PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1934622

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1934622

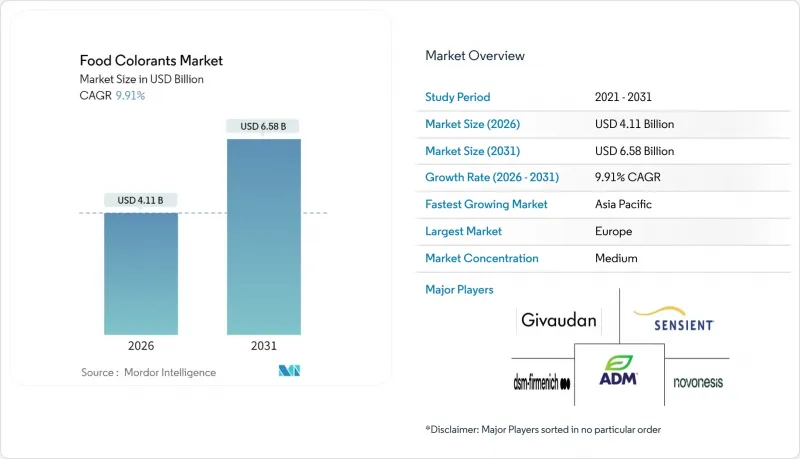

Food Colorants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

food colorants market size in 2026 is estimated at USD 4.11 billion, growing from 2025 value of USD 3.74 billion with 2031 projections showing USD 6.58 billion, growing at 9.91% CAGR over 2026-2031.

The market growth is driven by increasing restrictions on synthetic dyes, rising demand for clean-label product reformulations, and new regulatory approvals that expand the availability of plant-based colorants. Europe currently leads the market due to strict regulations on food additives, while the Asia-Pacific region shows significant growth potential, particularly in China and India, where packaged food industries are increasingly adopting natural colorants at a large scale. Advancements in precision fermentation technology and improved extraction methods are reducing the historical cost and performance differences between natural and synthetic colors, enabling manufacturers to compete on quality rather than price alone. The market is experiencing increased competitive activity, with large companies securing upstream raw material supplies while new entrants focus on specialized color development and fermentation-derived ingredients.

Global Food Colorants Market Trends and Insights

Growth in processed foods and beverage industry

The growth in processed food manufacturing drives consistent demand for colorants across various product categories, particularly in emerging markets where urbanization increases convenience food consumption. The expansion of the Asia-Pacific's processed food sector directly influences colorant usage, as manufacturers aim to enhance product appearance while catering to regional taste preferences. According to the Centers for Disease Control and Prevention (CDC) National Health and Nutrition Examination Survey released in August 2025, ultra-processed foods constitute 55.0% of total daily calories consumed by Americans aged 1 and older, with youth aged 1-18 consuming 61.9%. This significant consumption of processed and packaged foods maintains a steady demand for food additives, especially colorants, which enhance visual appeal and product differentiation. According to Ayana Bio, 67.0% of consumers in 2023/24 demonstrated willingness to pay premium prices for ultra-processed foods that offer convenience and quality. Natural colorants, including spirulina, beetroot, turmeric, and carotenoids, have increased in popularity as manufacturers respond to clean-label preferences while providing stable coloring solutions for confectionery, beverages, snacks, and ready-to-eat meals. The FDA's 2024 approval of spirulina extract for beverage applications demonstrates regulatory adaptation to support natural colorant use in processed foods. This trend shows medium-term impact as food processing infrastructure develops gradually, supported by consistent demographic and economic growth across developing regions.

Natural colorants take center stage in cosmetics

The global natural colorants market is experiencing robust growth, driven by increasing demand for ethical and vegan beauty products. Consumer preferences have fundamentally shifted toward cruelty-free, vegan, and ethically sourced cosmetics. This change extends beyond traditional clean-label or organic preferences, emphasizing ethical consumption, sustainability, and transparency in ingredient sourcing. Companies are actively transitioning from synthetic and animal-based pigments to plant-based and mineral-derived colorants in response to consumer awareness about product formulations. Consumer focus on ingredient transparency has intensified, particularly regarding vegan and cruelty-free products. A June 2024 Naris Cosmetics survey found that 46% of Japanese consumers thoroughly review ingredient labels before making purchasing decisions. The cosmetics market is experiencing a substantial transformation through the rapid expansion of vegan beauty products, which eliminate all animal-derived ingredients, including carmine (E120) from cochineal insects. This development has accelerated the adoption of alternative pigments sourced from plants, fruits, and algae. As ethical beauty transitions from a niche segment to mainstream, natural colorants are becoming essential components for future cosmetic product development and innovation.

Stringent regulations on synthetic colorants

Growing consumer awareness of health and environmental issues has led regulatory bodies to tighten controls on synthetic dyes and colorants due to their health risks and environmental impact. These regulations are driving manufacturers in the food, beverage, cosmetic, and pharmaceutical industries to adopt natural colorants. Natural alternatives offer safety benefits and environmental advantages while meeting consumer demands for clean-label products. This shift in regulatory landscape and consumer preferences continues to create substantial demand for natural and sustainable colorants across various sectors. The U.S. Food and Drug Administration (FDA) requires batch certification for artificial colorants to verify their identity and specifications. However, colorants derived from natural sources, including vegetables, minerals, and animals, are exempt from this certification requirement. These certification-exempt natural colorants include annatto extract (yellow), dehydrated beets (bluish-red to brown), caramel (yellow to tan), beta-carotene (yellow to orange), and grape skin extract (red or purple). This regulatory leniency has significantly strengthened the market for natural food colorants in the region. In October 2023, consumer advocacy groups intensified pressure on the FDA to ban synthetic red No. 3 food coloring, following California's legislative action that prohibited the dye's use due to its established connection with hyperactivity reactions in children.

Other drivers and restraints analyzed in the detailed report include:

- Rising demand for organic and clean-label ingredients

- Regulatory tailwinds expanding natural color approvals

- Stability and performance limitations for natural colorants

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Natural color commands 60.36% market share in 2025, reflecting consumer preference shifts and regulatory momentum toward plant-based alternatives, while synthetic color segments paradoxically exhibit the fastest growth at 10.33% CAGR through 2031 as manufacturers stockpile supplies before regulatory phase-outs. In the natural color segment, spirulina has shown significant growth following FDA approvals for use in beverage applications, while carotenoids continue to benefit from established supply chains and reliable stability profiles. Anthocyanins face formulation challenges in high-pH applications but maintain strong demand in dairy and confectionery products. Curcumin benefits from dual functionality as both a colorant and a functional ingredient, while carmine faces ethical concerns from vegan consumers despite superior performance characteristics.

Food manufacturers are stockpiling supplies of azo dyes and brilliant blue FCF ahead of impending regulatory restrictions, driving an acceleration in the synthetic segment's growth. This stockpiling behavior, aimed at mitigating potential supply chain disruptions and ensuring production continuity, creates temporary market distortions that obscure a more profound, long-term shift towards natural alternatives. Meanwhile, the FDA's expedited approval process for natural colors offers a competitive edge to companies boasting strong regulatory expertise, efficient compliance mechanisms, and a diverse product lineup, enabling them to adapt swiftly to evolving market demands.

The Food Colorants Market Report Segments the Industry by Product Type (Natural Color, Synthetic Color), Color (Blue, Green, Red, Yellow, Purple, and More), Application (Food and Beverages, Personal Care and Cosmetics, Pharmaceuticals, Dietary Supplements, Other Applications), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe holds a 34.10% market share in 2025, driven by established natural colorant regulations and robust supply chains for plant-based alternatives, maintaining its position as the global market leader. Germany and France demonstrate leadership in regulatory compliance and premium positioning, while the United Kingdom maintains strong demand despite Brexit-related supply chain adjustments. Italy emphasizes traditional food authenticity in line with natural colorant adoption, and Spain leverages its agricultural production capabilities for colorant extraction, further strengthening the regional market dynamics.

Asia-Pacific demonstrates the highest growth rate at 11.02% CAGR through 2031, supported by China's new standards for plant-based coloring foods introduced in May 2025 and India's comprehensive public awareness campaign on synthetic-dye health effects. The region's substantial processed-food industry requires extensive sourcing of curcumin, spirulina, and vegetable-juice concentrates to meet growing demand. Japanese confectionery manufacturers are transitioning from carmine to purple-sweet-potato extracts to accommodate vegan preferences, while Southeast Asian fruit exporters are incorporating color-extraction facilities to reduce waste and enhance export value in the global market.

North America shows significant market development as the FDA's timeline to remove petroleum-based dyes drives major food brands to secure alternatives, creating substantial market opportunities. U.S. beverage manufacturers initiated production trials of Galdieria extract blue shortly after approval, demonstrating the immediate impact of regulatory changes on market adoption. Under the Canada-United States-Mexico Agreement, Canada is expected to align with U.S. colorant restrictions, facilitating cross-border certification processes and enhancing regional market integration.

- Novonesis (Chr. Hansen Holding A/S)

- Sensient Technologies Corp.

- Archer-Daniels-Midland (ADM)

- DSM-Firmenich

- Dohler Group

- GNT Group (EXBERRY)

- BASF SE

- Lycored Ltd.

- Givaudan (Naturex)

- Fiorio Colori S.p.A.

- Kalsec Inc.

- Kerry Group

- Symrise AG

- Kemin Industries

- San-E Color Co.

- Sethness-Roquette

- Sun Chemical Corp.

- DDW China (Shanghai)

- Diana Food (Symrise)

- WILD Flavors & Specialty Ingredients

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and market definition

- 1.2 Scope of the study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in processed foods and beverage industry

- 4.2.2 Natural colorants take center stage in cosmetics

- 4.2.3 Rising demand for organic and clean-label ingredients

- 4.2.4 Regulatory tailwinds expanding natural color approvals

- 4.2.5 Advanced extraction methods improving yield, purity, and sustainability

- 4.2.6 Rising Adoption of spirulina-derived blue shades

- 4.3 Market Restraints

- 4.3.1 Stringent regulations on synthetic colorants

- 4.3.2 Stability and performance limitations for natural colorants

- 4.3.3 High cost of natural pigments

- 4.3.4 Climate-driven crop supply volatility

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porters Five Force Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 Product Type

- 5.1.1 Natural Color

- 5.1.1.1 Anthocyanins

- 5.1.1.2 Carotenoids

- 5.1.1.3 Curcumin

- 5.1.1.4 Carmine

- 5.1.1.5 Spirulina

- 5.1.1.6 Other Types

- 5.1.2 Synthetic Color

- 5.1.2.1 Azo Dyes (Tartrazine, Sunset Yellow, etc.)

- 5.1.2.2 Brilliant Blue FCF

- 5.1.2.3 Others

- 5.1.1 Natural Color

- 5.2 By Color

- 5.2.1 Blue

- 5.2.2 Green

- 5.2.3 Red

- 5.2.4 Yellow

- 5.2.5 Purple

- 5.2.6 Orange

- 5.2.7 Pink

- 5.2.8 Others

- 5.3 Application

- 5.3.1 Food and Beverages

- 5.3.1.1 Bakery and Confectionery

- 5.3.1.2 Dairy Products

- 5.3.1.3 Snacks and Cereals

- 5.3.1.4 Beverages

- 5.3.1.5 Others

- 5.3.2 Personal Care and Cosmetics

- 5.3.3 Pharmaceuticals

- 5.3.4 Dietary Supplements

- 5.3.5 Other Applications

- 5.3.1 Food and Beverages

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Russia

- 5.4.2.6 Spain

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Australia

- 5.4.3.4 Japan

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Active Companies

- 6.2 Market Positioning Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.3.1 Novonesis (Chr. Hansen Holding A/S)

- 6.3.2 Sensient Technologies Corp.

- 6.3.3 Archer-Daniels-Midland (ADM)

- 6.3.4 DSM-Firmenich

- 6.3.5 Dohler Group

- 6.3.6 GNT Group (EXBERRY)

- 6.3.7 BASF SE

- 6.3.8 Lycored Ltd.

- 6.3.9 Givaudan (Naturex)

- 6.3.10 Fiorio Colori S.p.A.

- 6.3.11 Kalsec Inc.

- 6.3.12 Kerry Group

- 6.3.13 Symrise AG

- 6.3.14 Kemin Industries

- 6.3.15 San-E Color Co.

- 6.3.16 Sethness-Roquette

- 6.3.17 Sun Chemical Corp.

- 6.3.18 DDW China (Shanghai)

- 6.3.19 Diana Food (Symrise)

- 6.3.20 WILD Flavors & Specialty Ingredients

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK