PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844609

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844609

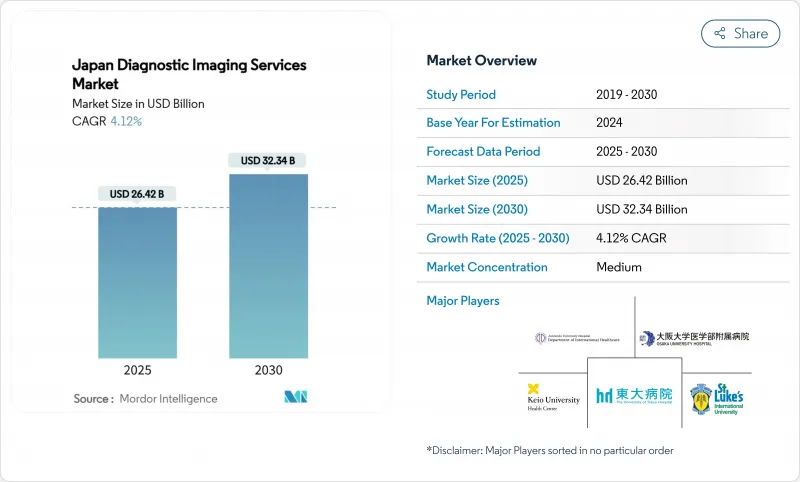

Japan Diagnostic Imaging Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Japan Diagnostic Imaging Services Market size is estimated at USD 26.42 billion in 2025, and is expected to reach USD 32.34 billion by 2030, at a CAGR of 4.12% during the forecast period (2025-2030).

The upward trajectory is propelled by the country's super-aged demographic structure, rapid diffusion of artificial intelligence across imaging workflows, and steady capital spending on modality upgrades despite hospital budget constraints. Consistent volume growth across X-ray, CT, MRI, ultrasound, and nuclear imaging counters workforce shortages by encouraging efficiency-boosting technologies such as triage algorithms and structured reporting. Portable ultrasound and flat-panel detector (FPD) radiography widen access in smaller facilities, while teleradiology hubs narrow urban-rural gaps. The combined effect is that the Japan diagnostic imaging services market now operates at the crossroads of population pressure and digital transformation, creating parallel opportunities for equipment vendors, software developers, and service providers prepared to embrace outcome-based care models.

Japan Diagnostic Imaging Services Market Trends and Insights

Rapid Expansion of AI-Reimbursed Imaging Procedures

Japan's 2024 reimbursement reform covering computer-aided detection (CAD) tools transformed imaging economics by neutralizing adoption costs for hospitals and imaging centers. Early adopters report 30% faster read times and higher lesion-detection sensitivity, enabling facilities to handle more studies without increasing radiologist headcount. The policy especially benefits high-volume mammography, chest CT, and gastrointestinal endoscopy programs where throughput gains translate into direct revenue. Seamless PACS integration and cloud deployment allow rapid scaling across institutions, positioning first movers to consolidate referral networks. As additional modalities secure coverage, the Japan diagnostic imaging services market is expected to record accelerated AI deployment, reinforcing productivity gains while improving diagnostic standardization.

Accelerating Replacement of Aging Analog Units With DR/FPD X-Ray Systems

More than 60% of rural hospitals were still operating cassette-based radiography units in 2024, prompting a nationwide push toward FPD systems that cut radiation dose by up to 36% and boost exam throughput by 25%. Government subsidies and vendor-backed financing mitigate up-front capital needs, particularly for sub-100-bed facilities that face tight budgets. Fast image availability shortens patient wait times, while automated exposure settings raise image consistency, easing radiologist workload. The modernization wave enlarges the addressable equipment base for manufacturers and underpins steady service contract revenue, reinforcing the evolution of the Japan diagnostic imaging services market toward fully digital workflows.

Soaring Physicist & Radiologist Shortages Constrain Scanner Utilisation

Only 8,610 radiologists are available nationwide, far below demand, with attrition now running at 3% annually. Staffing gaps force many scanners to sit idle during evenings and weekends, capping throughput at 60% of potential capacity in some prefectures. The shortage also slows the rollout of advanced modalities that require sub-specialty expertise, thereby tempering the expansion pace of the Japan diagnostic imaging services market. AI triage tools alleviate but do not eliminate the constraint, as final reads still require certified physicians.

Other drivers and restraints analyzed in the detailed report include:

- Government Stimulus for Rural Teleradiology Hubs

- Rising Chronic-Disease Workload in Super-Aged Prefectures

- Lengthy PMDA Approval Cycles for SaMD/AI Algorithms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

X-ray retained 31.86% of the Japan diagnostic imaging services market share in 2024, generating stable revenue from routine chest, skeletal, and abdominal studies. Portable FPD systems now penetrate emergency departments and nursing homes, lifting daily exam counts and reducing patient transfer needs. In parallel, the Japan diagnostic imaging services market size for ultrasound is projected to expand briskly as Compact 5000 series platforms enable cardiology, obstetrics, and point-of-care assessments at the bedside.

Ultrasound's 5.16% CAGR is further supported by AI modules that automate left-ventricular ejection fraction and thyroid nodule classification, freeing clinicians to focus on complex findings. CT and MRI remain indispensable for oncology staging and neurologic workups, yet their growth is moderated by price ceilings and staffing limits. Nuclear imaging benefits from GE HealthCare's acquisition of the remaining stake in Nihon Medi-Physics, which secures domestic radioisotope supply and safeguards continuity for cardiology SPECT and PET oncology protocols.

The Japan Diagnostic Imaging Services Market Report is Segmented by Modality (MRI, CT, Ultrasound, X-Ray, Nuclear Imaging, Fluoroscopy, Mammography), Application (Cardiology, Oncology, Neurology, Orthopedics, Gastroenterology, Gynecology, Other Applications), Service Provider (Hospitals, Diagnostic Imaging Centers, Clinics and Specialty Centers, Others). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- The University of Tokyo Hospital

- St. Luke's International Hospital

- Keio University Hospital

- Osaka University Hospital

- National Cancer Center Hospital

- Juntendo University Hospital

- Kobe University Hospital

- Tohoku University Hospital

- Yokohama City Univ. Medical Center

- Sapporo Medical Univ. Hospital

- Nagoya University Hospital

- Kyoto University Hospital

- Chiba University Hospital

- Fukuoka University Hospital

- Okayama University Hospital

- Niigata University Medical Hospital

- Kagoshima University Hospital

- Gunma University Hospital

- Hiroshima University Hospital

- Akita University Hospital

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Expansion of AI-Reimbursed Imaging Procedures

- 4.2.2 Accelerating Replacement of Aging Analog Units With DR/FPD X-Ray Systems

- 4.2.3 Government Stimulus for Rural Teleradiology Hubs

- 4.2.4 Rising Chronic-Disease Workload in Super-Aged Prefectures

- 4.2.5 Vendor Financing & Pay-Per-Scan Business Models

- 4.2.6 Surge In Demand for Pre-Therapeutic Imaging in Proton-Beam & CAR-T Centers

- 4.3 Market Restraints

- 4.3.1 Soaring Physicist & Radiologist Shortages Constrain Scanner Utilisation

- 4.3.2 Lengthy PMDA Approval Cycles for Samd/AI Algorithms

- 4.3.3 High Total Cost of Ownership for Multi-Slice CT & 3 T MRI In Sub-100-Bed Hospitals

- 4.3.4 Rising Public Anxiety Over Cumulative Radiation Dose

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers / Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Modality

- 5.1.1 MRI

- 5.1.2 CT

- 5.1.3 Ultrasound

- 5.1.4 X-Ray

- 5.1.5 Nuclear Imaging

- 5.1.6 Fluoroscopy

- 5.1.7 Mammography

- 5.2 By Application

- 5.2.1 Cardiology

- 5.2.2 Oncology

- 5.2.3 Neurology

- 5.2.4 Orthopedics

- 5.2.5 Gastroenterology

- 5.2.6 Gynecology

- 5.2.7 Other Applications

- 5.3 By Service Provider

- 5.3.1 Hospitals

- 5.3.2 Diagnostic Imaging Centers

- 5.3.3 Clinics and Specialty Centers

- 5.3.4 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 The University of Tokyo Hospital

- 6.3.2 St. Luke's International Hospital

- 6.3.3 Keio University Hospital

- 6.3.4 Osaka University Hospital

- 6.3.5 National Cancer Center Hospital

- 6.3.6 Juntendo University Hospital

- 6.3.7 Kobe University Hospital

- 6.3.8 Tohoku University Hospital

- 6.3.9 Yokohama City Univ. Medical Center

- 6.3.10 Sapporo Medical Univ. Hospital

- 6.3.11 Nagoya University Hospital

- 6.3.12 Kyoto University Hospital

- 6.3.13 Chiba University Hospital

- 6.3.14 Fukuoka University Hospital

- 6.3.15 Okayama University Hospital

- 6.3.16 Niigata University Medical Hospital

- 6.3.17 Kagoshima University Hospital

- 6.3.18 Gunma University Hospital

- 6.3.19 Hiroshima University Hospital

- 6.3.20 Akita University Hospital

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment