PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1937439

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1937439

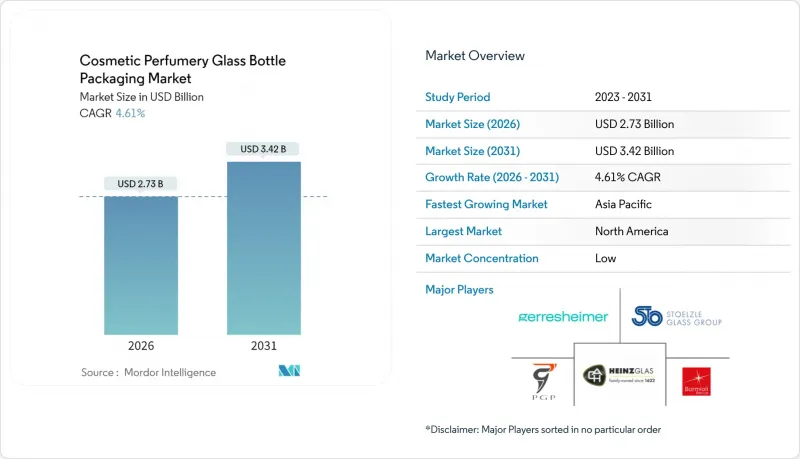

Cosmetic Perfumery Glass Bottle Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The cosmetic perfumery glass bottle packaging market was valued at USD 2.61 billion in 2025 and estimated to grow from USD 2.73 billion in 2026 to reach USD 3.42 billion by 2031, at a CAGR of 4.61% during the forecast period (2026-2031).

This moderate yet resilient growth trajectory reflects the sector's ability to navigate supply-chain volatility while capitalizing on premiumization trends that favor glass over alternative materials. The market's expansion occurs against a backdrop of transformative regulatory shifts, particularly EU Regulation 2025/40, which mandates that all packaging be recyclable by 2030. This regulation positions glass as a strategic advantage, given its infinite recyclability without degradation in quality. Macro forces reshaping the industry center on sustainability mandates intersecting with luxury positioning strategies. The premiumization wave in beauty and fragrance products drives demand for aesthetically superior packaging that conveys brand heritage and product integrity. Simultaneously, e-commerce expansion creates dual pressures: brands require visually compelling packaging for digital marketing while needing impact-resistant solutions to minimize breakage-related returns.

Global Cosmetic Perfumery Glass Bottle Packaging Market Trends and Insights

Premiumisation of Beauty and Fragrance Products

Premium beauty and fragrance brands increasingly position glass packaging as a tangible expression of product quality and brand heritage, driving specification shifts away from plastic alternatives. This trend accelerates as consumer willingness to pay premium prices for luxury cosmetics increases, particularly in emerging markets where glass packaging is seen as a symbol of authenticity and prestige. The premiumization effect creates a virtuous cycle: higher product prices justify the costs of glass packaging, while glass packaging reinforces premium positioning and enables further price increases. Luxury fragrance launches consistently specify custom glass flacons with unique shapes, colors, and decorative elements that plastic cannot replicate, cementing glass as the material of choice for high-end positioning. Digital marketing amplifies this trend, as glass packaging photographs better for social media and e-commerce platforms, creating additional value for brands that invest in visual differentiation.

Sustainability Push for Infinitely-Recyclable Glass

Regulatory frameworks and corporate sustainability commitments converge to favor the infinite recyclability advantage of glass packaging over plastic alternatives. The EU's Packaging and Packaging Waste Regulation mandates that all packaging be recyclable by 2030, with glass achieving 74% recycling rates compared to significantly lower plastic recycling performance. Glass recycling creates a closed-loop system where post-consumer cullet can constitute up to 82% of new bottle content without quality degradation, as demonstrated by O-I's carbon-neutral Estampe bottle. Corporate sustainability strategies are increasingly recognizing the contribution of glass packaging to Scope 3 emissions reduction, with brands like SGD Pharma launching bottles with 20% post-consumer recycled content, specifically designed for cosmetics applications. The sustainability narrative resonates particularly strongly with Gen Z consumers, who prioritize environmental credentials and view glass as a superior alternative to plastic.

Plastic Packaging Cost and Weight Advantage

Plastic packaging maintains significant cost and logistics advantages that hinder the adoption of glass, particularly in mass-market cosmetic segments where price sensitivity limits the selection of premium materials. Plastic containers typically cost 40-60% less than equivalent glass packaging, while weighing substantially less, which reduces shipping costs and the carbon footprint associated with high-volume distribution. Advanced plastic formulations are increasingly replicating glass aesthetics through clear polymers and surface treatments, enabling premium positioning without the costs associated with glass. The weight differential becomes particularly pronounced for large-format products and multi-product sets, where glass packaging can double shipping costs compared to plastic alternatives. E-commerce growth amplifies these concerns as brands optimize packaging for cost-effective fulfillment while minimizing damage-related returns and customer dissatisfaction.

Other drivers and restraints analyzed in the detailed report include:

- E-commerce Demand for Aesthetic, Impact-Resistant Packs

- Laser-Enabled Personalisation and Anti-Counterfeit Engraving

- Volatile Energy and Soda-Ash Input Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Perfumes accounted for a 46.28% portion of the cosmetic perfumery glass bottle packaging market in 2025, underscoring how fragrance houses rely on inert glass containers to preserve complex scent profiles. This dominant foothold equates to the single-largest slice of the cosmetic perfumery glass bottle packaging market share. The segment benefits from a well-established association between bespoke flacons and luxury positioning, enabling brands to maintain premium price points even during cost-inflation cycles. Strong marketing support from designer labels sustains steady reorder volumes, keeping the cosmetic perfumery glass bottle packaging market resilient to demand swings in adjacent beauty categories.

Nail care, although still comparatively smaller, is expanding at a 6.05% CAGR through 2031, the fastest growth among all tracked products, as consumers trade up to salon-quality lacquers packaged in custom glass vials. Growing influencer interest in nail art has expanded the addressable market, and formulators prefer glass to minimize solvent evaporation. Skin-care and hair-care lines report mid-single-digit advances as glass dropper bottles and treatment jars signal efficacy for retinol serums, ampoules, and concentrated masks. Although make-up remains selective in its use of glass, prestige brands tap artisanal flacons for limited-edition face mists and cushion-compact refills, keeping the cosmetic perfumery glass bottle packaging market diversified across multiple beauty rituals.

The Cosmetic Perfumery Glass Bottle Packaging Market Report is Segmented by Product Type (Perfumes, Skin Care, Nail Care, Hair Care, and More), Capacity (0-50 Ml, 50-150 Ml, and >150 Ml), Color (Flint, Amber, Frosted, Special-Coloured, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 37.10% of the worldwide cosmetic perfumery glass bottle packaging market revenue in 2025, driven by its established designer-fragrance ecosystem, subscription beauty boxes, and robust take-back programs that reward consumers for returning empty primary containers. Prestige houses continue to champion artisanal glass flacons as brand icons, while direct-to-consumer startups integrate refill pods to cut waste. Canada's Extended Producer Responsibility regime subsidizes cullet collection, which feeds regional furnaces and supports a closed-loop stream that bolsters the cosmetic perfumery glass bottle packaging market size.

The Asia-Pacific region is the sprinting growth engine, with a 5.36% CAGR to 2031, driven by TikTok-driven beauty trends and rising disposable incomes in China, India, and Indonesia. Mainland China's fragrance awakening triggers record custom-flacon briefs, and Indian consumers increasingly associate heavy-walled glass with authenticity, steering incremental demand toward the cosmetic perfumery glass bottle packaging market. South Korea's K-Beauty exporters innovate dual-chamber glass ampoules that keep active powders separate until activation, demonstrating how regional R&D leapfrogs legacy formats.

Europe remains anchored by regulatory muscle EU Regulation 2025/40 and storied perfumery clusters in Grasse, Idar-Oberstein, and Parma. Producers harvest high cullet ratios from mature collection schemes, allowing cosmetic perfumery glass bottle packaging market participants to hit brand carbon targets without price-crippling virgin-batch surcharges. Eastern Europe supplies value-centric flint bottles, leveraging lower energy tariffs, while Western converters focus on decoration excellence and luxury finishing.

- Verescence France SASU

- Gerresheimer AG

- Pochet SAS

- HEINZ-GLAS GmbH & Co. KGaA

- Bormioli Luigi S.p.A.

- Vitro, S.A.B. de C.V.

- PGP Glass Private Limited

- Stoelzle Glass Group

- Zignago Vetro S.p.A.

- Berlin Packaging LLC

- Saver Glass SAS

- Pragati Glass Pvt Ltd

- Baralan International S.p.A.

- Lumson S.p.A.

- vetroelite packaging s.r.l

- Feemio Group Co., Ltd.

- Brandsamor Commerce LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Premiumisation of beauty and fragrance products

- 4.2.2 Sustainability push for infinitely-recyclable glass

- 4.2.3 E-commerce demand for aesthetic, impact-resistant packs

- 4.2.4 Laser-enabled personalisation and anti-counterfeit engraving

- 4.2.5 EU-2025/40 regulation favouring recyclable mono-material packs

- 4.2.6 Electrified and lightweight furnaces cutting cost and CO2

- 4.3 Market Restraints

- 4.3.1 Plastic packaging cost and weight advantage

- 4.3.2 Volatile energy and soda-ash input prices

- 4.3.3 EU packaging-minimisation rules curbing heavy, ornate flacons

- 4.3.4 High e-commerce breakage / return rates for fragile glass

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Perfumes

- 5.1.2 Skin Care

- 5.1.3 Nail Care

- 5.1.4 Hair Care

- 5.1.5 Other Product Type

- 5.2 By Capacity

- 5.2.1 0-50 ml

- 5.2.2 50-150 ml

- 5.2.3 >150 ml

- 5.3 By Color

- 5.3.1 Flint

- 5.3.2 Amber

- 5.3.3 Frosted

- 5.3.4 Special-coloured

- 5.3.5 Other Color

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Chile

- 5.4.2.4 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 South Korea

- 5.4.4.5 Australia

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Turkey

- 5.4.5.1.4 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Nigeria

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Verescence France SASU

- 6.4.2 Gerresheimer AG

- 6.4.3 Pochet SAS

- 6.4.4 HEINZ-GLAS GmbH & Co. KGaA

- 6.4.5 Bormioli Luigi S.p.A.

- 6.4.6 Vitro, S.A.B. de C.V.

- 6.4.7 PGP Glass Private Limited

- 6.4.8 Stoelzle Glass Group

- 6.4.9 Zignago Vetro S.p.A.

- 6.4.10 Berlin Packaging LLC

- 6.4.11 Saver Glass SAS

- 6.4.12 Pragati Glass Pvt Ltd

- 6.4.13 Baralan International S.p.A.

- 6.4.14 Lumson S.p.A.

- 6.4.15 vetroelite packaging s.r.l

- 6.4.16 Feemio Group Co., Ltd.

- 6.4.17 Brandsamor Commerce LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment