PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073559

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073559

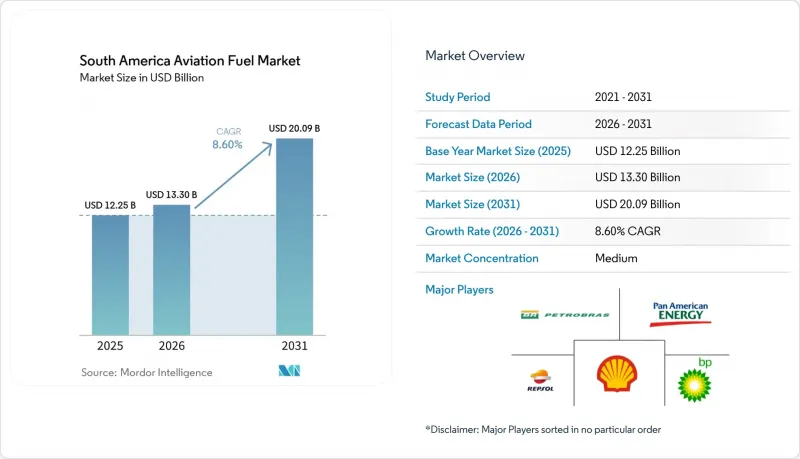

South America Aviation Fuel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2031)

According to Mordor Intelligence, the south america aviation fuel market size was valued at USD 12.25 billion in 2025 and is estimated to grow from USD 13.30 billion in 2026 to reach USD 20.09 billion by 2031, at a CAGR of 8.60% during the forecast period (2026-2031).

This report is Segmented by Fuel Type (Conventional Jet Fuel, SAF, Avgas), Aircraft Type (Narrow-Body, Wide-Body, Regional Jets and Turboprops, Cargo/Freighters), Application (Commercial Airlines, Defense/Military, General Aviation, Urban Air Mobility/EVTOL), and Geography (Brazil, Argentina, Colombia, Chile, Peru, Rest of South America). Market Forecasts are Provided in Value (USD).

South America Aviation Fuel Market Trends and Insights

Recovering Air Passenger Traffic Fuels Jet-A1 Demand

South America's airline sector has moved beyond a simple rebound and into a broader expansion phase that is now giving the South America aviation fuel market a firmer demand base. Latin America and Caribbean airlines recorded 8.6% year-on-year RPK growth in Q1 2026, and Brazil's domestic market grew 11.4% in the same period, which shows that traffic growth is still running ahead of many earlier expectations. Load factors have also stayed high, with the regional market reaching 85.9% in November 2025, which points to tight capacity and stronger aircraft utilization rather than a short-lived spike in bookings. When airlines keep aircraft in the air longer and fill more seats, fuel demand rises in a direct and predictable way across trunk routes, connecting routes, and airport turnarounds. This is why the South America aviation fuel market is benefiting not only from more passengers, but also from a more intensive use of available fleets and airport slots.

Expanding Low-Cost Carriers and Route Liberalization Widen the Fuel Market

Low-cost carrier growth is widening the South America aviation fuel market by pushing service beyond the main capital-city corridors and into secondary airports that need regular fuel supply. Argentina's liberalization push helped lift seat capacity by 8.5% in Q1 2026, which shows how policy change can quickly translate into more aircraft activity and more frequent departures. This matters because each new route does more than add passengers; it creates a repeat fuel-demand point that needs storage, delivery coordination, and supplier reliability. The effect is especially visible in domestic and short-haul flying, where single-aisle fleets run high daily utilization and turn fuel into one of the most immediate operating variables. As liberalization spreads, the South America aviation fuel market should see demand broaden geographically rather than remain tied only to the largest hubs.

Limited Regional SAF Production Capacity Creates Near-Term Supply Risk

The South America aviation fuel market is moving into mandated SAF consumption before the region has built a wide enough production base to supply it comfortably. Petrobras has established the first domestic delivery benchmark in Brazil, but the regional supply chain is still early and remains concentrated in a small number of projects and planned capacity additions. This creates a narrow supply window in which early compliance can depend on a small producer set, limited co-processing volumes, and gradual refinery adaptation rather than deep market liquidity. The MIT, LATAM, and Airbus work on Latin American decarbonization also points to the value of book-and-claim structures, because smaller national markets will struggle if they must wait for full local physical supply before participating in SAF procurement. Until production spreads beyond a few anchor projects, the South America aviation fuel market will face a supply-side constraint that can slow adoption even where regulation is already clear.

Other drivers and restraints analyzed in the detailed report include:

- Green-Corridor Commitments Accelerating SAF Uptake

- Airport Infrastructure Modernization Programs Drive Long-Term Fuel Infrastructure Demand

- Currency Volatility Increasing Fuel-Price Risk for Operators

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Conventional jet fuel accounted for 92.3% of South America aviation fuel market size in 2025, which shows that the region still runs on a deeply established fossil-fuel base. This dominance is tied to the installed reality of the market, because airport fuel systems, distribution assets, and most refinery output are already aligned with Jet A-1 and related aviation kerosene specifications. The segment should therefore remain the main source of supply over the near term, even as regulation starts to reshape procurement behavior around lower-carbon alternatives. Avgas remains a small but durable niche because general aviation, agricultural flying, and interior connectivity still depend on aircraft types that do not move with the same fuel profile as the main airline fleet.

SAF is the fastest-growing fuel type, with South America aviation fuel market size for this segment projected to expand at a 28.6% CAGR from 2026 to 2031. The growth rate looks high because the starting base is still small, but the underlying shift is real as Brazil's policy framework and CORSIA compliance pressures begin to turn SAF into a planning requirement rather than a symbolic purchase. Petrobras strengthened that path with its first domestic SAF delivery in December 2025, proving that certified local supply can move from refinery output into airport distribution. The Boaventura project and Raizen's certification pathway also show that the South America aviation fuel industry is building around feedstock access, co-processing, and ethanol-based routes rather than waiting for a single technology outcome.

Complete Report Scope:

- By Fuel Type

- Conventional Jet Fuel

- Sustainable Aviation Fuel (SAF)

- Avgas

- By Aircraft Type

- Narrow-body

- Wide-body

- Regional Jets and Turboprops

- Cargo/Freighters

- By Application

- Commercial Airlines

- Defense/Military Aviation

- General and Business Aviation

- Urban Air Mobility / eVTOL

- By Geography

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

List of Companies Covered in this Report:

- Petroleo Brasileiro SA (Petrobras)

- Repsol SA

- BP PLC

- Shell PLC

- TotalEnergies SE

- Pan American Energy SL

- Exxon Mobil Corporation

- Allied Aviation Services Inc.

- Ipiranga Produtos de Petroleo SA

- Raizen Energia SA

- YPF SA

- ENAP Refinerias SA

- Petroperu SA

- Chevron Corporation

- Vitol Aviation BV

- Gevo Inc.

- World Energy LLC

- Amyris Inc.

- SkyNRG BV

- Neste Oyj

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Recovering air passenger traffic post-pandemic

- 4.2.2 Expanding low-cost carriers and route liberalization

- 4.2.3 Rising disposable income & middle-class growth

- 4.2.4 Airport infrastructure modernization programs

- 4.2.5 eVTOL & regional air-taxi projects boost Jet-A1 demand

- 4.2.6 Green-corridor commitments accelerating SAF uptake

- 4.3 Market Restraints

- 4.3.1 Limited regional SAF production capacity

- 4.3.2 Currency volatility increasing fuel-price risk

- 4.3.3 Fossil-fuel dominated energy mix & policy inertia

- 4.3.4 Fuel-pipeline bottlenecks to remote airports

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Fuel Type

- 5.1.1 Conventional Jet Fuel

- 5.1.2 Sustainable Aviation Fuel (SAF)

- 5.1.3 Avgas

- 5.2 By Aircraft Type

- 5.2.1 Narrow-body

- 5.2.2 Wide-body

- 5.2.3 Regional Jets and Turboprops

- 5.2.4 Cargo/Freighters

- 5.3 By Application

- 5.3.1 Commercial Airlines

- 5.3.2 Defense/Military Aviation

- 5.3.3 General and Business Aviation

- 5.3.4 Urban Air Mobility / eVTOL

- 5.4 By Geography

- 5.4.1 Brazil

- 5.4.2 Argentina

- 5.4.3 Colombia

- 5.4.4 Chile

- 5.4.5 Peru

- 5.4.6 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Petroleo Brasileiro SA (Petrobras)

- 6.4.2 Repsol SA

- 6.4.3 BP PLC

- 6.4.4 Shell PLC

- 6.4.5 TotalEnergies SE

- 6.4.6 Pan American Energy SL

- 6.4.7 Exxon Mobil Corporation

- 6.4.8 Allied Aviation Services Inc.

- 6.4.9 Ipiranga Produtos de Petroleo SA

- 6.4.10 Raizen Energia SA

- 6.4.11 YPF SA

- 6.4.12 ENAP Refinerias SA

- 6.4.13 Petroperu SA

- 6.4.14 Chevron Corporation

- 6.4.15 Vitol Aviation BV

- 6.4.16 Gevo Inc.

- 6.4.17 World Energy LLC

- 6.4.18 Amyris Inc.

- 6.4.19 SkyNRG BV

- 6.4.20 Neste Oyj

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment