PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2034993

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2034993

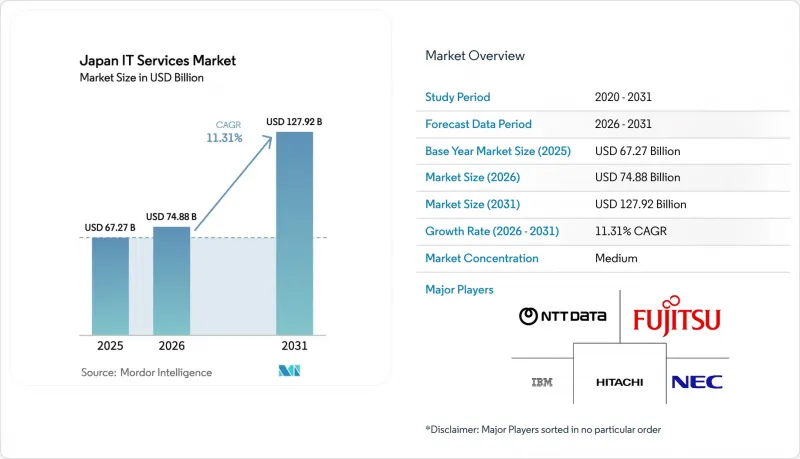

Japan IT Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Japan IT Services market size was valued at USD 67.27 billion in 2025 and estimated to grow from USD 74.88 billion in 2026 to reach USD 127.92 billion by 2031, at a CAGR of 11.31% during the forecast period (2026-2031).

Surging demand for core-system renewals ahead of the "2025 Digital Cliff," strong government backing for Society 5.0 initiatives, and cloud-first procurement rules for public agencies are sustaining double-digit expansion. Large enterprises are renewing mainframes, while small and medium enterprises (SMEs) are capitalizing on tax credits that subsidize up to 75% of software costs. Hyperscale datacenter buildouts and edge-computing rollouts are broadening the service mix toward platform and managed security offerings, and currency-driven cost pressures are accelerating offshore delivery adoption. Intensifying competition among traditional system integrators, cloud hyperscalers, and specialized cybersecurity vendors is reshaping pricing, margins, and consolidation strategies.

Japan IT Services Market Trends and Insights

DX Acceleration Under Society 5.0 Vision

Japan's Society 5.0 roadmap shifts enterprises from pilot-level automation to full-scale digitalization, creating large, multi-year transformation programs. Manufacturers such as Toyota linked 30,000 data points across 370 machines to streamline predictive maintenance, multiplying demand for systems integration services and edge analytics platforms. Service contracts are increasingly outcome-based, and consulting partners must deliver productivity gains without displacing labour, aligning with human-centric policy goals.

Cloud-First Procurement by Central and Municipal Agencies

The Digital Agency mandates that all new public-sector workloads adopt a cloud-first stance, removing on-premises default biases. Early movers have cut document handling times by 60%, proving the fiscal benefits of platform-as-a-service models. Multi-cloud rules lower vendor lock-in risk, boosting demand for orchestration and FinOps services and allowing mid-tier integrators to bid for government workloads previously gated by legacy procurement norms.

Structural Shortage of 800k IT Engineers by 2030

An aging workforce and limited STEM graduates produce a widening talent gap, raising salary costs and elongating project lead times. Large providers are scaling offshore centers in India and Vietnam, achieving up to 40% cost relief and reallocating scarce domestic engineers to client-facing roles.

Other drivers and restraints analyzed in the detailed report include:

- SME Tax Incentives for SaaS Adoption (2024-2027)

- 2025-Cliff" Legacy Risk Forcing Core-System Renewal

- JPY Weakness Inflating Imported IaaS Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

IT consulting and implementation secured 31.45% of the Japan IT Services market share in 2025, reflecting enterprises' need for strategic road-mapping ahead of major legacy sunsets. Japan IT Services market size for cloud and platform services is projected to expand at a 15.73% CAGR as hyperscale data centers multiply and government workloads shift to multi-cloud frameworks. Contract structures are pivoting from labour-based billing to value-based models that embed service-level outcomes, boosting average deal sizes. Aggressive transformation agendas at Fujitsu and NEC illustrate how incumbents' re-skill toward advisory and platform integration.

Standardization of cloud environments compresses margins in traditional IT outsourcing, but fuels cybersecurity and FinOps add-ons. Managed security services grow above 12% annually as cyber-insurance premiums spike and regulators mandate threat-monitoring baselines for critical infrastructure. Service providers packaging consulting, migration, and run operations into single contracts gain wallet share through lifecycle ownership.

Large organizations accounted for 67.25% of 2025 spending and drive complex, multi-year renewal projects focused on AI, analytics, and mainframe re-platforming. SMEs, energized by the IT Subsidy Program, post a 12.98% CAGR, unlocking pent-up demand for cloud ERP, HR, and security suites. Japan IT Services market size for SME projects is still comparatively small, yet the subsidy compresses adoption cycles and makes standardized delivery economical for vendors.

Providers targeting SMEs build productized, fixed-scope offerings that simplify procurement. Those reliant on subsidy leads face potential revenue cliffs after 2027 unless they transition clients to self-funded renewals. Large enterprises, meanwhile, deepen partnerships with a select roster of global and domestic integrators, driving vendor consolidation and longer contract tenures.

The Japan IT Services Market Report is Segmented by Service Type (IT Consulting & Implementation, IT Outsourcing, Business Process Outsourcing, Managed Security Services, & Cloud and Platform Services), Enterprise Size (Small and Medium Enterprises, & Large Enterprises), End-User Vertical (BFSI, Manufacturing, and More), and Deployment Model (Onshore, Near-Shore, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- NTT DATA Group Corp.

- NEC Corp.

- Fujitsu Ltd.

- Hitachi Ltd. (Hitachi Digital Services)

- IBM Japan Ltd.

- SCSK Corp.

- Internet Initiative Japan Inc.

- Nomura Research Institute Ltd.

- TIS Inc.

- Kyocera Communication Systems Co. Ltd.

- Nihon Unisys Ltd.

- Tokyo Electron Device Ltd.

- NS Solutions Corp.

- IIJ Global Solutions Inc.

- BellSystem24 Holdings Inc.

- Sakura Internet Inc.

- Oracle Japan Corp.

- Accenture Japan Ltd.

- Capgemini Japan K.K.

- Deloitte Tohmatsu Consulting LLC

- PwC Consulting LLP (Japan)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 DX acceleration under Society 5.0 vision

- 4.2.2 Cloud-first procurement by central and municipal agencies

- 4.2.3 SME tax incentives for SaaS adoption (2024-2027)

- 4.2.4 Surge in hyperscale and edge-DC build-outs

- 4.2.5 Managed security demand amid cyber-insurance premium hikes

- 4.2.6 Under-reported: "2025-Cliff" legacy risk forcing core-system renewal

- 4.3 Market Restraints

- 4.3.1 Structural shortage of 800 k IT engineers by 2030

- 4.3.2 JPY weakness inflating imported IaaS costs

- 4.3.3 On-prem lock-in within keiretsu supply chains

- 4.3.4 Under-reported: rising green-datacentre power curbs in Kanto

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Buyer Power

- 4.7.2 Supplier Power

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 IT Consulting and Implementation

- 5.1.2 IT Outsourcing (ITO)

- 5.1.3 Business Process Outsourcing (BPO)

- 5.1.4 Managed Security Services

- 5.1.5 Cloud and Platform Services

- 5.2 By End-User Enterprise Size

- 5.2.1 Small and Medium Enterprises (SMEs)

- 5.2.2 Large Enterprises

- 5.3 By End-User Vertical

- 5.3.1 BFSI

- 5.3.2 Manufacturing

- 5.3.3 Government and Public Sector

- 5.3.4 Healthcare and Life-Sciences

- 5.3.5 Retail and Consumer Goods

- 5.3.6 Telecom and Media

- 5.3.7 Logistics and Transport

- 5.3.8 Energy and Utilities

- 5.3.9 Other End-User Verticals

- 5.4 By Deployment Model

- 5.4.1 Onshore Delivery

- 5.4.2 Near-shore Delivery

- 5.4.3 Offshore Delivery

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 NTT DATA Group Corp.

- 6.4.2 NEC Corp.

- 6.4.3 Fujitsu Ltd.

- 6.4.4 Hitachi Ltd. (Hitachi Digital Services)

- 6.4.5 IBM Japan Ltd.

- 6.4.6 SCSK Corp.

- 6.4.7 Internet Initiative Japan Inc.

- 6.4.8 Nomura Research Institute Ltd.

- 6.4.9 TIS Inc.

- 6.4.10 Kyocera Communication Systems Co. Ltd.

- 6.4.11 Nihon Unisys Ltd.

- 6.4.12 Tokyo Electron Device Ltd.

- 6.4.13 NS Solutions Corp.

- 6.4.14 IIJ Global Solutions Inc.

- 6.4.15 BellSystem24 Holdings Inc.

- 6.4.16 Sakura Internet Inc.

- 6.4.17 Oracle Japan Corp.

- 6.4.18 Accenture Japan Ltd.

- 6.4.19 Capgemini Japan K.K.

- 6.4.20 Deloitte Tohmatsu Consulting LLC

- 6.4.21 PwC Consulting LLP (Japan)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment