PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906017

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906017

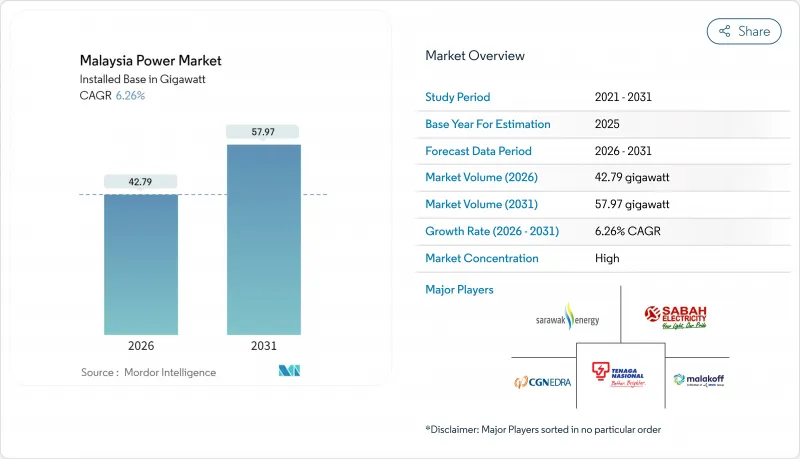

Malaysia Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

Malaysia Power Market size in 2026 is estimated at 42.79 gigawatt, growing from 2025 value of 40.27 gigawatt with 2031 projections showing 57.97 gigawatt, growing at 6.26% CAGR over 2026-2031.

Hyperscale data-center clusters account for 11 GW of new load applications, a figure that has doubled in only two years and is forcing Tenaga Nasional Berhad (TNB) to accelerate generation and grid investments. While thermal technologies maintained 75.6% of the Malaysian power market in 2024, renewables are the fastest-growing through 2030 and will re-allocate capital toward solar, hydro, and battery projects at the expense of coal. Third-party access rules are shifting procurement power to corporate consumers, and tariff-subsidy reforms are aligning prices with cost recovery, which, in turn, improves the economics of distributed solar. Semiconductor fabrication and cloud infrastructure hubs in Penang, Selangor, and Johor underpin sustained industrial demand, yet natural-gas supply constraints and curtailment risk in weak East Malaysia grids serve as headline uncertainties.

Malaysia Power Market Trends and Insights

Industrial Electricity-Demand Surge

Infineon's EUR 2 billion silicon-carbide fab in Kulim exemplifies the structural shift from legacy petrochemicals toward precision manufacturing that now underpins the Malaysian power market. TNB has confirmed that data-center applications alone total 11 GW, compelling the utility to reserve 30% of its RM 16.3 billion contingent capital expenditure for unanticipated load growth. Industrial demand is expected to maintain half of total consumption through 2030, but the composition tilts toward semiconductor and cloud workloads that require low-carbon electricity. Any lapse in generation or transmission build-out risks divesting these investments to regional competitors with more advanced renewable procurement frameworks. Consequently, local authorities are fast-tracking substation upgrades and incentivizing battery storage to keep reserve margins adequate.

Renewable-Energy Capacity Targets

The National Energy Transition Roadmap sets milestones of 31% renewable capacity by 2025 and 40% by 2035. Achieving these goals requires annual additions near 1.5 GW, notably faster than historical build-out rates. Large-Scale Solar Round 5 allocated 2 GW in 2024 to Malaysian-controlled bidders, favoring domestic content capture but narrowing the developer field. TNB's 2.5 GW floating-solar program across hydro reservoirs leverages existing transmission corridors and minimizes land-use conflicts, while Sarawak Energy's 7,300 MW hydro fleet positions East Malaysia as a potential clean-power exporter once cross-border interconnections advance. The 70% renewable aspiration by 2050 implies near-zero coal, with hydrogen-ready combined-cycle gas turbines providing a bridge technology, albeit with fuel-supply uncertainties.

Natural-Gas Supply Constraints and Price Volatility

Domestic gas production has plateaued, and Petronas prioritizes LNG exports, resulting in periodic fuel shortages that force generators to switch to costlier diesel back-up.When global LNG prices spiked in 2022, Malaysia's tariff-pass-through mechanism lagged fuel costs, compressing IPP margins. Planned hydrogen-ready turbines assume green hydrogen will gradually displace gas, yet industrial-scale hydrogen infrastructure remains nascent. Unless coordinated storage, import, and pricing reforms materialize, gas exposure will weigh on Malaysia's power market expansion speed by suppressing investor appetite for flexible thermal assets.

Other drivers and restraints analyzed in the detailed report include:

- Aging Coal-Fleet Retirements Triggering Replacement Build-Outs

- Hyperscale Data-Center Clusters Driving Load Pockets

- Electricity-Tariff Subsidy Reforms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Malaysian power market size for renewables is projected to rise at a 22.89% CAGR, eating into thermal technology's 74.92% Malaysia power market share in Malaysia in 2025. Solar leads the renewable surge, propelled by TNB's 2.5 GW floating-solar roll-out and 2 GW of allocated capacity under Large-Scale Solar Round 5. Hydro remains pivotal in East Malaysia, yet expansion is bound by environmental assessment and community engagement. Coal will decline sharply, with 9.1 GW scheduled to retire by 2030, while hydrogen-ready gas turbines pick up reserve margins and prepare the grid for future fuel transitions. Battery storage adoption becomes a gating factor: adequate storage unlocks higher solar penetration, while shortfalls would keep mid-merit gas plants online longer.

Solar's levelized cost fell below marginal gas generation in 2024, even before storage, encouraging IPPs to stack corporate PPAs on top of utility tenders. Hydro assets in Sarawak supply near-baseload output at low variable cost, positioning the state as a potential exporter pending interconnection. Wind and geothermal remain exploratory, and biomass expansion slows due to rising feedstock prices. The evolving mix will influence dispatch order, emissions intensity, and investment allocation across the Malaysia power market.

The Malaysia Power Market Report is Segmented by Power Source (Thermal, Nuclear, and Renewables) and End-User (Utilities, Commercial and Industrial, and Residential). The Market Sizes and Forecasts are Provided in Terms of Installed Capacity (GW).

List of Companies Covered in this Report:

- Tenaga Nasional Berhad (TNB)

- Sarawak Energy Berhad

- Sabah Electricity Sdn Bhd (SESB)

- Edra Power Holdings

- Malakoff Corporation Berhad

- YTL Power International

- Genting Sanyen Power

- Petronas Power Sdn Bhd

- Cypark Resources Berhad

- Solarvest Holdings Berhad

- ERS Energy Sdn Bhd

- Verdant Solar

- LYS Energy Group

- Pathgreen Energy Sdn Bhd

- Sunway Construction Group Bhd (RE EPC)

- JinkoSolar (Malaysia Module Fab)

- First Solar Malaysia

- KEPCO Engineering & Construction

- Huawei Digital Power Malaysia

- Siemens Energy Malaysia

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Industrial electricity-demand surge

- 4.2.2 Renewable-energy capacity targets (31 % by 2025; 40 % by 2035)

- 4.2.3 Aging coal-fleet retirements triggering replacement build-outs

- 4.2.4 Grid-modernisation & T&D capex push

- 4.2.5 Corporate PPAs enabled by Third-Party Access rules

- 4.2.6 Hyperscale data-centre clusters driving load pockets

- 4.3 Market Restraints

- 4.3.1 Natural-gas supply constraints & price volatility

- 4.3.2 Electricity-tariff subsidy reforms

- 4.3.3 Land & permitting hurdles for utility-scale RE

- 4.3.4 Curtailment risk in East-Malaysia weak grids

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook (Smart grid, hydrogen-ready CCGT, BESS)

- 4.7 Porters Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Power Source

- 5.1.1 Thermal (Coal, Natural Gas, Oil and Diesel)

- 5.1.2 Nuclear

- 5.1.3 Renewables (Solar, Wind, Hydro, Geothermal, Biomass & Waste, Tidal)

- 5.2 By End User

- 5.2.1 Utilities

- 5.2.2 Commercial and Industrial

- 5.2.3 Residential

- 5.3 By T&D Voltage Level (Qualitative Analysis only)

- 5.3.1 High-Voltage Transmission (Above 230 kV)

- 5.3.2 Sub-Transmission (69 to 161 kV)

- 5.3.3 Medium-Voltage Distribution (13.2 to 34.5 kV)

- 5.3.4 Low-Voltage Distribution (Up to 1 kV)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Tenaga Nasional Berhad (TNB)

- 6.4.2 Sarawak Energy Berhad

- 6.4.3 Sabah Electricity Sdn Bhd (SESB)

- 6.4.4 Edra Power Holdings

- 6.4.5 Malakoff Corporation Berhad

- 6.4.6 YTL Power International

- 6.4.7 Genting Sanyen Power

- 6.4.8 Petronas Power Sdn Bhd

- 6.4.9 Cypark Resources Berhad

- 6.4.10 Solarvest Holdings Berhad

- 6.4.11 ERS Energy Sdn Bhd

- 6.4.12 Verdant Solar

- 6.4.13 LYS Energy Group

- 6.4.14 Pathgreen Energy Sdn Bhd

- 6.4.15 Sunway Construction Group Bhd (RE EPC)

- 6.4.16 JinkoSolar (Malaysia Module Fab)

- 6.4.17 First Solar Malaysia

- 6.4.18 KEPCO Engineering & Construction

- 6.4.19 Huawei Digital Power Malaysia

- 6.4.20 Siemens Energy Malaysia

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment