PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035125

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035125

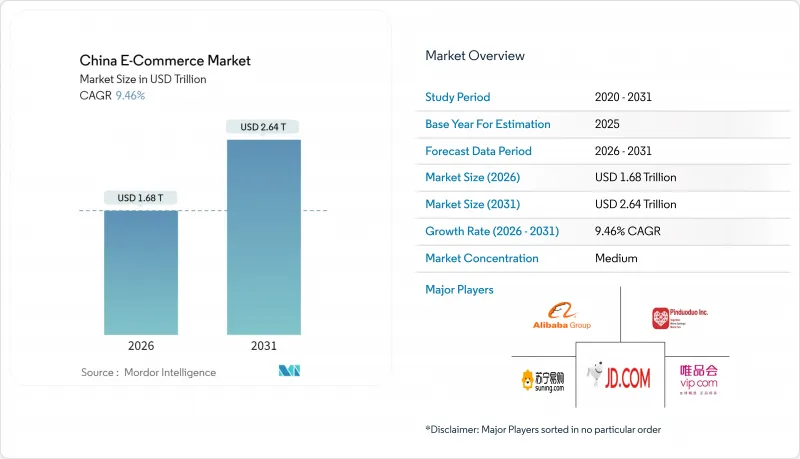

China E-Commerce - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The China e-commerce market reached USD 1.68 trillion in 2026 and is projected to climb to USD 2.64 trillion by 2031, translating into a 9.46% CAGR during the forecast period.

This performance places the China e-commerce market among the world's fastest-expanding large digital retail arenas, driven by live-stream shopping, cross-border duty exemptions and same-day grocery fulfillment. A pivot from saturated tier-1 metros toward lower-tier municipalities is unlocking disposable-income pools, while platform investment in mobile-first interfaces keeps transaction growth tightly linked to smartphone penetration. Regulatory tightening on monopolistic conduct is tempering margin upside, yet it is creating room for regional specialists and niche category platforms to scale. Intensifying competition among Alibaba, JD.com, Pinduoduo, Douyin and Kuaishou is compressing take-rates, but also accelerating innovation in AI-powered personalization and low-carbon logistics.

China E-Commerce Market Trends and Insights

Livestream Commerce Expansion in Lower-Tier Cities

Livestream shopping generated USD 807 billion in gross merchandise value during 2024 and is on track to sustain an 18% CAGR through 2026, with more than 60% of new live-stream buyers coming from tier-3 and smaller cities. Disposable income in these municipalities rose 5.8% year-on-year in H1 2024, giving residents greater spending power. Platforms such as Kuaishou and Douyin deploy local creators who speak regional dialects, strengthening trust and reducing the anonymity barrier that limits traditional marketplace conversion. As content becomes the storefront, agricultural goods and daily-use appliances that once lacked offline distribution reach see new demand. Pending Ministry of Commerce rules that require real-time disclosure of sponsored segments are expected to formalize influencer contracts and lift consumer confidence.

Same-Day Logistics Unlocking FMCG and Fresh Grocery Online

Fulfillment windows in Beijing, Shanghai and Shenzhen have fallen below 30 minutes thanks to hybrid supermarket-warehouse formats like JD 7Fresh and Alibaba Hema. Electric scooters and autonomous robots now handle the final leg, while cold-chain capacity expanded 22% in 2024 under state subsidy programs. Meituan Select's community group-buying model widened to 2,800 cities by year-end 2024, aggregating demand and slicing last-mile costs. Streamlined customs procedures introduced in 2025 shortened border clearance for imported fruit from 48 to 12 hours, enabling same-day delivery of premium berries and seafood. These advances shift grocery purchases from weekly offline stock-ups to high-frequency online baskets, stabilizing revenue streams for platforms.

