PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062020

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062020

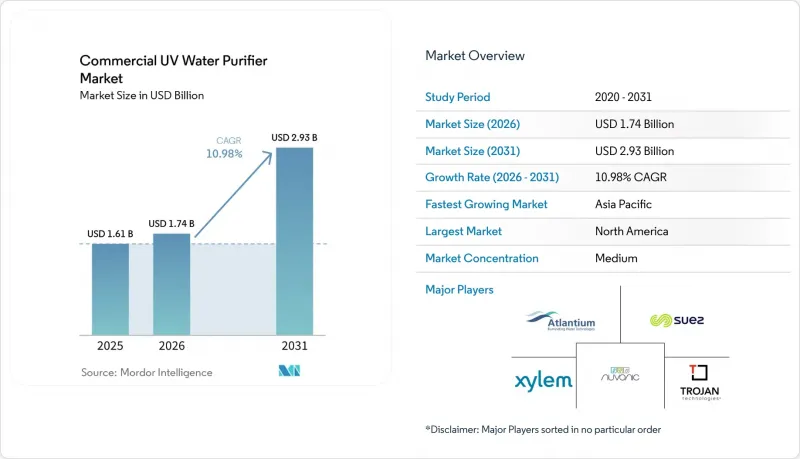

Commercial UV Water Purifier - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the commercial UV water purifier market size is expected to grow from USD 1.61 billion in 2025 to USD 1.74 billion in 2026 and is forecast to reach USD 2.93 billion by 2031 at 10.98% CAGR over 2026-2031.

This report is Segmented by Product Type (Low-Pressure and More), Application (Wastewater Treatment and More), Installation Type (Batch UV Systems and More), System Configuration (Single-Stage and More), End-User Industry (Residential Sector and More), Distribution Channel (Online and More), and Geography. Market Forecasts are Provided in Terms of Value USD.

Global Commercial UV Water Purifier Market Trends and Insights

California and Colorado DPR Rules Force Multi-Barrier UV Integration

California's 2025 direct potable reuse framework elevates UV disinfection from an optional polishing step to a required component in a multi-barrier train that includes membrane separation and advanced oxidation, with stringent log-reduction targets for viruses and protozoa . Colorado's potable reuse rule mirrors the multi-barrier concept, sets default log-reduction values, and requires at least one eligible disinfection barrier, such as UV or ozone, as a critical control point, reinforcing design convergence across state-level programs . Utilities are responding by procuring validated, controller-integrated UV units tied into SCADA with continuous UVT monitoring, automated lamp intensity control, and data-logged dose assurance to streamline compliance reporting. The North City Pure Water facility in San Diego illustrates the protocol, placing UV/AOP after ozonation, biologically activated carbon, and reverse osmosis to complete a five-step process that has passed tens of thousands of quality tests. This regulatory clarity supports the commercial UV water purifier market as procurement teams prioritize proven validation pathways, cybersecurity-ready controls, and factory-integrated performance monitoring to limit commissioning delays and verification costs.

Mercury Phase-Outs Accelerate UV-C LED Adoption Despite Cost Gaps

Global and regional policy shifts are tightening constraints on mercury-based lamps, with the Minamata Convention's upcoming controls, the European Union's lamp phase-out timeline, and Japan's fluorescent lamp ban pushing OEM portfolios toward solid-state UV-C LED systems. Miura's 2026 commercial launch of a 25 m3/h UV-LED sterilizer, built on high-output Nichia emitters with a compact footprint, shows how industrial POE and POU designs are scaling in cosmetics, pharma, and beverage lines. Nikkiso's PearlAqua platform spans from compact point-of-entry modules to municipal-scale units, positioning deep-UV LEDs under 280 nm for flexible deployment across water servers, factory wash lines, aquaculture tanks, and treatment plants. Materials advances also matter, with Crystal IS reporting 100 mm single-crystal AlN wafer readiness in 2024 to support serial production of germicidal LEDs at 260-270 nm, which underpins future emitter performance and reliability. These developments do not erase today's capital premium for LEDs, yet they reduce maintenance touchpoints, simplify end-of-life compliance, and curb mercury handling, which together strengthen the commercial UV water purifier market's long-run shift toward solid-state systems where policy and lifetime cost models align.

Turbidity Sensitivity and Lack of Residual Disinfection Constrain Standalone Deployment

UV dose delivery drops when turbidity exceeds regulatory thresholds because particulate and dissolved matter shield pathogens, which is why drinking water rules require low turbidity and high UV transmittance before UV application . Unlike chlorine, UV provides no residual in pipelines, so networks with biofilm risks still need an additional barrier at distribution ends or a downstream disinfectant to avoid recontamination. In tropical regions with seasonal surges in turbidity and humic content, utilities must pair UV with upstream coagulation and filtration, which raises lifecycle costs and adds maintenance tasks. Studies from large-scale plants have shown UV's effectiveness against protozoa after proper filtration, while affirming the need for a final residual within the distribution system to keep water safe to the tap. These constraints limit UV's standalone role in remote sites unless used with filtration, which fragments procurement across multiple vendors and complicates warranty administration for combined systems in the commercial UV water purifier market.

Other drivers and restraints analyzed in the detailed report include:

- IoT-Enabled UV Systems Unlock Performance-Based Contracting

- Aging Infrastructure and Municipal Retrofit Cycles Drive Replacement Demand

- Quartz Sleeve Supply Constraints and Controller Electronics Shortages Throttle Scaling

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Low-pressure UV systems held 44.4% of the commercial UV water purifier market share in 2025, supported by long lamp life and predictable O&M profiles across municipal and industrial lines. Momentum is shifting as UV-C LED units gain on policy changes that penalize mercury in OECD markets, which accelerates asset owners' shift toward solid-state designs in new lines and selective retrofits where lifetime costs and disposal risks carry weight. Medium-pressure UV remains relevant in high-flow conditions and lower-UVT wastewater trains, although its shorter lamp life increases service frequency compared to amalgam low-pressure designs . Hybrid UV-RO skids are expanding in decentralized packaged plants for hotels, bottled water sites, and greenhouses where footprint limits and commissioning speed favor integrated designs over field-built sequences. Emergency and mobile container solutions continue to gain traction, including UV-LED carts that allow rapid deployment and supervised operation in disaster response, which broadens access points for chemical-free disinfection.

UV-C LED systems are on track for a 14.7% CAGR through 2031 as major components mature and as early adopters in Japan, South Korea, and Scandinavia expand use cases from compact POE/POU to mid-scale industrial loops. Miura's 25 m3/h UV-LED release underscores how footprint and operational simplicity improve with high-output emitters, which lowers mechanical complexity and lamp handling risks. Nikkiso's portfolio positioning demonstrates how LED-based units can flex into municipal and industrial roles with scalable arrays and integrated monitoring for verified dose delivery. The enduring presence of low-pressure and medium-pressure lamps ensures a gradual transition as cost-sensitive buyers wait for further LED price declines, yet the direction of change is clear, where regulations and lifecycle cost models align. This dynamic will keep the commercial UV water purifier market competitive across technology lines while encouraging OEMs to maintain dual-track portfolios during the forecast window.

Drinking water purification held 53.8% in 2025 due to potable reuse mandates and municipal retrofits that codify UV inside multi-barrier designs for verified pathogen inactivation. Wastewater reuse projects continue to replace chemical contact basins with UV-based polishing to eliminate disinfection byproducts, supported by validated open-channel systems in major reuse centers. Industrial process water needs around ultra-low TOC and high log-reduction standards drive the use of high-performance UV reactors that fit into compact skids with multireactor manifolds. Food and beverage operators rely on UV to disinfect sugar syrups and condensate recoveries, avoiding thermal methods that can degrade product characteristics. Regional wastewater upgrades that pair UV with membranes to meet discharge and reuse standards illustrate the long-term role of UV in environmental protection.

Aquaculture water treatment is advancing at a 12.8% CAGR through 2031 as RAS farms scale in Asia, Europe, and the Americas and as export markets require mercury-free biosecurity measures. As LED options expand, hatcheries adopt compact, solid-state reactors that simplify maintenance and reduce lamp disposal liabilities while meeting dose targets for pathogen control at high stocking densities. System designers integrate UV into central loops and localized tanks to contain outbreaks and to protect expensive fry inventories, which lowers insurance risks and aligns with stricter audit trails. UV's chemical-free profile fits aquaculture, where residuals can stress stock and alter water chemistry, although influent conditioning remains necessary to secure a dose where solids and organics elevate. These factors keep aquaculture as one of the faster-growing application lines in the commercial UV water purifier market during the forecast period.

Geography Analysis

North America held 36.25% of revenue in 2025 and is projected to grow at a 6.5% CAGR through 2031 as utilities focus on replacements and compliance-driven upgrades rather than greenfield expansions. The North City Pure Water project in San Diego demonstrates how UV/AOP final barriers fit into advanced reuse, providing a model for other cities that are now planning or piloting DPR programs. Utilities in the region are adopting validated, sensor-rich reactors and open-channel UV for reuse, with suppliers emphasizing real-time dose assurance and automated controls to meet state-specific mandates. Differences among states on TOC and LRV targets create localized compliance documentation requirements that favor incumbents with specialized regulatory teams. A combination of replacement cycles and compliance upgrades will maintain a steady base for the commercial UV water purifier market in North America during the forecast period.

Asia-Pacific is projected to expand at a 13.8% CAGR through 2031, led by municipal wastewater upgrades, piped-water expansion programs, and aquaculture growth that demands chemical-free barriers. The Philippines installed a municipal UV disinfection system at the Calamba Water District in 2024 with a PHP 100 million budget, equal to USD 1.8 million using 2024 average exchange rates, which signals growing municipal adoption in Southeast Asia. Japan's industrial sector is deploying higher-capacity UV-LED systems as mercury lamps exit the market, which is expanding POE and POU use cases in process lines. LED providers now offer both compact and municipal-scale models, which helps diversify options for municipalities and industrial buyers across the region. These shifts position Asia-Pacific as the fastest-growing region for the commercial UV water purifier market.

Europe maintains a mature installed base with a measured 6% growth path that is supported by aggressive mercury phase-outs and by the expansion of "chlorine-free" UV disinfection in selected municipalities. France and neighboring countries illustrate how local OEMs deliver certified systems for drinking water while Scandinavia pilots municipal-scale LED deployments for potential nationwide rollouts. Southern Europe uses proven low-pressure systems at scale for wastewater polishing, demonstrating how different subregions follow distinct technology curves inside the same policy block. Western Asia and Africa outpace Europe's growth rates as new reuse and desalination projects add polishing steps and as donor programs expand rural systems, while South America grows unevenly with pockets of resort city retrofits. These regional patterns give suppliers an incentive to maintain portfolios that span mercury and LED, municipal and industrial, and packaged and component models to fit different adoption drivers in the commercial UV water purifier market.

- Xylem (Wedeco, ATG, Evoqua)

- Trojan Technologies (Veralto)

- Nuvonic (Halma: Aquionics, Berson, Hanovia, Orca)

- Atlantium Technologies

- SUEZ (Aquaray)

- ProMinent GmbH

- ULTRAAQUA A/S

- Atlantic Ultraviolet Corporation

- Heraeus Noblelight

- American Ultraviolet

- Advanced UV, Inc.

- ENAQUA

- Aquafine (Trojan Technologies)

- VIQUA (Trojan Technologies)

- ATG UV (Xylem)

- Severn Trent Services

- Kuraray (Calgon Carbon UV/AOP)

- Pentair (Commercial UV Solutions)

- Watts Water Technologies (Commercial UV)

- UV Pure Technologies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stricter potable, reuse, and industrial water quality rules

- 4.2.2 Shift to chemical-free, DBP-free disinfection

- 4.2.3 UV-C LED performance gains enabling compact POE/POU

- 4.2.4 Aging water assets and retrofit programs in utilities and industry

- 4.2.5 Validation-driven, IoT-dosed UV enabling performance contracts

- 4.2.6 Decarbonizing cooling/process loops by replacing biocides

- 4.3 Market Restraints

- 4.3.1 No residual; efficacy sensitive to UVT/turbidity

- 4.3.2 Quartz sleeve and controller electronics supply constraints

- 4.3.3 Skilled labor gaps for UV system design/validation

- 4.3.4 High capex and O&M for medium/large-flow systems

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Low-Pressure UV Systems

- 5.1.2 Medium-Pressure UV Systems

- 5.1.3 UV LED Systems

- 5.1.4 Hybrid UV-RO Units

- 5.1.5 Mobile/Containerised UV Units

- 5.2 By Application

- 5.2.1 Purification of Drinking Water

- 5.2.2 Wastewater Treatment

- 5.2.3 Industrial Process Water Treatment

- 5.2.4 Aquaculture Water Treatment

- 5.2.5 Food & Beverage Processing

- 5.3 By Installation Type

- 5.3.1 Batch UV Systems

- 5.3.2 Continuous Flow UV Systems

- 5.3.3 Skid-Mounted Systems

- 5.3.4 Modular Systems

- 5.4 By System Configuration

- 5.4.1 Single-Stage UV Systems

- 5.4.2 Multi-Stage UV Systems

- 5.4.3 Compact UV Systems

- 5.4.4 Custom Configurable Systems

- 5.5 By End-User Industry

- 5.5.1 Municipal Water Treatment

- 5.5.2 Residential Sector

- 5.5.3 Commercial Sector

- 5.5.4 Healthcare Facilities

- 5.5.5 Food Processing Industry

- 5.6 By Distribution Channel

- 5.6.1 Direct Sales

- 5.6.2 EPC and System Integrators

- 5.6.3 Authorized Distributors and Value Added Resellers

- 5.6.4 Online (B2B marketplaces and D2C)

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 Canada

- 5.7.1.2 United States

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Peru

- 5.7.2.3 Chile

- 5.7.2.4 Argentina

- 5.7.2.5 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 United Kingdom

- 5.7.3.2 Germany

- 5.7.3.3 France

- 5.7.3.4 Spain

- 5.7.3.5 Italy

- 5.7.3.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.7.3.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.7.3.8 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 India

- 5.7.4.2 China

- 5.7.4.3 Japan

- 5.7.4.4 Australia

- 5.7.4.5 South Korea

- 5.7.4.6 South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines)

- 5.7.4.7 Rest of Asia-Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 United Arab Emirates

- 5.7.5.2 Saudi Arabia

- 5.7.5.3 South Africa

- 5.7.5.4 Nigeria

- 5.7.5.5 Rest of Middle East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Xylem (Wedeco, ATG, Evoqua)

- 6.4.2 Trojan Technologies (Veralto)

- 6.4.3 Nuvonic (Halma: Aquionics, Berson, Hanovia, Orca)

- 6.4.4 Atlantium Technologies

- 6.4.5 SUEZ (Aquaray)

- 6.4.6 ProMinent GmbH

- 6.4.7 ULTRAAQUA A/S

- 6.4.8 Atlantic Ultraviolet Corporation

- 6.4.9 Heraeus Noblelight

- 6.4.10 American Ultraviolet

- 6.4.11 Advanced UV, Inc.

- 6.4.12 ENAQUA

- 6.4.13 Aquafine (Trojan Technologies)

- 6.4.14 VIQUA (Trojan Technologies)

- 6.4.15 ATG UV (Xylem)

- 6.4.16 Severn Trent Services

- 6.4.17 Kuraray (Calgon Carbon UV/AOP)

- 6.4.18 Pentair (Commercial UV Solutions)

- 6.4.19 Watts Water Technologies (Commercial UV)

- 6.4.20 UV Pure Technologies

7 Market Opportunities & Future Outlook

- 7.1 UV-C LED POE/POU retrofits for decentralized commercial buildings

- 7.2 UV-AOP for micropollutant control in beverage and pharma process water

- 7.3 Modular skid UV for emergency/disaster relief and remote sites