PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940711

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940711

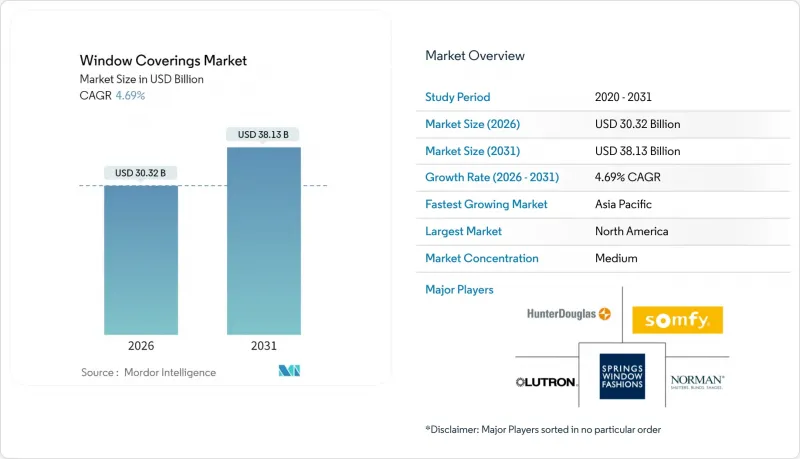

Window Coverings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The window coverings market was valued at USD 28.96 billion in 2025 and estimated to grow from USD 30.32 billion in 2026 to reach USD 38.13 billion by 2031, at a CAGR of 4.69% during the forecast period (2026-2031).

Increasing demand for energy-efficient homes, smart-home ecosystems, and aesthetic upgrades drives this expansion, transforming a once utilitarian category into a technology-enabled, performance-oriented industry. Smart automation, tax incentives for high-efficiency products, and stringent green-building regulations now outweigh purely decorative considerations. At the same time, raw-material volatility and emerging electrochromic glass alternatives inject competitive tension, compelling producers to innovate on both cost and sustainability fronts.

Global Window Coverings Market Trends and Insights

Surging Residential Renovation Expenditure

US homeowners are expected to spend USD 509 billion on improvement projects in 2025, up 1.2% from 2024. Rising home equity and favorable financing terms push discretionary spending toward energy-saving upgrades such as insulated cellular shades. Renovation projects increasingly bundle smart-home capabilities, so premium window solutions incorporating voice control and automation gain traction. Manufacturers benefit from bulk orders for entire home retrofits, improving economies of scale. This spending cycle also fosters do-it-yourself demand, prompting suppliers to release simplified installation kits.

Rapid Adoption of Motorized/Smart Shades

Cordless safety rules and voice-assistant popularity have moved automation from niche to mainstream, propelling the smart segment to a 12.4% CAGR. Sensor-equipped motors pre-empt interior heat gain by lowering blinds when sunlight intensity crosses thresholds, cutting HVAC loads. Open-protocol radios such as Zigbee 3.0 assure compatibility across platforms, reducing buyer hesitation. Battery-powered engines now last 18-24 months per charge, broadening retrofit appeal. Commercial buildings adopt centralized shading that aligns with BMS software, enhancing comfort scores used in WELL and LEED certifications.

Volatility of Raw-Material Prices

PVC resin rose by 1 cent per pound in March 2025 amid seasonal construction demand. China's tariff hike to 5.5% on PVC imports further inflates input costs. Aluminium spot prices also climb, squeezing blind manufacturers. Producers hedge with recycled feedstocks and bio-attributed PVC that cuts CO2 by 58%, but initial premiums weigh on margins. Volatile costs complicate long-term contracts with commercial builders, increasing project risk.

Other drivers and restraints analyzed in the detailed report include:

- Energy-Efficiency Mandates and Green-Building Codes

- Commercial Daylight Management for Employee Well-Being

- Environmental Pushback on Single-Use Plastics and Corded Blinds

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Blinds generated 34.68% of the window coverings market size in 2025 thanks to versatility and price competitiveness. Aluminium venetians stay popular for commercial retrofits, while vertical formats serve large patio doors. Motorized shades, though smaller in value, are advancing at 7.47% CAGR as smart-home hubs become household staples. Roller shades dominate office fit-outs because they integrate neatly with occupancy sensors. Shutters retain niche appeal in high-wind regions for storm protection. Curtains and drapes defend relevance in hospitality where textile layers enhance acoustics. Between-glass blind systems, sealed within IGUs, illustrate product innovation that meets stringent energy codes in markets like China.

A second wave of demand arises from retrofit packages that bundle motorized rollers with voice-assistant skills. Channel partners report that adding automation can lift average ticket prices by 18-22%. Despite growth, saturation in mature suburban neighborhoods tempers long-term volume. Blinds makers therefore emphasize recyclable alloys and low-VOC coatings to stay aligned with green-building specs. The cleaners-friendly nature of aluminium continues to attract healthcare projects requiring frequent sanitation. Meanwhile, luxury installers upsell dual-shade combos-one blackout, one sheer-to achieve both privacy and daylight management in premium apartments.

Synthetic yarns account for 39.85% of market revenue due to fade resistance and wide color gamut. Polyester remains the workhorse across roller, roman, and panel tracks. Nevertheless, composite fabrics-blends of recycled PET, glass fiber, and bio-PU films-are gaining at 8.05% CAGR, meeting LEED material credits. Natural fibers claim mindshare among wellness-oriented consumers seeking low-chemical interiors, though humidity sensitivity limits their share in tropical zones.

Aluminium and steel command institutional jobs requiring fire-rating compliance and vandal resistance. Faux-wood slats satisfy moisture-prone bathrooms, displacing real basswood. In parallel, bio-attributed PVC enters mass production, promising identical performance with lower scope-3 footprints. Raw-material unpredictability encourages multi-material hybrid designs that optimize cost while lowering weight, easing motor load requirements. Suppliers showcase clear EPDs (Environmental Product Declarations) to differentiate in government tenders.

The Window Coverings Market Report is Segmented by Product Type (Blinds, Shades, Shutters, and More), Material (Fabric, Wood and Faux Wood, Metal, Plastic and Vinyl, Composite and Others), Technology (Manual, Motorized, Smart/IoT-enabled), End-User (Residential, Commercial, Hospitality, Healthcare and Institutional, and More), Distribution Channel, and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 32.35% of global revenue in 2025 as federal incentives and state rebates spurred adoption of insulated honeycomb shades. The window coverings market size across the region is projected to grow steadily thanks to stable disposable income and robust renovation outlays. Smart-home penetration surpasses 45% of households, converting curiosity into sales of voice-controlled rollers. Canada amplifies demand in cold-weather provinces where thermal performance is paramount. Nonetheless, material cost swings linked to tariffs remain a short-term headwind.

Europe maintains mature but innovation-driven demand anchored by stringent EPBD revisions targeting near-zero-energy buildings. Germany mandates dynamic shading in public tenders, while France links property tax discounts to facade energy ratings. Circular-economy directives accelerate uptake of recyclable aluminium and cradle-to-cradle fabrics. Brexit-related customs checks initially slowed UK imports, but domestic assembly hubs now buffer lead-time risks. Southern markets such as Spain and Italy favor solar-reflective screens that beat summer heat without ADP system strain.

Asia-Pacific will register a 6.22% CAGR, making it the fastest-growing territory through 2031. China enforces GB 50189-2005 thermal benchmarks that elevate demand for low-U-value shade assemblies. The 14th Five-Year Plan's urban housing push raises volume possibilities, while PVC tariffs reshape supply chains toward regional resin sources. India's multi-tower residential boom features standardized curtain-wall glazing that benefits from factory-calibrated roller kits. Japan and South Korea embrace retrofittable motors in compact apartments, leveraging high broadband penetration for IoT control. Meanwhile, ASEAN nations prioritize affordable blinds meeting basic glare control yet gradually adopt cellular fabrics in premium condos.

- Hunter Douglas N.V.

- Springs Window Fashions LLC

- Norman Window Fashions Ltd.

- Somfy S.A.

- Lutron Electronics Co., Inc.

- MechoShade Systems LLC

- Griesser AG

- Kvadrat Shade B.V.

- Decora Blind Systems Ltd.

- Insolroll Window Shading Systems

- Hillarys Blinds Ltd.

- Bombay Dyeing and Manufacturing Co. Ltd.

- Roma KG

- 3 Day Blinds LLC

- Guangzhou JADY Window Coverings Technology Co., Ltd.

- Alta Window Fashions Inc.

- Legrand S.A. (BTicino and Netatmo Shades)

- Hunter Douglas India Pvt. Ltd.

- Western Sydney Shutters Pty Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging residential renovation expenditure

- 4.2.2 Rapid adoption of motorized/smart shades

- 4.2.3 Energy-efficiency mandates and green-building codes

- 4.2.4 Commercial daylight-management for employee well-being

- 4.2.5 Insurance rebates for glare and heat-gain control (under-reported)

- 4.2.6 Growth of antimicrobial fabrics in healthcare blinds (under-reported)

- 4.3 Market Restraints

- 4.3.1 Volatility of raw-material (PVC, aluminium) prices

- 4.3.2 Environmental pushback on single-use plastics and corded blinds

- 4.3.3 Rising competition from electro-chromic smart-glass

- 4.3.4 IoT-related cybersecurity and privacy concerns (under-reported)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Investment Analysis

- 4.9 Key Performance Indicators (KPIs)

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Blinds (Venetian, Vertical, Roller, Others)

- 5.1.2 Shades (Roman, Pleated, Roller)

- 5.1.3 Shutters

- 5.1.4 Curtains and Drapes

- 5.1.5 Other Types

- 5.2 By Material

- 5.2.1 Fabric (Natural, Synthetic)

- 5.2.2 Wood and Faux Wood

- 5.2.3 Metal (Aluminium, Steel)

- 5.2.4 Plastic and Vinyl

- 5.2.5 Composite and Others

- 5.3 By Technology

- 5.3.1 Manual

- 5.3.2 Motorized (Battery, Hard-wired)

- 5.3.3 Smart/IoT-enabled

- 5.4 By End-user

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.4.3 Hospitality

- 5.4.4 Healthcare and Institutional

- 5.4.5 Other End-users (Marine, Automotive, etc.)

- 5.5 By Distribution Channel

- 5.5.1 Offline (Department, DIY, Specialist, Grocery)

- 5.5.2 Online

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 Middle East

- 5.6.4.1 Israel

- 5.6.4.2 Saudi Arabia

- 5.6.4.3 United Arab Emirates

- 5.6.4.4 Turkey

- 5.6.4.5 Rest of Middle East

- 5.6.5 Africa

- 5.6.5.1 South Africa

- 5.6.5.2 Egypt

- 5.6.5.3 Rest of Africa

- 5.6.6 South America

- 5.6.6.1 Brazil

- 5.6.6.2 Argentina

- 5.6.6.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Hunter Douglas N.V.

- 6.4.2 Springs Window Fashions LLC

- 6.4.3 Norman Window Fashions Ltd.

- 6.4.4 Somfy S.A.

- 6.4.5 Lutron Electronics Co., Inc.

- 6.4.6 MechoShade Systems LLC

- 6.4.7 Griesser AG

- 6.4.8 Kvadrat Shade B.V.

- 6.4.9 Decora Blind Systems Ltd.

- 6.4.10 Insolroll Window Shading Systems

- 6.4.11 Hillarys Blinds Ltd.

- 6.4.12 Bombay Dyeing and Manufacturing Co. Ltd.

- 6.4.13 Roma KG

- 6.4.14 3 Day Blinds LLC

- 6.4.15 Guangzhou JADY Window Coverings Technology Co., Ltd.

- 6.4.16 Alta Window Fashions Inc.

- 6.4.17 Legrand S.A. (BTicino and Netatmo Shades)

- 6.4.18 Hunter Douglas India Pvt. Ltd.

- 6.4.19 Western Sydney Shutters Pty Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment