PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844673

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844673

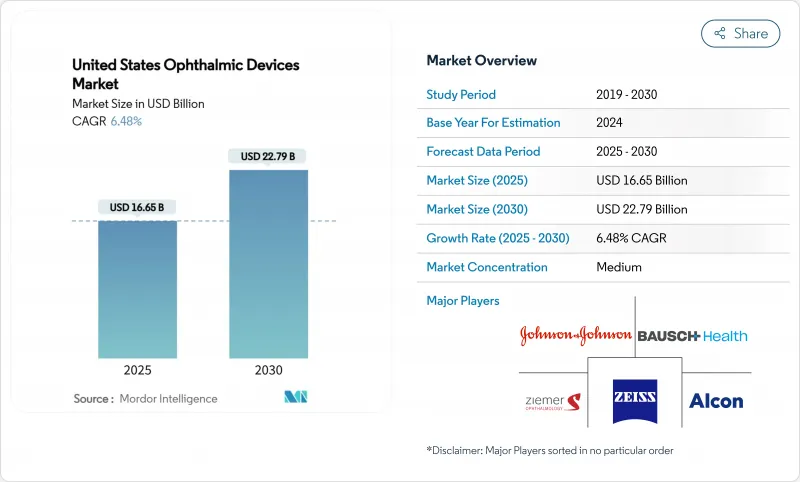

United States Ophthalmic Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The United States ophthalmic devices market size is valued at USD 16.65 billion in 2025 and is forecast to reach USD 22.7 billion by 2030, advancing at a 6.48% CAGR over the period.

Rising cataract volumes among adults over 65 years, broader insurance coverage, and continuous upgrades in imaging software collectively underpin this steady expansion. Surgical devices currently command 42.1% of revenue because they enable high-margin refractive, cataract, and glaucoma procedures that few hospitals can defer. Ambulatory surgical centers are the fastest-growing end-user channel, registering a 5.23% CAGR as payers and patients migrate from inpatient to outpatient settings that deliver comparable outcomes at lower cost. Meanwhile, the premium intraocular-lens boom and the rapid adoption of autonomous AI screening tools are reshaping purchasing criteria, prompting device makers to bundle hardware, analytics, and cloud connectivity for lifecycle differentiation.

United States Ophthalmic Devices Market Trends and Insights

Demographic Shift: Myopia & Diabetic Eye-Disease Surge Driving Diagnostic Demand

An aging and increasingly myopic population is materially lifting diagnostic volumes across the United States ophthalmic devices market. Projections indicate that one in two Americans will be myopic by 2050, encouraging payers to consider classifying high myopia as a chronic disease. The diabetic-retinopathy population doubled between 2004 and 2024 to 9.6 million, yet sight-threatening events declined because earlier screening now redirects patients to treatment sooner. Autonomous fundus-photography algorithms installed in community clinics are central to this progress, reducing referral delays and widening access in rural counties.

Rapid Uptake of Premium Cataract & Refractive IOLs Transforming Surgical Outcomes

Surgeons have embraced presbyopia-correcting and extended-depth-of-focus lenses to meet patient demand for spectacle independence. The 2022 ESCRS survey showed a 4% rise in presbyopia-correcting IOL use since 2016, while bifocal models fell to 2% as newer optics improved contrast sensitivity. Johnson & Johnson's TECNIS Odyssey lens, launched in September 2024, already treats more than 14,000 eyes, delivering double the low-light contrast versus earlier multifocal implants. This accelerated turnover drives the United States ophthalmic devices market because surgeons often pair premium lenses with upgraded phaco consoles calibrated for precise lens positioning.

High Capital Outlay for Advanced Diagnostic Suites Limiting Adoption

A full diagnostic bay comprising OCT, corneal topography, and automated refraction can cost more than USD 500,000, straining budgets at independent practices that lack large ASC volumes. With many states seeing flat professional-service fees, these providers hesitate to commit capital that may depreciate in under seven years. Leasing and pay-per-use models mitigate risk, yet present back-office complexity because fees fluctuate with patient load. Consequently, growth in the United States ophthalmic devices market is uneven, with small offices deferring purchases until AI software updates justify their return on investment.

Other drivers and restraints analyzed in the detailed report include:

- Growth of AI-based OCT & Fundus Imaging Platforms Revolutionizing Diagnostics

- Expansion of Minimally-Invasive Glaucoma Surgery (MIGS) Implants Driving Surgical Innovation

- FDA Stringency on Femtosecond & Excimer Laser Upgrades Slowing Innovation Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Surgical systems generated 42.11% of revenue in 2024 and remain the anchor of the United States ophthalmic devices market because they combine high upfront prices and recurring consumables. The strong performance benefits from sustained premium-IOL penetration, which boosts per-procedure value and nudges surgeons to purchase consoles optimized for toric alignment and astigmatic correction. Networks of ambulatory surgical centers also favor modular femtosecond platforms that fit compact operating rooms. This steady replacement cycle lifts the surgical slice of United States ophthalmic devices market size whenever surgeons retire aging phaco units to support combined MIGS-and-cataract workflows.

Conversely, vision-care devices still dominate unit volumes, accounting for 63.21% of shipments in 2024, yet price erosion and online spectacles discounting limit their value contribution. Contact-lens makers respond with silicone-hydrogel materials that extend oxygen permeability, extending wear times and lowering dropout rates. As users reorder lenses quarterly, suppliers secure predictable cash flow that finances incremental research. The virtuous feedback loop sustains category leadership without materially altering the overall profit mix of the United States ophthalmic devices market.

The United States Ophthalmic Devices Market Report is Segmented by Device Type (Diagnostic & Monitoring Devices, Surgical Devices, and Vision Care Devices), Disease Indication (Cataract, Glaucoma, Diabetic Retinopathy, Other Disease Indications), End-User (Hospitals, Specialty Ophthalmic Clinics, and More. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Alcon

- Johnson & Johnson

- Bausch + Lomb Corp.

- Carl Zeiss

- EssilorLuxottica

- Hoya Corp.

- CooperVision Inc.

- Glaukos Corp.

- Topcon Corp.

- Nidek

- Ziemer Group

- Heidelberg Engineering

- Lumenis

- Lensar Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Demographic Shift: Myopia & Diabetic Eye Disease Surge in the U.S.

- 4.2.2 Rapid Uptake of Premium Cataract & Refractive IOLs

- 4.2.3 Medicare Reimbursement Stability for Cataract Surgery

- 4.2.4 Growth of AI-based OCT & Fundus Imaging Platforms

- 4.2.5 Expansion of Minimally-Invasive Glaucoma Surgery (MIGS) Implants

- 4.3 Market Restraints

- 4.3.1 High Capital Outlay for Advanced Diagnostic Suites

- 4.3.2 FDA Stringency on Femtosecond & Excimer Laser Upgrades

- 4.3.3 Limited Private Insurance Coverage for Premium Vision Correction

- 4.3.4 Consolidated Supplier Base Driving Component Costs

- 4.4 Regulatory Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Device Type

- 5.1.1 Diagnostic & Monitoring Devices

- 5.1.1.1 OCT Scanners

- 5.1.1.2 Fundus & Retinal Cameras

- 5.1.1.3 Autorefractors & Keratometers

- 5.1.1.4 Corneal Topography Systems

- 5.1.1.5 Ultrasound Imaging Systems

- 5.1.1.6 Perimeters & Tonometers

- 5.1.1.7 Other Diagnostic & Monitoring Devices

- 5.1.2 Surgical Devices

- 5.1.2.1 Cataract Surgical Devices

- 5.1.2.2 Vitreoretinal Surgical Devices

- 5.1.2.3 Refreactive Surgical Devices

- 5.1.2.4 Glaucoma Surgical Devices

- 5.1.2.5 Other Surgical Devices

- 5.1.3 Vision Care Devices

- 5.1.3.1 Spectacles Frames & Lenses

- 5.1.3.2 Contact Lenses

- 5.1.1 Diagnostic & Monitoring Devices

- 5.2 By Disease Indication

- 5.2.1 Cataract

- 5.2.2 Glaucoma

- 5.2.3 Diabetic Retinopathy

- 5.2.4 Other Disease Indications

- 5.3 By End-user

- 5.3.1 Hospitals

- 5.3.2 Specialty Ophthalmic Clinics

- 5.3.3 Ambulatory Surgery Centers (ASCs)

- 5.3.4 Other End-users

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Alcon Inc.

- 6.3.2 Johnson & Johnson Vision Care Inc.

- 6.3.3 Bausch + Lomb Corp.

- 6.3.4 Carl Zeiss Meditec AG

- 6.3.5 EssilorLuxottica SA

- 6.3.6 Hoya Corp.

- 6.3.7 CooperVision Inc.

- 6.3.8 Glaukos Corp.

- 6.3.9 Topcon Corp.

- 6.3.10 Nidek Co. Ltd

- 6.3.11 Ziemer Ophthalmic Systems AG

- 6.3.12 Heidelberg Engineering GmbH

- 6.3.13 Lumenis Be Ltd

- 6.3.14 Lensar Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment