PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940720

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940720

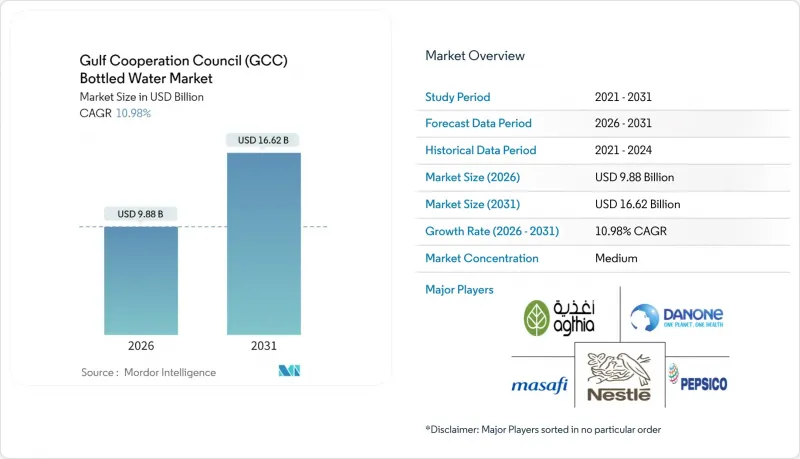

Gulf Cooperation Council (GCC) Bottled Water - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

GCC bottled water market size in 2026 is estimated at USD 9.88 billion, growing from 2025 value of USD 8.90 billion with 2031 projections showing USD 16.62 billion, growing at 10.98% CAGR over 2026-2031.

The region's status as the most water-stressed globally, its 90% dependence on desalination for drinking water, and frequent extreme temperatures are key factors driving this demand. Growing health and wellness awareness is prompting consumers to opt for bottled water over sugary and carbonated beverages. Additionally, the significant influx of tourists and pilgrims in GCC countries is boosting bottled water consumption, particularly in the hospitality and travel sectors. Policies promoting public health, water safety, and environmental sustainability are further supporting industry growth and fostering innovation. These factors collectively address environmental challenges, align with changing lifestyles, and meet evolving consumer preferences, driving the strong expansion of the GCC bottled water market.

Gulf Cooperation Council (GCC) Bottled Water Market Trends and Insights

Extreme climatic conditions drive structural demand

In the GCC, where extreme climatic conditions prevail, traditional water infrastructure is inadequate to meet critical hydration demands. Qatar, identified as the world's most water-stressed country with a 2023 Baseline water stress score of 5 by the World Resources Institute , highlights the role of bottled water as an essential infrastructure rather than a discretionary expense. Bahrain indicates that urban development projects exacerbate thermal stress and increase water consumption, showcasing the impact of urban heat island effects in the region. With temperatures often exceeding human tolerance levels, portable hydration becomes indispensable for outdoor workers and tourists. Due to limited local freshwater availability and the often poor taste or safety of tap water, residents and businesses heavily depend on bottled water as a reliable hydration source. Rising temperatures further drive the preference for ready-to-drink bottled water for use at home, in offices, and on the go, underscoring the significance of convenience.

Government water quality initiatives reshape market standards

Regional governments are introducing comprehensive water security frameworks, which are indirectly driving the demand for bottled water by addressing quality standards and infrastructure deficiencies. In March 2025, the GCC launched a regional water security task force, supported by USD 58 billion in environmental investments made between November 2024 and March 2025, showcasing significant policy coordination. Saudi Arabia's SWCC, acknowledged as the world's leading producer of desalinated water, achieved a daily production of over 11.5 million cubic meters in 2024 , according to the Saline Water Conversion Corporation (SWCC). Additionally, Bahrain's Electricity and Water Authority is actively encouraging residential water conservation while aiming for net-zero carbon emissions by 2060. This approach is fostering a perception of quality that benefits premium bottled water. Harmonized standards and certification systems streamline regulatory processes, facilitating market expansion and attracting international brands adhering to GCC norms. Government-led water quality initiatives bolster the safety and sustainability of bottled water products, enhancing consumer trust and fueling industry growth. While these initiatives elevate entry barriers for producers and foster innovation, they also steer the GCC bottled water market towards becoming a more standardized, trustworthy, and eco-conscious sector.

PET waste regulations create packaging transition costs

The Dubai Can initiative aims to eliminate single-use plastic bottles in the hospitality sector. United Arab Emirates residents' bottled water consumption significantly contributes to greenhouse gas emissions from PET production and disposal, prompting government actions such as waste separation mandates and the establishment of recycling facilities. As the initiative gains momentum in the hospitality sector, it pressures retail channels to comply, pushing manufacturers to adopt alternative packaging solutions despite higher unit costs. Regulatory progress is highlighted by collaborations like Majid Al Futtaim's partnership with Coca-Cola Middle East and Sparklo, which targets the collection of 1.8 million bottles annually through Reverse Vending Machines. The United Arab Emirates Circular Economy Policy 2031 indicates a potential shift from voluntary compliance to mandatory packaging standards. Companies face transition costs as they move toward aluminum and glass alternatives, with Agthia Group tripling its glass-bottled water production capacity to meet evolving regulatory demands.

Other drivers and restraints analyzed in the detailed report include:

- Health consciousness accelerates sugar-free beverage migration

- Tourism and pilgrimage expansion multiplies consumption touchpoints

- Water resource limitations constrain production scalability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Still Water retained a 76.30% revenue hold in 2025, yet functional and enhanced variants are tracking a 11.02% CAGR as wellness trends intensify. That trajectory mirrors the 50% beverage-tax policy that moved spending toward premium, low-calorie hydration. Functional recipes incorporating vitamins and electrolytes resonate with health-conscious millennials, while sparkling options cater to on-premise occasions. The GCC bottled water market size for functional formats is forecast to advance steadily on the back of higher unit margins and tourism-led exposure.

Despite its maturity, the Still segment benefits from broad price accessibility and entrenched consumer trust, especially in Saudi Arabia, where mass retail penetration is deepest. Marketers differentiate through mineral content origin stories and sustainability claims on source protection. Cross-promotions with sports events and religious gatherings also sustain baseline demand, ensuring the GCC bottled water market continues to anchor on core Still volumes even as functional innovation attracts discretionary spending.

Bottles between 331 ml and 500 ml delivered 39.30% of 2025 sales, capitalizing on portability during daily commutes and outdoor work shifts. These sizes are well-suited for on-the-go hydration, matching typical daily consumption needs. Their convenience has made them popular in offices, schools, hospitals, and retail environments. At the same time, households are increasingly opting for 501-1000 ml packs, which are the fastest-growing segment with an 8.12% CAGR, supported by e-commerce subscriptions enabling regular doorstep deliveries. As quick-commerce operators focus on SKUs that balance weight and economic efficiency, the share of these mid-range packs in the GCC bottled water market is expected to grow.

Institutional buyers, such as hospitals and labor camps, continue to purchase large 5-gallon dispensers, but single-serve volumes are gaining traction due to their higher per-liter margins and increased brand-switching. To adapt to these trends, Saudi factories have upgraded their filling lines to accommodate various pack sizes, ensuring they meet the shifting demands of retail and on-trade markets. Retail channels, which dominate the region, maintain significant stock of these sizes, particularly during sales peaks driven by seasonal events and growing urbanization.

The GCC Bottled Water Market Report is Segmented by Product Type (Still Water, Sparkling Water, and More), Packaging Size (<=330ml, 331-500ml, 501-1000ml, and More), Packaging Material (PET Bottles, Glass Bottles, and More), Distribution Channels (On-Trade, Off-Trade), and Geography (Saudi Arabia, United Arab Emirates, Kuwait, Qatar, Bahrain, Oman). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Liters).

List of Companies Covered in this Report:

- Nestle SA

- Agthia Group PJSC (Al Ain Water)

- Masafi LLC

- PepsiCo Inc. (Aquafina)

- Danone SA

- Mai Dubai LLC

- Hana Food Industries Co. (Hana Water)

- Berain Water

- Nova Water

- Almarai Company

- Crystal Mineral Water and Refreshments LLC

- Al-Qassim Water

- Al Furat Drinking Water LLC

- Al-Rawdatain Water Bottling Co.

- Rayyan Mineral Water Company (Qatar)

- Al Jomaih Water and Beverages

- New Technology Bottling Company KSCC

- The Coca-Cola Company

- Highland Spring Limited

- The Wonderful Company LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Extreme climatic conditions and year-round hydration needs

- 4.2.2 Government initiatives for drinking-water quality

- 4.2.3 Rising health consciousness and sugar-free beverage shift

- 4.2.4 Tourism and pilgrimage expansion multiplies consumption touchpoints

- 4.2.5 E-commerce and rapid-delivery expansion

- 4.2.6 Innovation in packaging and portability

- 4.3 Market Restraints

- 4.3.1 PET-plastic waste regulations and green taxes

- 4.3.2 Water scarcity and resource limitations

- 4.3.3 High energy cost of desalination bottling

- 4.3.4 Seasonal demand fluctuations

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By Product Type

- 5.1.1 Still Water

- 5.1.2 Sparkling Water

- 5.1.3 Functional / Enhanced Water

- 5.1.4 Flavored / Infused Water

- 5.2 Bt Packaging Size

- 5.2.1 <330 ml

- 5.2.2 331 ml-500 ml

- 5.2.3 501 ml-1000 ml

- 5.2.4 1001 ml- 2000 ml

- 5.2.5 2001 ml- 5000 ml

- 5.2.6 >5001 ml

- 5.3 By Packaging Material

- 5.3.1 PET Bottles

- 5.3.2 Glass Bottles

- 5.3.3 Aluminium Cans and Bottles

- 5.3.4 Others

- 5.4 By Distribution Channels

- 5.4.1 On-trade

- 5.4.2 Off-trade

- 5.4.2.1 Supermarkets / Hypermarkets

- 5.4.2.2 Convenience / Grocery Stores

- 5.4.2.3 Home and Office Space

- 5.4.2.4 Online Retail

- 5.4.2.5 Other Off-trade channels

- 5.5 By Geography

- 5.5.1 Saudi Arabia

- 5.5.2 United Arab Emirates

- 5.5.3 Kuwait

- 5.5.4 Qatar

- 5.5.5 Bahrain

- 5.5.6 Oman

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Nestle SA

- 6.4.2 Agthia Group PJSC (Al Ain Water)

- 6.4.3 Masafi LLC

- 6.4.4 PepsiCo Inc. (Aquafina)

- 6.4.5 Danone SA

- 6.4.6 Mai Dubai LLC

- 6.4.7 Hana Food Industries Co. (Hana Water)

- 6.4.8 Berain Water

- 6.4.9 Nova Water

- 6.4.10 Almarai Company

- 6.4.11 Crystal Mineral Water and Refreshments LLC

- 6.4.12 Al-Qassim Water

- 6.4.13 Al Furat Drinking Water LLC

- 6.4.14 Al-Rawdatain Water Bottling Co.

- 6.4.15 Rayyan Mineral Water Company (Qatar)

- 6.4.16 Al Jomaih Water and Beverages

- 6.4.17 New Technology Bottling Company KSCC

- 6.4.18 The Coca-Cola Company

- 6.4.19 Highland Spring Limited

- 6.4.20 The Wonderful Company LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK