PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1911333

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1911333

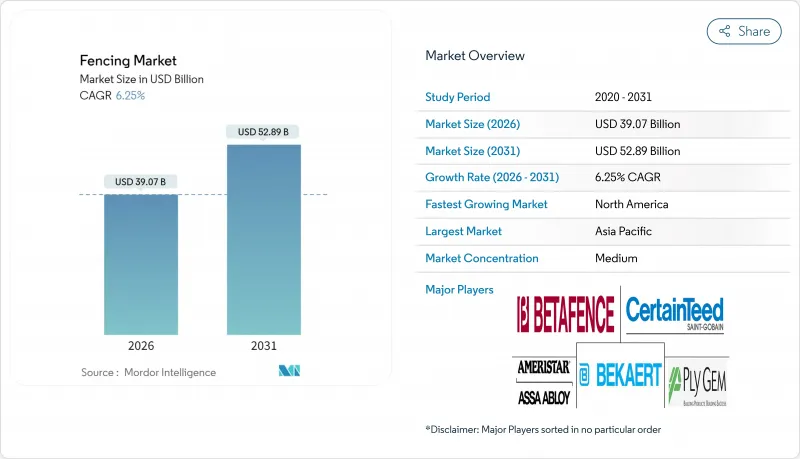

Fencing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

Fencing market size in 2026 is estimated at USD 39.07 billion, growing from 2025 value of USD 36.77 billion with 2031 projections showing USD 52.89 billion, growing at 6.25% CAGR over 2026-2031.

This expansion reflects mandatory hardening of power grids, data centers and borders, the rapid commercialization of smart perimeter hardware, and steady government infrastructure outlays. Metal products continue to dominate large-scale projects because of durability and life-cycle economics, while composite and PVC alternatives are scaling quickly under climate-resilient design mandates. Residential demand remains robust, yet agriculture and renewable-energy installations are emerging as the fastest-moving opportunity set. Professional contractors capture most revenue as IoT-enabled systems raise the technical bar, although DIY kits are expanding in mature housing markets. Regionally, North America retains leadership because of federal spending packages, but Asia-Pacific is set to outpace all other regions on the back of multibillion-dollar border and industrial programs.

Global Fencing Market Trends and Insights

Government Infrastructure Spend Boosting Perimeter Safety Demand

National security priorities are translating into sizeable multiyear budgets devoted to border fortifications and critical-asset protection. India has earmarked INR 32,500 crore (USD 3.89 billion) for fencing and road construction along sensitive borders through 2034, specifying anti-cut and anti-climb steel designs. Updated North American Electric Reliability Corporation guidance requires crash-rated gates at high-impact grid control centers, prompting utilities to overhaul outdated perimeter lines. United States federal building standards now embed Crime Prevention Through Environmental Design principles that specify layered barriers and electronic access control. These mandates are fueling demand for high-specification installations and favoring suppliers with security clearances.

Rising Adoption Of Smart, Sensor-Enabled Fencing Systems

IoT integration is converting passive fences into active threat-detection networks. IEEE studies show multi-sensor smart fences cut false alarms by 60% relative to legacy beam detectors. The U.S. Department of Defense telecommunication standard, recently updated to incorporate secure IoT interfaces, is shaping commercial product roadmaps. Airports adhering to National Safe Skies Alliance best practices are now specifying perimeter solutions that merge video analytics, radar, and credential databases. Department of Homeland Security validation protocols have created uniform performance metrics that accelerate procurement cycles.

Volatile Steel, Timber & PVC Resin Prices

Metal and resin markets remain tight due to energy costs and electrification demand. The World Bank metals index rose 9% in April 2024 and indicates further upside for base metals in 2025. Century Aluminum's curtailed domestic output underscores cost sensitivity in aluminum supply. Boise Cascade's 2024 revenue dip illustrates timber price pass-through challenges during soft housing cycles. Manufacturers are issuing more frequent surcharges, but volatility still squeezes margins and complicates bid pricing.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory Critical-Asset Hardening Regulations

- Climate-Resilient Composite & PVC Materials Gaining Traction

- Competition From Low-cost Unorganised Manufacturers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metal products generated 50.05% of 2025 revenue, anchoring the fencing market through proven strength and lifecycle value. Steel commands defense and utility projects, while aluminum gains residential traction for corrosion resistance. Wood keeps a loyal following where planning codes favor natural aesthetics, though upcoming EU formaldehyde caps create substitution risk. Concrete panels stay niche but indispensable at blast-critical sites.

Composite and PVC systems are scaling at an 8.25% CAGR as specifiers seek low-maintenance alternatives and compliance with lead-free directives. Manufacturers pursuing post-consumer PVC recovery and bio-based stabilizers stand to secure green-procurement premiums. Agrivoltaic pilots highlight how lightweight composites double as solar-panel sub-structures, expanding the fencing market size for multifunctional assets.

Second-generation composites position vendors for long-run advantage by balancing strength-to-weight ratios and recyclability. Restrictive EU rules on lead and novel SVHC listings are accelerating the pivot to zinc-stabilized PVC and recycled HDPE blends. Suppliers with extrusion capacity and closed-loop post-industrial scrap streams can undercut virgin-resin incumbents. Sustainability disclosures are now prerequisites for many public tenders, reinforcing the shift.

The Fencing Market Report is Segmented by Material (Metal, Wood, Plastic & Composite, Concrete, Other Materials), by End-User (Residential, Agricultural, Military & Defense, Government, Mining, and More), by Installation Type (Professional Contractor, Others - Fabricators, DIY / Modular Kits), and by Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 35.10% of 2025 global sales, propelled by federal grants for road, grid, and veterans facility upgrades. Updated NERC rules obligate utilities to fortify substation perimeters, while Buy-America provisions steer spend toward domestic roll-formers and fabricators. An expanding residential remodeling base supports the region's near-term outlook.

Asia-Pacific, though smaller today, is set to post the fastest 7.05% CAGR through 2031. India has budgeted more than USD 400 million for border fencing, including anti-climb steel grating along high-risk corridors. China's infrastructure stimulus and urban renewal projects cushion fencing demand despite property-sector headwinds. Japan and South Korea champion smart-sensor adoption, while Australia's mining sector continues to procure temporary barriers for remote camps.

Europe's market is framed by stringent eco-design laws and circular-economy targets. Lead-free PVC deadlines and the 2026 EU formaldehyde threshold spur material substitution, opening a competitiveness gap for innovators. Renewables build-out, particularly onshore wind repowering, sustains utility demand. Eastern Europe benefits from EU cohesion fund grants channelled into transport corridors that require long miles of acoustic and security fencing.

- CertainTeed

- Bekaert

- Betafence

- Ameristar Perimeter Security

- Ply Gem

- Long Fence

- Gregory Industries

- A-1 Fence Products

- Specrail

- Jerith

- Trex Company

- Barrette Outdoor Living

- Master Halco

- ActiveYards

- Fortress Building Products

- Allied Tube & Conduit

- Eastern Wholesale Fence

- Merchants Metals

- ITOCHU Corporation (Sakura)

- Gentek Building Products

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government infrastructure spend boosting perimeter safety demand

- 4.2.2 Rising adoption of smart, sensor-enabled fencing systems

- 4.2.3 Climate-resilient composite & PVC materials gaining traction

- 4.2.4 Surging DIY home-improvement culture in mature economies

- 4.2.5 Mandatory critical-asset hardening (utilities, data-centres) regulations

- 4.2.6 Demand for perimeter security in agrivoltaics & vertical farming sites

- 4.3 Market Restraints

- 4.3.1 Volatile steel, timber & PVC resin prices

- 4.3.2 Competition from low-cost unorganised manufacturers

- 4.3.3 Stricter environmental rules on wood preservatives & PVC additives

- 4.3.4 Rising substitute spend on electronic surveillance in lieu of physical barriers

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Materials Analysis

- 4.9 Impact of Geopolitics On Fencing Market

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Material

- 5.1.1 Metal

- 5.1.1.1 Steel

- 5.1.1.2 Aluminium

- 5.1.2 Wood

- 5.1.3 Plastic & Composite

- 5.1.4 Concrete

- 5.1.5 Other Materials

- 5.1.1 Metal

- 5.2 By End-User

- 5.2.1 Residential

- 5.2.2 Agricultural

- 5.2.3 Military & Defense

- 5.2.4 Government

- 5.2.5 Mining

- 5.2.6 Petroleum & Chemicals

- 5.2.7 Energy & Power

- 5.2.8 Other End-Users

- 5.3 By Installation Type

- 5.3.1 Professional Contractor

- 5.3.2 Others - Fabricators, DIY / Modular Kits

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Chile

- 5.4.2.4 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Netherlands

- 5.4.3.7 Rest of Europe

- 5.4.4 Middle East and Africa

- 5.4.4.1 Saudi Arabia

- 5.4.4.2 United Arab Emirates

- 5.4.4.3 South Africa

- 5.4.4.4 Nigeria

- 5.4.4.5 Rest of Middle East and Africa

- 5.4.5 Asia-Pacific

- 5.4.5.1 China

- 5.4.5.2 India

- 5.4.5.3 Japan

- 5.4.5.4 South Korea

- 5.4.5.5 Australia

- 5.4.5.6 Indonesia

- 5.4.5.7 Rest of Asia-Pacific

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, Recent Developments)

- 6.4.1 CertainTeed

- 6.4.2 Bekaert

- 6.4.3 Betafence

- 6.4.4 Ameristar Perimeter Security

- 6.4.5 Ply Gem

- 6.4.6 Long Fence

- 6.4.7 Gregory Industries

- 6.4.8 A-1 Fence Products

- 6.4.9 Specrail

- 6.4.10 Jerith

- 6.4.11 Trex Company

- 6.4.12 Barrette Outdoor Living

- 6.4.13 Master Halco

- 6.4.14 ActiveYards

- 6.4.15 Fortress Building Products

- 6.4.16 Allied Tube & Conduit

- 6.4.17 Eastern Wholesale Fence

- 6.4.18 Merchants Metals

- 6.4.19 ITOCHU Corporation (Sakura)

- 6.4.20 Gentek Building Products

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

8 Appendix

- 8.1 Macroeconomic Indicators

- 8.2 Key Production, Consumption, Export & Import Stats