PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850191

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850191

UK Contraceptive Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

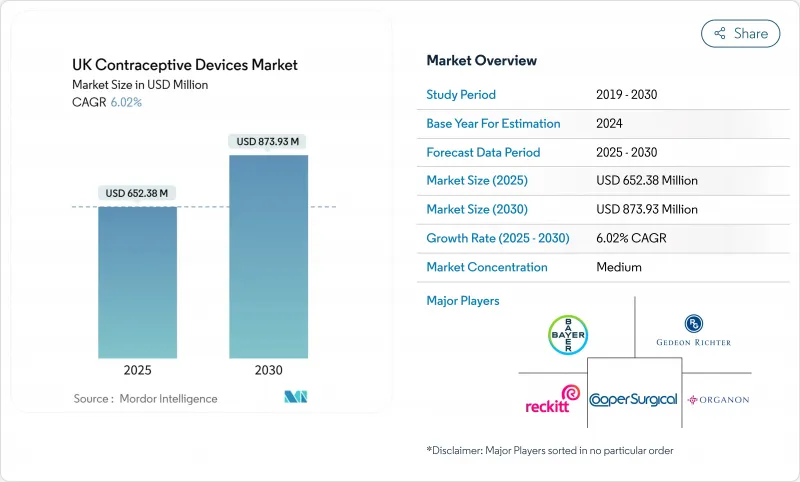

The UK contraceptive devices market reached USD 652.38 million in 2025 and is forecast to climb to USD 873.94 million in 2030, advancing at a 6.02% CAGR.

This expansion reflects the National Health Service's (NHS) preventive-care emphasis, a regulatory climate that rewards product safety, and persistent demographic trends that sustain demand for reliable birth-control technologies. Rising sexually transmitted infection (STI) rates, notably the 85,223 gonorrhoea diagnoses recorded in 2023, keep dual-protection methods such as condoms squarely in focus.The Medicines and Healthcare products Regulatory Agency (MHRA) intensified post-market surveillance rules in 2024, raising entry barriers yet reinforcing end-user confidence in device quality. Meanwhile, the January 2024 policy that allows pharmacists to dispense oral contraceptives without a general-practitioner consultation has accelerated over-the-counter (OTC) and online sales channels. Together, these forces position the UK contraceptive devices market for steady medium-term growth despite public-sector budget constraints and periodic supply bottlenecks.

UK Contraceptive Devices Market Trends and Insights

High Prevalence of STIs & Rising Awareness

England alone logged 401,800 STI cases in 2023, a 4.7% year-on-year increase, keeping barrier methods at the centre of preventive policy. Gonorrhoea cases have reached their highest level since 1918, while 52 antibiotic-resistant strains had been identified by mid-2025. Public-health messaging now frames condoms as dual-function tools that curb both pregnancies and infections, boosting unit volumes in the UK contraceptive devices market. National surveillance also shows that 46% of new STI cases occur in the 15-24 age bracket, prompting age-specific outreach campaigns.Local authorities, citing resource strain, increasingly promote self-care and home-delivery condom programmes, reinforcing a preventive mindset.

Increasing Unintended Pregnancies & UK-Wide Public-Health Drives

UK reproductive-health profiles show long-acting reversible contraception (LARC) uptake among women under 25 rising from 27.6% in 2019 to 36.2% in 2023, yet overall utilisation remains below pre-pandemic levels. Scotland's bridging-contraception initiative delivers three-month supplies of progestogen-only pills through pharmacies, eliminating appointment delays and widening access. Parallel educational reforms mandate comprehensive relationships and sex education in schools, ensuring that the emerging adult cohort enters the UK contraceptive devices market with higher baseline awareness parliament.uk. Together, these programmes create latent demand for a diverse product mix that extends beyond condoms to LARCs, rings, and diaphragms.

Device-Related Adverse Effects & Discontinuation

Heightened media attention on safety concerns, such as the meningioma risk linked to prolonged use of certain injectable progestogens, has raised discontinuation rates for some methods. The MHRA now obliges manufacturers to submit granular adverse-event reports within strict timelines, elevating compliance costs but also improving post-market data transparency. Professional societies such as the British Society of Urogynaecology actively encourage clinicians to report device complications, further sensitising the public to possible side effects. While long-acting progestogen therapies can reduce repeat interventions, risk-benefit calculations have become more nuanced, leading some women to revert to condoms or non-hormonal methods.

Other drivers and restraints analyzed in the detailed report include:

- Government Support for Reproductive and Family-Planning Services

- Consumer Shift Toward OTC & E-Pharmacy Fulfilment

- NHS Funding Pressure Causing Supply Bottlenecks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The segment generated 55.89% of UK contraceptive devices market revenue in 2024, underscoring condoms' strong dual-protection value proposition and extensive retail availability. The UK contraceptive devices market size for condoms amounted to USD 365.2 million in 2025, and volumes stay resilient as STI control remains a public-health priority. Intra-uterine devices (IUDs) are the fastest-growing line, advancing at a 9.03% CAGR to 2030, bolstered by extended wear times and favourable cost-utility ratios. Bayer's Mirena and Kyleena systems now carry eight-year licences, a milestone that reduces replacement frequency and elevates lifetime adherence. Regulatory confidence also surfaced in 2024 when the Levosert hormonal IUS secured its own eight-year extension, signalling a high safety-efficacy threshold for hormonal platforms.

Innovations in non-hormonal technology add breadth to the category. The contoured Caya diaphragm, already registered in nearly 40 countries, demonstrates high acceptability in pilot studies and offers a silicone-free alternative for latex-sensitive users. Research published in Advanced Materials shows promise for stimuli-responsive hydrogels that produce reversible fallopian-tube occlusion, hinting at future patient-controlled sterilisation modalities. Vaginal rings are evolving beyond hormone-delivery systems; Bayer is co-developing a ferrous-gluconate-based ring that impedes sperm motility without altering hormonal balance. These R&D pipelines widen the technology mix, enabling manufacturers to address both safety concerns and emerging lifestyle preferences.

UK Contraceptive Devices Market Report is Segmented by Type (Condoms, Diaphragms & Cervical Caps, Vaginal Rings, Intra Uterine Devices, Implants & Injectables, Spermicidal Devices and Other Types), Gender (Male and Female) and Distribution Channel (NHS & Community Sexual-Health Clinics, Retail Pharmacies, Online Pharmacies & E-Commerce, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Bayer

- The Cooper Companies

- Pfizer

- Organon

- Gedeon Richter Plc.

- Reckitt Benckiser Group plc (Durex)

- Pregna International Ltd.

- Karex Berhad

- Okamoto Industries Inc.

- Femcap Inc

- Lifestyle Healthcare Pte Ltd

- Pasante Healthcare Ltd

- Relarc BV

- LTC Healthcare

- Skins Sexual Health

- KESSEL medintim GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High prevalence of STDs & rising awareness

- 4.2.2 Increasing unintended pregnancies & UK-wide public-health drives

- 4.2.3 Government support for Reproductive and Family Planning services

- 4.2.4 Consumer shift toward OTC & e-pharmacy fulfilment

- 4.2.5 Growth Demand for LARCs and Innovative Devices

- 4.2.6 Integration of Contraception with Digital Health Platforms

- 4.3 Market Restraints

- 4.3.1 Device-related adverse effects & discontinuation

- 4.3.2 Sociocultural resistance among specific faith & ethnic groups

- 4.3.3 NHS funding pressure causing supply bottlenecks

- 4.3.4 Regulatory and Privacy Challenges Amid Digital Contraceptive Solutions

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technology Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Type

- 5.1.1 Condoms

- 5.1.2 Diaphragms & Cervical caps

- 5.1.3 Vaginal Rings

- 5.1.4 Intra-Uterine Devices

- 5.1.5 Implants & Injectables

- 5.1.6 Spermicidal Devices

- 5.1.7 Other Types

- 5.2 By Gender

- 5.2.1 Male

- 5.2.2 Female

- 5.3 By Distribution Channel

- 5.3.1 NHS & Community Sexual-Health Clinics

- 5.3.2 Retail Pharmacies

- 5.3.3 Online Pharmacies & e-commerce

- 5.3.4 Supermarkets & Convenience Stores

- 5.3.5 Others (Charities, Youth Centres)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 Bayer AG

- 6.3.2 Cooper Surgical Inc.

- 6.3.3 Pfizer Inc.

- 6.3.4 Organon & Co.

- 6.3.5 Gedeon Richter Plc.

- 6.3.6 Reckitt Benckiser Group plc (Durex)

- 6.3.7 Pregna International Ltd.

- 6.3.8 Karex Berhad

- 6.3.9 Okamoto Industries Inc.

- 6.3.10 Femcap Inc

- 6.3.11 Lifestyle Healthcare Pte Ltd

- 6.3.12 Pasante Healthcare Ltd

- 6.3.13 Relarc BV

- 6.3.14 LTC Healthcare

- 6.3.15 Skins Sexual Health

- 6.3.16 KESSEL medintim GmbH

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment