbon that can reduce chemicals and improve taste. The category's segmentation reflects how consumers optimize around their likely water sources and trip profiles rather than the brand alone.

Gravity purifiers led technology adoption with a 38.7% share in 2025, supported by their hands-free operation and ability to fill containers while users attend to other tasks. Throughput varies by membrane age and water conditions, yet simplicity remains the draw for family camping, paddling, and group trips. RO purifiers are growing at a 10.8% CAGR off a smaller base, a sign of rising interest in broader contaminant coverage in portable formats. Battery-operated and countertop portable RO models sit between home under-sink units and backcountry filters, meeting a preparedness use case that values PFAS and virus reduction in a device that can travel. This performance positioning is central for buyers who view the portable water purifier market as a path to reduce bottled water reliance in outages. As product teams tune power consumption and cartridge replacement cycles, the value story blends removal breadth with manageable upkeep in off-grid conditions.

Standards and guidance continue to shape technology selection. EPA identifies granular activated carbon, anion exchange, RO, and nanofiltration among the technologies capable of reducing PFAS, which informs engineering tradeoffs and certification plans. NSF/ANSI 55-2024 also clarifies Class A and Class B UV performance thresholds, which helps users fit UV into a broader treatment plan when water is clear and pre-filtered. Portable RO devices continue to advertise comprehensive reduction across viruses and regulated chemicals, while UV devices position as fast microbe inactivation if turbidity is low. Hybrid designs that combine physical filtration and carbon with UV or RO are gaining visibility, and some brands have extended purifier-level claims into gravity-fed countertop products, pairing microbiological performance with chemical reduction in one cartridge form factor. This technology blending indicates a move to one device that answers and reduces confusion for non-expert users.

Geography Analysis

North America led the portable water purifier market with 44.5% of 2025 volume, supported by a deep outdoor culture and heightened attention to service reliability. Federal reporting of 4,036 boil water advisories in 2021, most linked to infrastructure failures, reinforced household interest in point-of-use options for contingency planning. Buyers in the United States and Canada compare purifier labels and virus claims closely and tend to accept larger form factors when they deliver broader contaminant coverage. Preparedness-minded households in this region also favor countertop portability that can ride through outages. Retailers emphasize certifications and throughput to move buyers from entry filters to certified purifiers. These behaviors align with a portable water purifier market that rewards credible documentation and ease of setup.

Asia-Pacific is projected to grow at 11.1% CAGR to 2031 as urbanization, outdoor recreation, and disaster readiness converge in demand. Households and institutions in several markets look for portable options that combine microbiological protection with chemical reduction, and that operate without fixed plumbing. Government planning for resiliency is reinforcing interest in scalable, portable solutions that can deploy quickly in response to flooding and storms. As smartphone adoption remains high, app-linked reminders and simple indicators help reduce maintenance friction. The portable water purifier market is capturing this interest with a mix of gravity, UV, and RO devices tailored for apartment living and travel. Countries with strong hiking and camping participation also move toward lighter solutions for weekend and holiday trips.

Europe's growth in the portable water purifier market includes strong adoption in outdoor active countries and rising interest in devices that reduce micropollutants while preserving mineral taste. Nordic and BENELUX countries show consistent interest in premium gravity and UV purifiers that fit with low-impact travel habits. Southern markets lean on portable bottles and UV pens for international travel convenience, which aligns with compact packing and airline rules. Middle East & Africa remains early stage with pockets of demand in higher income markets and through institutional or humanitarian channels. South America shows solid uptake in outdoor hotspots and urban centers, with a preference for portable countertop RO in households that want broader coverage. Across all regions, certified performance and practical portability shape purchasing, which supports consistent gains for the portable water purifier market.

- Katadyn Group

- LifeStraw (Vestergaard)

- Sawyer Products, Inc.

- MSR

- Platypus

- GRAYL, Inc.

- Aquamira

- HydroBlu

- Survivor Filter

- Icon LifeSaver Systems

- Water-to-Go

- Epic Water Filters

- LARQ

- WAATR (CrazyCap)

- GoSun

- PureHydration (Aquapure Traveller)

- Waterdrop

- SteriPEN (Katadyn brand)

- RapidPure

- Platypus (QuickDraw/GravityWorks)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising adventure tourism and off-grid activities drive demand for portable water purifiers

- 4.2.2 Emergency preparedness and disaster response funding prioritizes portable treatment

- 4.2.3 Rising awareness of backcountry pathogens and boil-water advisories

- 4.2.4 PFAS regulation and chemical-contaminant concerns elevate demand for certified claims

- 4.2.5 Defense and humanitarian procurement pull innovation into virus-rated portable systems

- 4.2.6 D2C and marketplace logistics reduce friction in global availability

- 4.3 Market Restraints

- 4.3.1 Flow-rate/clogging tradeoffs and maintenance burden limit repeat use

- 4.3.2 Many filters do not remove viruses or PFAS, creating trust and performance gaps

- 4.3.3 Tightening testing/claim scrutiny escalates cost and time-to-market

- 4.3.4 UV and gadget-centric devices underperform in turbid water and cold conditions

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Extrusion Water Purifier

- 5.1.2 Pump Water Purifier

- 5.1.3 Suction Water Purifier

- 5.1.4 UV-Pen Purifier

- 5.1.5 Others (Filter Bottles, Gravity Bags, etc.)

- 5.2 By Technology

- 5.2.1 Gravity Purifier

- 5.2.2 UV Purifier

- 5.2.3 RO Purifier

- 5.2.4 Others (Electro-adsorption, Nano-filtration, etc.)

- 5.3 By End-User

- 5.3.1 Residential

- 5.3.2 Commercial (schools, military, hospitals, etc.)

- 5.4 By Distribution Channel (Value)

- 5.4.1 B2C/Retail

- 5.4.1.1 Multi-brand Stores (big box retailers, department stores, electronics chain, home improvement centers)

- 5.4.1.2 Exclusive Brand Outlets

- 5.4.1.3 Online

- 5.4.1.4 Other Distribution Channels

- 5.4.2 B2B/Directly from the Manufacturers

- 5.4.1 B2C/Retail

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 Canada

- 5.5.1.2 United States

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Peru

- 5.5.2.3 Chile

- 5.5.2.4 Argentina

- 5.5.2.5 Rest of South America

- 5.5.3 Asia-Pacific

- 5.5.3.1 India

- 5.5.3.2 China

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.5.3.7 Rest of APAC

- 5.5.4 Europe

- 5.5.4.1 United Kingdom

- 5.5.4.2 Germany

- 5.5.4.3 France

- 5.5.4.4 Spain

- 5.5.4.5 Italy

- 5.5.4.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.5.4.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.5.4.8 Rest of Europe

- 5.5.5 Middle East & Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East & Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Katadyn Group

- 6.4.2 LifeStraw (Vestergaard)

- 6.4.3 Sawyer Products, Inc.

- 6.4.4 MSR

- 6.4.5 Platypus

- 6.4.6 GRAYL, Inc.

- 6.4.7 Aquamira

- 6.4.8 HydroBlu

- 6.4.9 Survivor Filter

- 6.4.10 Icon LifeSaver Systems

- 6.4.11 Water-to-Go

- 6.4.12 Epic Water Filters

- 6.4.13 LARQ

- 6.4.14 WAATR (CrazyCap)

- 6.4.15 GoSun

- 6.4.16 PureHydration (Aquapure Traveller)

- 6.4.17 Waterdrop

- 6.4.18 SteriPEN (Katadyn brand)

- 6.4.19 RapidPure

- 6.4.20 Platypus (QuickDraw/GravityWorks)

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment

- 7.2 PFAS-compliant portable purifiers for travelers and emergency kits

- 7.3 Virus-rated group gravity/pump systems for humanitarian, defense, and field hospitals