PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073583

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073583

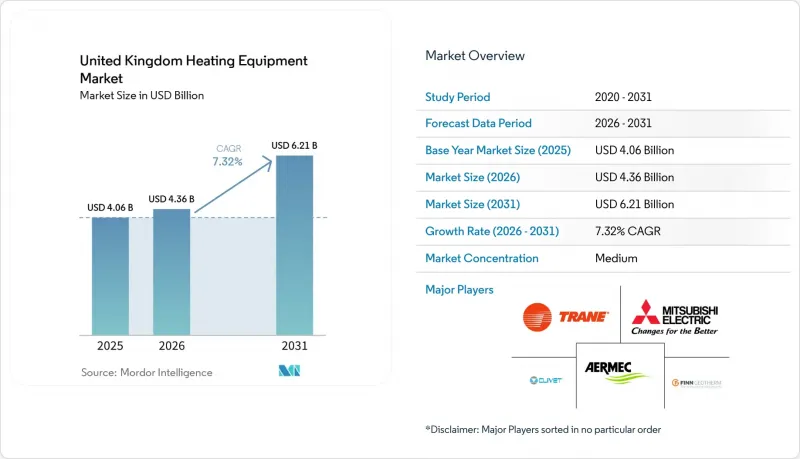

United Kingdom Heating Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united kingdom heating equipment market size is expected to grow from USD 4.06 billion in 2025 to USD 4.36 billion in 2026 and is forecast to reach USD 6.21 billion by 2031 at 7.32% CAGR over 2026-2031.

This report is Segmented by Equipment Type (Boilers, Furnaces, Heat Pumps, and More), End-User Industry (Residential, Commercial, and More), Fuel Type (Natural Gas, Electricity, Oil, and More), Technology (Condensing, Non-Condensing, and More), Installation Type (New Installation, and Replacement/Retrofit), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

United Kingdom Heating Equipment Market Trends and Insights

Supportive Government Decarbonisation Policies and Incentives

Expanded grants, technology-neutral eligibility, and flexible leasing options are reshaping purchasing behavior across the United Kingdom heating equipment market. The Department for Energy Security and Net Zero's consultation to widen the Boiler Upgrade Scheme now covers air-to-air units and heat batteries, aligning financial support with diverse property profiles. Coupled with a pledge to train 18,000 additional retrofit installers, the policy mix addresses both demand creation and supply-side capacity. March 2025 applications surged 88% year on year, signaling effective stimulus. Scotland's earlier 2045 Net Zero deadline amplifies local uptake, positioning policy as the single most powerful demand accelerator.

Ageing Boiler Stock Triggering Replacement Demand

More than 80% of U.K. homes were built before 1960, and many gas boilers installed during the 1990s now near end-of-life . This aging stock secures a baseline of predictable replacement volumes, driving 71.21% of current sales. Manufacturers exploit the cycle by offering hybrid packages that couple familiar gas units with add-on heat pumps compatible with existing pipework. As building codes tighten, each end-of-life event becomes an inflection point where owners weigh carbon and efficiency gains, sustaining both volume stability and technology upgrading within the United Kingdom heating equipment market.

High Upfront Cost of Low-Carbon Heating Systems

University of Edinburgh research found that average installed heat-pump prices have stagnated for a decade, leaving households with net costs of USD 6,500-14,000 even after grants. Properties needing electrical upgrades or radiator swaps see higher totals, deterring many until outright boiler failure. The economic barrier explains why replacement outpaces proactive retrofits despite policy support, curbing near-term acceleration of the United Kingdom heating equipment market.

Other drivers and restraints analyzed in the detailed report include:

- Efficiency-Boosting Technology Innovations

- Green-Home Finance Products Accelerating Upgrades

- Skilled Labour Shortage for Advanced Installations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Heat pumps are expanding at an 11.24% CAGR, steadily eroding the 37.65% share currently held by gas boilers. The United Kingdom heating equipment market size for heat pumps is set to widen as government rebates and high-temperature models enable retrofits without full radiator replacement. strengthening growth in the United Kingdom heat pumps market. Gas boilers persist due to lower capital outlay and installer familiarity, but forthcoming efficiency mandates tighten margins. Hybrid offerings combine both technologies, granting manufacturers a hedging strategy that balances present sales with future readiness. Furnaces and ancillary radiators maintain niche roles in industrial and large-commercial settings, providing steady though limited demand.

Gas-fired incumbents seek relevance through hydrogen-ready prototypes, exemplified by Worcester Bosch units certified for 20% hydrogen blends. Meanwhile, heat-pump specialists leverage private-equity backing to scale domestic capacity, signaling confidence in the long-term electrification trajectory of the United Kingdom heating equipment market.

The residential sector owned 58.41% revenue share in 2025 and is projected to expand at a 7.52% CAGR to 2031, reflecting both the sheer number of households and an aging installed base. Energy-efficiency rules for new builds are pushing developers toward low-carbon options from day one, while homeowners take advantage of grants when they replace legacy boilers. In commercial real estate, ESG commitments spur retrofits in offices, retail outlets, and hospitality venues, although project complexity can elongate decision cycles, moderating immediate growth rates across the United Kingdom heating equipment market.

Residential demand has become a proving ground for technology innovation. Heat Geek's portfolio of optimized residential heat-pump systems reportedly achieves 50% better seasonal performance than typical U.K. installations. The public-sector subsegment-schools, hospitals, and council buildings-leans on framework agreements to procure low-carbon equipment at scale and share maintenance expertise. Industrial users prioritize furnace technologies that can integrate with process heat requirements, whereas data centers increasingly evaluate liquid-cooling heat recovery, hinting at future adjacency opportunities within the United Kingdom heating equipment market.

Complete Report Scope:

- By Equipment Type

- Boilers

- Furnaces

- Heat Pumps

- Radiators and Other Heater Types

- By End-User Industry

- Residential

- Commercial

- Industrial

- Public/Institutional

- By Fuel Type

- Natural Gas

- Electricity

- Oil

- Biomass

- Hydrogen-Ready

- By Technology

- Condensing

- Non-Condensing

- Air Source Heat Pumps

- Ground Source Heat Pumps

- Hybrid Systems

- Smart Connected Systems

- By Installation Type

- New Installation

- Replacement/Retrofit

List of Companies Covered in this Report:

- Robert Bosch GmbH (Worcester Bosch Group)

- Vaillant GmbH

- Ideal Boilers Ltd.

- Baxi Heating UK Ltd.

- Viessmann Werke GmbH and Co. KG

- Mitsubishi Electric Europe B.V.

- Daikin Industries Ltd.

- Trane Technologies plc

- Danfoss A/S

- Aermec S.p.A.

- Clivet S.p.A.

- Finn Geotherm UK Ltd.

- Systemair AB

- Swegon Group AB

- Rhoss S.p.A.

- Grant Engineering (UK) Ltd.

- Kensa Heat Pumps Ltd.

- LG Electronics UK Ltd.

- Panasonic Heating and Cooling Solutions

- Stiebel Eltron GmbH and Co. KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Supportive government decarbonisation policies and incentives

- 4.2.2 Ageing boiler stock triggering replacement demand

- 4.2.3 Efficiency-boosting technology innovations

- 4.2.4 Green-home finance products accelerating upgrades

- 4.2.5 Urban district-heat network expansion

- 4.2.6 Emergence of heat-as-a-service subscription models

- 4.3 Market Restraints

- 4.3.1 High upfront cost of low-carbon heating systems

- 4.3.2 Skilled labour shortage for advanced installations

- 4.3.3 Rural grid-capacity constraints

- 4.3.4 Hydrogen-infrastructure uncertainty

- 4.4 Industry Ecosystem Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Equipment Type

- 5.1.1 Boilers

- 5.1.2 Furnaces

- 5.1.3 Heat Pumps

- 5.1.4 Radiators and Other Heater Types

- 5.2 By End-User Industry

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Industrial

- 5.2.4 Public/Institutional

- 5.3 By Fuel Type

- 5.3.1 Natural Gas

- 5.3.2 Electricity

- 5.3.3 Oil

- 5.3.4 Biomass

- 5.3.5 Hydrogen-Ready

- 5.4 By Technology

- 5.4.1 Condensing

- 5.4.2 Non-Condensing

- 5.4.3 Air Source Heat Pumps

- 5.4.4 Ground Source Heat Pumps

- 5.4.5 Hybrid Systems

- 5.4.6 Smart Connected Systems

- 5.5 By Installation Type

- 5.5.1 New Installation

- 5.5.2 Replacement/Retrofit

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Robert Bosch GmbH (Worcester Bosch Group)

- 6.4.2 Vaillant GmbH

- 6.4.3 Ideal Boilers Ltd.

- 6.4.4 Baxi Heating UK Ltd.

- 6.4.5 Viessmann Werke GmbH and Co. KG

- 6.4.6 Mitsubishi Electric Europe B.V.

- 6.4.7 Daikin Industries Ltd.

- 6.4.8 Trane Technologies plc

- 6.4.9 Danfoss A/S

- 6.4.10 Aermec S.p.A.

- 6.4.11 Clivet S.p.A.

- 6.4.12 Finn Geotherm UK Ltd.

- 6.4.13 Systemair AB

- 6.4.14 Swegon Group AB

- 6.4.15 Rhoss S.p.A.

- 6.4.16 Grant Engineering (UK) Ltd.

- 6.4.17 Kensa Heat Pumps Ltd.

- 6.4.18 LG Electronics UK Ltd.

- 6.4.19 Panasonic Heating and Cooling Solutions

- 6.4.20 Stiebel Eltron GmbH and Co. KG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment