Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693515

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693515

India Urea - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 166 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

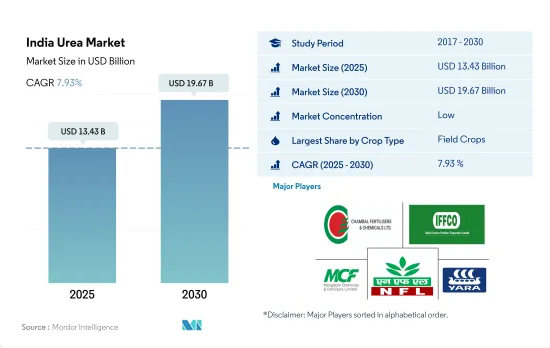

The India Urea Market size is estimated at 13.43 billion USD in 2025, and is expected to reach 19.67 billion USD by 2030, growing at a CAGR of 7.93% during the forecast period (2025-2030).

The rising consumption of urea in all crop types and increasing demand for highly efficient fertilizers are expected to boost the urea fertilizer market

- In India, field crops alone account for about 89.3% value share of the total urea fertilizer market and consumed about 89.7% of conventional urea fertilizers in 2022 due to their low cost and widespread availability in the country. However, in field crops, there is an increasing trend in adopting specialty urea fertilizers due to their efficiency. Due to this, its market value is projected to register a CAGR of 7.8% between 2023 and 2030.

- Horticulture crops account for about 10.2% of the total urea fertilizer market, which was valued at USD 1.2 billion in 2022. India is the world's second-largest producer of fruits and vegetables, and the country ranks first in banana, mango, lemon, papaya, and okra. The rising demand for fruits and vegetables, coupled with the expansion of cultivation area, is anticipated to drive the growth of the market.

- Since the last few decades, there has been an increase in nitrogen application rates and a decrease in nitrogen use efficiency. It is estimated that fertilizer consumption in India may double by 2050, and there is an urgent need to improve the country's fertilizer use efficiency. The controlled-release fertilizers can improve fertilizer use efficiency and decrease fertilizer pollution, particularly in horticultural crops. These factors are anticipated to fuel the growth of control-release fertilizers in all crop segments in the coming years.

- The floriculture has been one of the growing industries in recent years. For instance, in 2020-21, the country exported 15.6 thousand metric tons of floriculture products for a total value of USD 7.8 million. The rising domestic and international demand for flowers is expected to increase the market value of turf and ornamental crops at 7.1% CAGR from 2023 to 2030.

India Urea Market Trends

Manganese deficiency is a common problem in European countries, which most frequently affects sandy and organic soils with a pH above 6

- The area under field crop cultivation in the country increased by 3.5% during 2017-2022. The increased cultivation of cereals, pulses, and oilseeds in the country due to the rising consumer demand domestically and internationally is the major driving factor for the rising acreage.

- By crop type, rice, wheat, and soybean occupied the largest area under cultivation in the country, accounting for 47 million ha, 31.1 million ha, and 12.3 million ha in 2022. Rice is the most important food crop of India, covering about one-fourth of the total cropped area and providing food to about half of the Indian population. It is cultivated in almost all the states of the country, mainly in West Bengal, Uttar Pradesh, Andhra Pradesh, Punjab, and Tamil Nadu.

- Accordingly, rice consumption in the country increased from 95.8 million tons in 2016 to 107 million tons in 2022, which shows the rising demand for the crop in the country. This trend is further anticipated to drive the demand for fertilizers during 2023-2030. Similarly, wheat cultivation in the country increased from 98.5 million tons in 2017 to 107.6 million tons in 2020. It is cultivated majorly in Punjab, West Bengal, Haryana, and Rajasthan. Wheat is the second most important cereal crop in India and plays a vital role in the food and nutritional security of the country. Therefore, the intense cereal cultivation in the country, coupled with rising domestic and international demand, is anticipated to drive the Indian fertilizer market during 2023-2030.

Among the primary nutrients, nitrogen is the most-applied nutrient in field crops.

- In 2022, the average application rate for primary nutrients stood at 125.1 kg/ha. Notably, nitrogen topped the list with an average application rate of 223.5 kg/ha. Given its significance as a primary nutrient, nitrogen plays a pivotal role in supporting high-yield crops like rice, which is extensively cultivated in the country. However, nutrient deficiencies, particularly in nitrogen, are hampering rice productivity nationwide. The soil health in India, as highlighted in the State of Biofertilizers and Organic Fertilizers report, is a cause for concern. It reveals a rising reliance on chemical fertilizers, with 97.0%, 83.0%, and 71.0% of tested soils showing deficiencies in nitrogen, phosphorous, and potassium, respectively.

- Among the major crops, wheat, rice, and corn/maize led the pack in nutrient application rates in 2022, averaging 231, 156, and 149 kg/ha, respectively. Wheat and rice, being staple foods both domestically and globally, face challenges due to multiple nutrient deficiencies. Apart from nitrogen, phosphorous, and potassium, these crops also require micronutrients like sulfur, boron, iron, and zinc for optimal growth. Effective nutrient management is crucial for boosting crop production, thereby fueling market growth.

- Field crops, especially grains and cereals, have a voracious appetite for primary nutrients, particularly nitrogen fertilizers. Given the extensive cultivation of these crops in India, the soil's nutrient content is rapidly depleting. Consequently, farmers are increasingly relying on fertilizers to bridge the gap, a trend projected to drive the market from 2023 to 2030.

India Urea Industry Overview

The India Urea Market is fragmented, with the top five companies occupying 12.09%. The major players in this market are Chambal Fertilizers & Chemicals Ltd, Indian Farmers Fertiliser Cooperative Limited, Mangalore Chemicals & Fertilizers Ltd., National Fertilizers Ltd and Yara International ASA (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 92579

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Primary Nutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.1 Primary Nutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Speciality Type

- 5.1.1 CRF

- 5.1.1.1 Polymer Coated

- 5.1.1.2 Polymer-Sulfur Coated

- 5.1.1.3 Others

- 5.1.2 Liquid Fertilizer

- 5.1.3 SRF

- 5.1.4 Water Soluble

- 5.1.1 CRF

- 5.2 Crop Type

- 5.2.1 Field Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Turf & Ornamental

- 5.3 Form

- 5.3.1 Conventional

- 5.3.2 Speciality

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Chambal Fertilizers & Chemicals Ltd

- 6.4.2 Coromandel International Ltd.

- 6.4.3 Gujarat Narmada Valley Fertilizers & Chemicals Ltd

- 6.4.4 Indian Farmers Fertiliser Cooperative Limited

- 6.4.5 Mangalore Chemicals & Fertilizers Ltd.

- 6.4.6 National Fertilizers Ltd

- 6.4.7 Yara International ASA

- 6.4.8 Zuari Agro Chemicals Ltd

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.