Data-Privacy and Antitrust Regulations Curbing Monetization

Antitrust guidelines released in November 2025 outlaw forced exclusivity and demand transparency around algorithmic rankings. Coupled with stringent data-privacy rules that took effect in January 2025, platforms have had to redesign consent flows and reduce third-party data sharing. Compliance investments totaled CNY 2.8 billion (USD 390 million) for Alibaba in fiscal 2025, and merchant surveys point to 12-15% lower click-through rates on sponsored slots since the new rules. While trust gains with consumers are evident, short-term monetization suffers, trimming growth vectors for ad-supported revenue lines.

Other drivers and restraints analyzed in the detailed report include:

- Private-Traffic WeChat Mini-Program Enablement for SMEs

- Cross-Border Duty Exemption Boosting Imported Cosmetics

- Weak IP Enforcement Deterring Luxury Brand Presence

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Business-to-consumer transactions represented 87.24% of total sales in 2025, underscoring how retail-focused ecosystems such as Taobao, JD.com and Pinduoduo dominate the China e-commerce market. The business-to-business stream, however, is expanding at 11.37% per year, two percentage points faster than B2C, as industrial buyers migrate sourcing to cloud marketplaces that offer real-time supplier matching. The China e-commerce market size for B2B flows reached CNY 3 trillion (USD 420 billion) on Alibaba 1688.com in 2024, highlighting the depth of this structural shift. Factories in Henan and Anhui now integrate procurement APIs into ERP software, gaining price transparency that trims raw-material spend.

Enterprise buyers in Southeast Asia and Africa amplified cross-border B2B demand by 14% in 2024, using unified customs codes that cut paperwork 40%. The Ministry of Industry and Information Technology's industrial internet blueprint prioritizes SaaS procurement tools, channeling subsidies toward small manufacturers who previously relied on offline agents. As B2C growth moderates in saturated metros, the China e-commerce market gains a second engine from B2B digitization that carries lower marketing costs and higher order values. Content-driven commerce on Douyin and Kuaishou grabs consumer mindshare, but factory-floor purchasing decisions are increasingly shaped by AI-powered quote engines that recalibrate prices on the fly, suggesting a divergent yet complementary growth path for the China e-commerce industry.

Smartphones generated 67.57% of B2C turnover in 2025, confirming their role as the default gateway to the China e-commerce market. Ubiquitous 5G coverage, QR-code payments and mini-program ubiquity keep app dwell times high, with the average user spending 6.2 hours daily on mobile internet in 2024. The China e-commerce market size attributed to smartphones is forecast to climb at 10.12% CAGR through 2031, as 5G handset upgrades filter into inland cities and data-inclusive tariffs lower browsing costs.

Desktop and laptop sessions stabilized at roughly 32% of transactions, buoyed by buyers who prefer large screens for side-by-side product comparisons in electronics and furniture. Corporate procurement teams also favor desktops for bulk ordering, linking B2B platform usage to office hardware. Emerging devices such as smart TVs and voice assistants remain sub-5% but are gaining traction as IoT ecosystems like Xiaomi Youpin embed one-click replenishment. Platform design parity ensures promotions synchronize across screens, preventing leakage of shopper attention and sustaining multi-device engagement within the broader China e-commerce market.

The China E-Commerce Market Report is Segmented by Business Model (B2C, and B2B), Device Type for B2C (Smartphone/Mobile, Desktop and Laptop, and More), Payment Method for B2C (Credit and Debit Cards, Digital Wallets, BNPL, and More), Product Category for B2C (Beauty and Personal Care, Consumer Electronics, Fashion and Apparel, Food and Beverages, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Alibaba Group Holding Ltd.

- JD.com Inc.

- Pinduoduo Inc.

- Vipshop Holdings Ltd.

- Suning.com Co. Ltd.

- Meituan (Beijing) Technology Co., Ltd.

- Xingin Information Technology (Shanghai) Co., Ltd.

- Dangdang Inc.

- Mogu Inc.

- NetEase (Hangzhou) Network Co., Ltd.

- SHEIN (Roadget Business Pte. Ltd.)

- Kaola E-commerce (China) Co., Ltd.

- Hangzhou Weidian Technology Co., Ltd.

- Shanghai Shizhuang Information Technology Co., Ltd.

- Beijing DHgate Information Technology Co., Ltd

- 1688.com (Alibaba (China) Co., Ltd.)

- Beijing Xiaomi Electronic Products Co., Ltd

- Beijing Douyin Information Service Co., Ltd.

- Beijing Kuaishou Technology Co., Ltd.

- Ele.me (Shanghai Hummingbird Internet Technology Co., Ltd.)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Livestream commerce expansion in lower-tier cities

- 4.2.2 Same-day logistics unlocking FMCG and fresh grocery online

- 4.2.3 Private-traffic WeChat mini-program enablement for SMEs

- 4.2.4 Cross-border duty exemption boosting imported cosmetics

- 4.2.5 AI-driven personalised sizing solutions reducing returns

- 4.2.6 Renewable-energy powered data-centres enhancing ESG appeal

- 4.3 Market Restraints

- 4.3.1 Data-privacy and anti-trust regulations curbing monetisation

- 4.3.2 Weak IP enforcement deterring luxury brand presence

- 4.3.3 Mobile-internet user saturation in tier-1 cities

- 4.3.4 Cross-border carbon tariffs inflating shipping costs

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Macroeconomic Trends on the Market

- 4.9 Key Market Trends and E-commerce Share of Total Retail

- 4.10 Demographic Trends (Population, Internet, Age, Income)

- 4.11 Cross-Border E-commerce Analysis

- 4.12 China's Position in Asia Pacific E-commerce

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Business Model

- 5.1.1 B2C

- 5.1.2 B2B

- 5.2 By Device Type (B2C)

- 5.2.1 Smartphone / Mobile

- 5.2.2 Desktop and Laptop

- 5.2.3 Other Device Types

- 5.3 By Payment Method (B2C)

- 5.3.1 Credit and Debit Cards

- 5.3.2 Digital Wallets

- 5.3.3 Buy Now Pay Later (BNPL)

- 5.3.4 Other Payment Methods

- 5.4 By Product Category (B2C)

- 5.4.1 Beauty and Personal Care

- 5.4.2 Consumer Electronics

- 5.4.3 Fashion and Apparel

- 5.4.4 Food and Beverages

- 5.4.5 Furniture and Home

- 5.4.6 Toys, DIY and Media

- 5.4.7 Other Product Categories

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Alibaba Group Holding Ltd.

- 6.4.2 JD.com Inc.

- 6.4.3 Pinduoduo Inc.

- 6.4.4 Vipshop Holdings Ltd.

- 6.4.5 Suning.com Co. Ltd.

- 6.4.6 Meituan (Beijing) Technology Co., Ltd.

- 6.4.7 Xingin Information Technology (Shanghai) Co., Ltd.

- 6.4.8 Dangdang Inc.

- 6.4.9 Mogu Inc.

- 6.4.10 NetEase (Hangzhou) Network Co., Ltd.

- 6.4.11 SHEIN (Roadget Business Pte. Ltd.)

- 6.4.12 Kaola E-commerce (China) Co., Ltd.

- 6.4.13 Hangzhou Weidian Technology Co., Ltd.

- 6.4.14 Shanghai Shizhuang Information Technology Co., Ltd.

- 6.4.15 Beijing DHgate Information Technology Co., Ltd

- 6.4.16 1688.com (Alibaba (China) Co., Ltd.)

- 6.4.17 Beijing Xiaomi Electronic Products Co., Ltd

- 6.4.18 Beijing Douyin Information Service Co., Ltd.

- 6.4.19 Beijing Kuaishou Technology Co., Ltd.

- 6.4.20 Ele.me (Shanghai Hummingbird Internet Technology Co., Ltd.)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment