PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071369

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2071369

Aviation Fuel Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

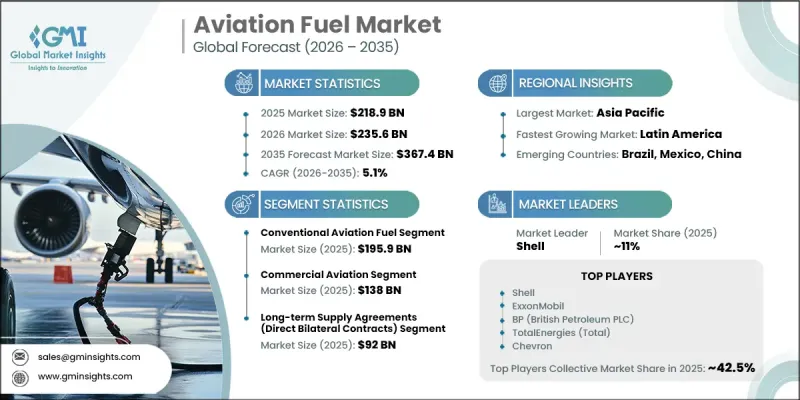

The Global Aviation Fuel Market was valued at USD 218.9 billion in 2025 and is estimated to grow at a CAGR of 5.1% to reach USD 367.4 billion by 2035.

The market is experiencing steady expansion owing to the continuous rise in global air passenger traffic across both domestic and international routes. Increasing tourism activity, growing business travel, and improved regional air connectivity are contributing to higher aircraft utilization worldwide. Rising disposable incomes and the expansion of the middle-class population in developing economies are further supporting passenger growth and strengthening demand for air transportation services. In addition, the recovery of long-distance travel and the increase in flight frequency are driving higher aviation fuel consumption across commercial airline operations. Growing preference for air transportation for long-distance travel continues to reinforce market growth. The Aviation Fuel Market is also benefiting from ongoing investments in airline fleet modernization and airport infrastructure development. Airlines are expanding and upgrading their aircraft fleets to accommodate rising passenger demand while improving operational efficiency. Simultaneously, governments and private-sector stakeholders are investing in airport expansion projects, fueling infrastructure, and regional connectivity initiatives to enhance aviation capacity. These developments continue to create favorable conditions for sustained growth across the global aviation sector.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $218.9 Billion |

| Forecast Value | $367.4 Billion |

| CAGR | 5.1% |

The conventional aviation fuel segment generated USD 195.9 billion in 2025. The segment continues to dominate the industry due to its extensive use across commercial, military, and cargo aviation operations. Consistent growth in passenger traffic, expanding airline networks, and increasing aircraft movements are supporting strong demand for traditional aviation fuels. Furthermore, established refining capabilities, mature supply chains, and compatibility with existing aircraft technologies continue to reinforce the widespread adoption of conventional aviation fuel across major aviation markets worldwide.

The commercial aviation segment captured USD 138 billion in 2025. The segment's strong position is driven by rising passenger volumes across domestic and international routes, continued expansion of airline networks, and increasing aircraft deployment globally. Growth in tourism, business travel, and budget airline operations continues to support fuel demand within the commercial aviation sector. Additionally, increasing air freight activity and ongoing airport infrastructure enhancements are contributing to higher fuel consumption levels, further strengthening the segment's market position.

North America Aviation Fuel Market generated USD 63.3 billion in 2025. The region benefits from increasing passenger traffic, a well-established commercial aviation industry, and continuous fleet expansion activities. The United States remains the largest contributor to regional revenue, supported by an extensive domestic aviation network, substantial defense aviation operations, and a highly developed refining infrastructure that supports aviation fuel production. Regional growth is also being supported by increasing cargo aviation activity and continued investments in airport modernization and aviation infrastructure development.

Major companies operating in the Global Aviation Fuel Market include Chevron, Shell, ExxonMobil, TotalEnergies, BP (British Petroleum PLC), World Kinect Corporation, Vitol, China Aviation Oil, Indian Oil Corporation Limited, Bharat Petroleum Corporation Limited (BPCL), Hindustan Petroleum Corporation Limited (HPCL), Gazprom, Mercury Air Group, and Virent, Inc. a Companies operating in the Aviation Fuel Market are adopting a variety of strategic initiatives to strengthen their market presence and enhance long-term competitiveness. Key strategies include expanding refining capacity, optimizing fuel supply networks, and strengthening distribution infrastructure to improve operational efficiency and meet growing demand. Market participants are also investing in sustainable aviation fuel development, advanced production technologies, and research initiatives aimed at reducing carbon emissions and supporting industry sustainability goals. Strategic partnerships, long-term supply agreements, and collaborations with airlines, airports, and fuel distributors are helping companies secure stable revenue streams and expand customer reach. Additionally, businesses are focusing on geographic expansion, digital supply chain management, and infrastructure modernization to improve service reliability, increase market penetration, and maintain a strong competitive position within the evolving aviation fuel industry.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Fuel Type

- 2.2.3 Application

- 2.2.4 Procurement Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global air passenger traffic

- 3.2.1.2 Expansion of airline fleets and airport infrastructure

- 3.2.1.3 Growth in air cargo and logistics transportation

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Volatility in crude oil prices

- 3.2.2.2 Stringent environmental regulations

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing adoption of sustainable aviation fuel (SAF)

- 3.2.3.2 Emerging aviation markets in developing economies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Fuel Type, 2022 - 2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Conventional Aviation Fuel

- 5.2.1 Jet Fuel (Turbine Fuel)

- 5.2.2 Aviation Gasoline (Avgas)

- 5.2.3 Others

- 5.3 Sustainable Aviation Fuel (SAF)

- 5.3.1 HEFA-SPK (Hydroprocessed Esters & Fatty Acids)

- 5.3.2 FT-SPK (Fischer-Tropsch Synthetic Paraffinic Kerosene)

- 5.3.3 ATJ-SPK (Alcohol-to-Jet Synthetic Paraffinic Kerosene)

- 5.3.4 Others (Co-processing, SIP, HC-HEFA)

- 5.4 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Commercial aviation

- 6.2.1 Narrow-body aircraft

- 6.2.2 Wide-body aircraft

- 6.2.3 Regional jets & turboprops

- 6.2.4 Air cargo & freighters

- 6.3 Military aviation

- 6.3.1 Fighter & combat aircraft

- 6.3.2 Transport & logistics aircraft

- 6.3.3 Military helicopters

- 6.3.4 Military UAVs & unmanned combat aerial vehicles (UCAVs)

- 6.4 Private & business aviation

- 6.4.1 Business jets

- 6.4.2 Turboprop & piston-engine private aircraft

- 6.5 Commercial & civil UAVs/drones

- 6.5.1 Logistics & last-mile delivery drones

- 6.5.2 Surveillance, mapping & inspection UAVs

- 6.5.3 Agricultural UAVs

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Procurement Channel, 2022 - 2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Long-Term Supply Agreements (Direct Bilateral Contracts)

- 7.3 Spot Market Purchases

- 7.4 Into-Plane Service Contracts (via FBOs & Handling Agents)

- 7.5 Government & Tender-Based Procurement

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 ExxonMobil

- 9.2 Shell

- 9.3 BP (British Petroleum PLC)

- 9.4 TotalEnergies (Total)

- 9.5 Chevron

- 9.6 Vitol

- 9.7 World Kinect Corporation

- 9.8 China Aviation Oil

- 9.9 Indian Oil Corporation Limited

- 9.10 Bharat Petroleum Corporation Limited (BPCL)

- 9.11 Hindustan Petroleum Corporation Limited (HPCL)

- 9.12 Gazprom

- 9.13 Mercury Air Group

- 9.14 Virent, Inc.