PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644649

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644649

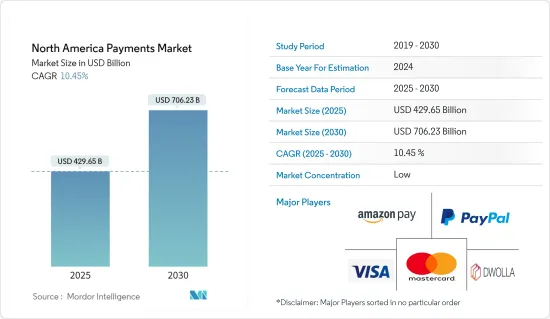

North America Payments - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The North America Payments Market size is estimated at USD 429.65 billion in 2025, and is expected to reach USD 706.23 billion by 2030, at a CAGR of 10.45% during the forecast period (2025-2030).

In the United States, American Express is a significant credit card corporation. It is well-known for offering exceptional customer service as well as some of the greatest incentives. From ultra-elite corporate travel cards to daily rewards, American Express has a credit card to fit every cardholder. Credit card issuers (or providing banks) are the institutions (banks or credit unions) from whom credit cards are obtained. The largest banks in the United States are Chase and Citi, while the largest in Canada are TD and RBC. The issuing bank has the authority to set the interest rate, the limit, international fees, and so on.

Key Highlights

- Using biometric authentication technologies in transactions is a major trend that is gaining traction in the payments industry. Biometric authentication is an essential payment technique that combines and provides accuracy, effectiveness, and security in a single package. For instance, in December 2023, FortressPay announced the launch of an enterprise-ready biometric payment platform. With its new Payment Identity platform, FortressPay aims to provide a frictionless customer experience while eliminating payment fraud.

- The payments industry is significantly shifting in both the consumer and business sectors. The rise of real-time payments, more access to and use of customer data, increasing consumer choice among digital and conventional payment methods, and growing rivalry and collaboration between internet behemoths and traditional banks are all hot subjects. These new and ongoing trends are requiring firms to reassess their business strategies in order to foster innovation and client acceptability.

- Technical advancements in the North American digital payment sector are projected to generate attractive development prospects for the market. This platform allows you to divide payments for online purchases using a combination of debit and credit cards with no interest or additional fees. As a result, the platform is expected to assist users in reducing the cost load on individual cards, increasing financial privacy, and building credit ratings.

- The COVID-19 pandemic significantly impacted the payment industry in North America. Lockdowns and business closures prevented people from making in-person purchases and altered how they transacted before the outbreak. While overall spending fell due to concerns about the economy and personal finances, people spent more money online, hastening the transition from cash to digital payments. There appears to have been a significant increase in contactless payment solutions, such as cards, smartphones, and wearable devices.

North America Payments Market Trends

Increasing use of digital wallets payments

- The increasing use of digital wallet payments in North America reflects a significant shift in consumer behavior and the broader digital transformation of financial services. As technology continues shaping how people manage their finances, digital wallets have emerged as a convenient, secure, and versatile alternative to traditional payment methods.

- Also, the regulatory environment in North America has adapted to accommodate the rise of digital wallets, ensuring that these payment methods align with existing financial regulations. As governments recognize the importance of fostering innovation in financial services, regulatory frameworks have evolved to provide a supportive environment for the growth of digital payment technologies.

- Furthermore, the e-commerce platforms can accept various payment methods, making it easier for more users to access the business, such as major credit cards, gift cards, etc. E-commerce platforms such as Amazon, eBay, and Shopify frequently charge monthly and transaction fees to cover online payment processing fees.

- E-commerce sales in the United States are increasing as digital payment experiences improve. This rise reflects consumers' growing comfort with online shopping and their increased use of mobile and handheld devices.

- The buy-now-pay-later (BNPL) service is gaining popularity among North American consumers as an alternative payment solution. Consumers in the United States utilize BNPL for a variety of reasons, including purchasing items that would otherwise be beyond reach, avoiding interest on credit cards, and borrowing money without a credit check. Market participants are implementing various tactics to expand the adoption of BNPL. For example, in May 2023, Splitit announced its partnership with visa to offer merchants a buy now, pay later (BNPL) solution. Both the companies had signed an agreement in which Splitit's installments-as-a-service offering is combined with Visa Instalments to form a BNPL solution that will be piloted in select markets during the second half of the year

United States to hold a majority market share

- Credit cards are the most commonly used payment method in the United States and Canada, both offline and online, with debit cards coming in second. With the enhancement of digital payment experiences, the country's e-commerce sales are expanding. This growth reflects customers' growing comfort with online buying and their increased usage of mobile and handheld devices.

- Additionally, the Federal Reserve has integrated the United States' ACH system into local settling systems in Canada, the United Kingdom, the Eurozone, Mexico, and Panama, allowing individuals and companies to move cash directly from U.S. bank accounts to bank accounts in other countries. Financial technology firms are rapidly venturing into cross-border payments, notably peer-to-peer payments. Financial technology firms, for example, are joining the remittance sector, allowing users to fund "mobile wallets" online using their bank accounts and debit or credit cards and sending money straight to overseas mobile wallets.

- Moreover, retail instant payment systems execute small-value interbank transfers such that money is available almost quickly, as contrast to the possibly multiday settlement wait for retail transfers on some traditional bank payment systems. Like other retail payment systems, immediate payment systems often employ bank deposit money but eventually settle in central bank reserve balances. include the Clearing House's RTP Network (RTP), which began in 2017, and the FedNow Service, which the Federal Reserve aims to implement in 2023.

- Due to the growth of the digital payment market, mobile commerce has also changed the way brick-and-mortar businesses operate, particularly in terms of accepting cashless payments. Apple Pay, Samsung Pay, and Google Pay, for example, are among the leading competitors competing with market leaders in their respective countries. With consistent increases in mobile payment in several countries, the North American digital payment market is expanding rapidly.

North America Payments Industry Overview

The North American Payments market is highly competitive, with key players such as Apple Pay, Samsung Pay, Amazon Pay, Google Pay, and many others in the region developing new e-commerce solutions for a wide range of end-user applications. Companies are also investing and forming partnerships in the continent to expand their businesses and provide e-commerce platforms to the country's people.

- June 2023 - Amazon Pay announced its partnership with BNPL outlet Affirm. With this partnership, Amazon Pay offers buy-now-pay-later (BNPL) services to small business owners using its online store.

- March 2023 - Apple Inc. introduced Apple Pay Later in the U.S. designed with users' financial health, It also allows users to split purchases into four payments, spread over six weeks with no interest and no fees. Users can easily track, manage, and repay their Apple Pay later loans in one convenient location in Apple Wallet.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Stakeholder Analysis

- 4.3 Industry Attractiveness-Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Evolution of the payments landscape in North America

- 4.5 Key market trends pertaining to the growth of cashless transaction in North America

- 4.6 Impact of COVID-19 on the payments market in North America

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 High Proliferation of E-commerce, Including the Rise of M-commerce

- 5.1.2 Smartphone Growth and Electronic Initiatives in the payment market

- 5.1.3 Increase in Real-Time Payments

- 5.2 Market Challenges

- 5.2.1 Data security risks

- 5.3 Market Opportunities

- 5.3.1 Transformation to a Cashless Society

- 5.3.2 New players in the payment market may drive innovation leading to greater adoption.

- 5.4 Key Regulations and Standards in the Digital Payments Industry

- 5.5 Analysis of major case studies and use-cases

- 5.6 Analysis of key demographic trends and patterns related to payments industry in North America (Coverage to include Population, Internet Penetration, Banking Penetration/Unbanking Population, Age & Income etc.)

- 5.7 Analysis of the increasing emphasis on customer satisfaction and convergence of global trends in North America

- 5.8 Analysis of cash displacement and rise of contactless payment modes in North America

6 Market Segmentation

- 6.1 By Mode of Payment

- 6.1.1 Point of Sale

- 6.1.1.1 Card Payments (includes Debit Cards, Credit Cards, Bank Financing Prepaid Cards)

- 6.1.1.2 Digital Wallet (includes Mobile Wallets)

- 6.1.1.3 Cash

- 6.1.1.4 Others

- 6.1.2 Online Sale

- 6.1.2.1 Card Payments (includes Debit Cards, Credit Cards, Bank Financing Prepaid Cards)

- 6.1.2.2 Digital Wallet (includes Mobile Wallets)

- 6.1.2.3 Others (includes Cash on Delivery, Bank Transfer, and Buy Now, Pay Later)

- 6.1.1 Point of Sale

- 6.2 By End-user Industry

- 6.2.1 Retail

- 6.2.2 Entertainment

- 6.2.3 Healthcare

- 6.2.4 Hospitality

- 6.2.5 Other End-user Industries

- 6.3 By Country

- 6.3.1 United States

- 6.3.2 Canada

7 Competitive Landscape

- 7.1 Company Profiles

- 7.1.1 PayPal Holdings Inc.

- 7.1.2 MasterCard Incorporated (MasterCard)

- 7.1.3 Dwolla

- 7.1.4 Amazon.com Inc.

- 7.1.5 Visa Inc.

- 7.1.6 Alipay.com Co. Ltd

- 7.1.7 Alphabet Inc. (Apple Pay)

- 7.1.8 Google Pay (Google LLC)

- 7.1.9 Beacon Payments LLC

- 7.1.10 Interac Corp.

8 Investment Analysis

9 Future Outlook of the Market