PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2083312

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2083312

Commercial Heating Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

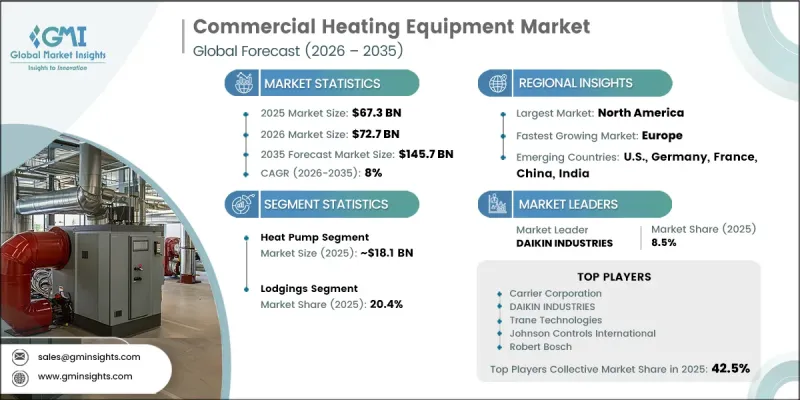

The Global Commercial Heating Equipment Market was valued at USD 67.3 billion in 2025 and is estimated to grow at a CAGR of 8% to reach USD 145.7 billion by 2035.

The market is experiencing strong momentum, supported by continuous investments in energy-efficient commercial infrastructure, replacement of aging heating systems, and growing construction activity across major global economies. Increasing emphasis on reducing carbon emissions, improving building energy efficiency, and complying with evolving environmental regulations is accelerating the transition toward electrically powered commercial heating technologies. Building owners and facility managers are increasingly replacing conventional heating equipment with advanced systems that deliver higher operational efficiency and lower long-term energy costs. Government initiatives promoting energy-efficient infrastructure, combined with favorable financial incentives and modernization programs, continue to encourage large-scale equipment upgrades across commercial buildings. Rising operational expenses associated with traditional heating technologies are also driving demand for modern alternatives that offer improved performance and lower lifecycle costs. These long-term industry trends are expected to support sustained growth across the global commercial heating equipment market throughout the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $67.3 Billion |

| Forecast Value | $145.7 Billion |

| CAGR | 8% |

The commercial heating equipment market continues to benefit from increasing investments in sustainable building technologies and modernization projects. Businesses are placing greater emphasis on reducing energy consumption while improving environmental performance and operational reliability. Growing adoption of intelligent building management systems and energy-efficient heating solutions is strengthening demand across commercial facilities. Continuous improvements in product performance, combined with stricter building efficiency standards and ongoing replacement of outdated heating infrastructure, are creating favorable conditions for long-term market expansion.

The heat pump segment accounted for 26.9% share in 2025, generating USD 18.1 billion, and is projected to grow at a CAGR of 12% through 2035. This growth rate significantly exceeds the overall market average due to increasing demand across both new commercial construction and building renovation projects. Growing preference for energy-efficient heating technologies, favorable regulatory policies supporting low-emission systems, and continuous improvements in manufacturing efficiency are accelerating adoption. Declining installation cost differences between heat pump systems and conventional heating equipment are also supporting broader commercial acceptance.

The lodging segment held 20.4% share in 2025, equivalent to USD 13.7 billion, and is expected to grow at a CAGR of 8% through 2035. The segment maintains its leadership due to the continuous heating requirements of hospitality facilities and increasing investments in energy-efficient building operations. Commercial property owners are prioritizing heating system upgrades to improve operational efficiency, reduce energy costs, and support sustainability objectives, contributing to continued demand across this end-use sector.

North America Commercial Heating Equipment Market accounted for 28.2% share in 2025, representing USD 19 billion, and is forecast to grow at a CAGR of 5.9% through 2035. The regional market is characterized by a mature installed equipment base, with growth primarily supported by replacement demand rather than new construction. Ongoing modernization of commercial buildings, increasing focus on energy efficiency, and continued investment in advanced heating technologies are expected to sustain market expansion across the region throughout the forecast period.

Major players operating in the global commercial heating equipment market are Carrier Corporation, Daikin Industries, Mitsubishi Electric Corporation, Panasonic Corporation, Trane Technologies, Johnson Controls International, Lennox International, LG Electronics, Viessmann Group, Rheem Manufacturing Company, Robert Bosch, Vaillant Group, Danfoss, Honeywell International Inc., Ariston Holding N.V., BDR Thermea Group, A.O. Smith, STIEBEL ELTRON GmbH, Fujitsu General, Midea, Navien, Rinnai Corporation, Cleaver-Brooks, Goodman Manufacturing Company, Hoval, Thermax Limited, Miura America, Baxi Heating, Bradford White Corporation, Emerson Electric Co., Ferroli, Fulton, NIBE Industrier AB, SAMSUNG, WM Technologies, and WOLF GmbH. Companies operating in the commercial heating equipment market are strengthening their market position through continuous product innovation, expansion of energy-efficient product portfolios, and strategic investments in advanced heating technologies. Manufacturers are prioritizing research and development to improve system efficiency, smart connectivity, and sustainability while meeting evolving regulatory requirements. Businesses are also expanding production capabilities, strengthening distribution networks, and forming strategic partnerships to improve market reach and customer support. Digital monitoring solutions, intelligent building integration, and customized heating systems are becoming important competitive differentiators.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Technology trends

- 2.1.3 End use trends

- 2.1.4 Channel trends

- 2.1.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.3 Regulatory landscape

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of commercial heating equipment

- 3.7.1 Heat pump

- 3.7.2 Boiler

- 3.7.3 Furnace

- 3.7.4 Water heater

- 3.8 Emerging opportunities & trends

- 3.9 Digitalization & IoT integration

- 3.10 Growth in untapped markets & applications

- 3.11 Investment analysis & future prospects

- 3.12 Price trend analysis (USD/Unit) (Driven by Primary Research)

- 3.12.1 By region (Driven by Primary Research)

- 3.12.2 By technology (Driven by Primary Research)

- 3.13 Trade data analysis (Driven by Primary Research)

- 3.13.1 Import/export value trends (Driven by Primary Research)

- 3.13.2 Key trade corridors & tariff impact (Driven by Primary Research)

- 3.14 Impact of AI & Generative AI on the market (Driven by Primary Research)

- 3.14.1 AI-Driven production optimization (Driven by Primary Research)

- 3.14.2 Predictive maintenance & fault detection (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans & funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Size and Forecast, By Technology, 2022 - 2035 (USD Million & '000 Units)

- 5.1 Key trends

- 5.2 Heat pump

- 5.3 Boiler

- 5.4 Furnace

- 5.5 Water heater

- 5.6 Others

Chapter 6 Market Size and Forecast, By End Use, 2022 - 2035 (USD Million & '000 Units)

- 6.1 Key trends

- 6.2 Offices

- 6.3 Healthcare facilities

- 6.4 Educational institutions

- 6.5 Lodgings

- 6.6 Retail stores

- 6.7 Others

Chapter 7 Market Size and Forecast, By Channel, 2022 - 2035 (USD Million & '000 Units)

- 7.1 Key trends

- 7.2 Online

- 7.3 Dealer

- 7.4 Retail

Chapter 8 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & '000 Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 France

- 8.3.3 UK

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Portugal

- 8.3.7 Romania

- 8.3.8 Netherlands

- 8.3.9 Switzerland

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Egypt

- 8.5.4 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 A.O. Smith

- 9.2 Ariston Holding N.V.

- 9.3 Baxi Heating

- 9.4 BDR Thermea Group

- 9.5 Bradford White Corporation

- 9.6 Carrier Corporation

- 9.7 Cleaver-Brooks

- 9.8 DAIKIN INDUSTRIES

- 9.9 Danfoss

- 9.10 Emerson Electric Co.

- 9.11 Ferroli

- 9.12 Fujitsu General

- 9.13 Fulton

- 9.14 Goodman Manufacturing Company

- 9.15 Honeywell International Inc.

- 9.16 Hoval

- 9.17 Johnson Controls International

- 9.18 Lennox International

- 9.19 LG Electronics

- 9.20 Midea

- 9.21 Mitsubishi Electric Corporation

- 9.22 Miura America

- 9.23 Navien

- 9.24 NIBE Industrier AB

- 9.25 Panasonic Corporation

- 9.26 Rheem Manufacturing Company

- 9.27 Rinnai Corporation

- 9.28 Robert Bosch

- 9.29 SAMSUNG

- 9.30 STIEBEL ELTRON GmbH

- 9.31 Thermax Limited

- 9.32 Trane Technologies

- 9.33 Vaillant Group

- 9.34 Viessmann Group

- 9.35 WM Technologies

- 9.36 WOLF GmbH