PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035074

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035074

Renewable Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

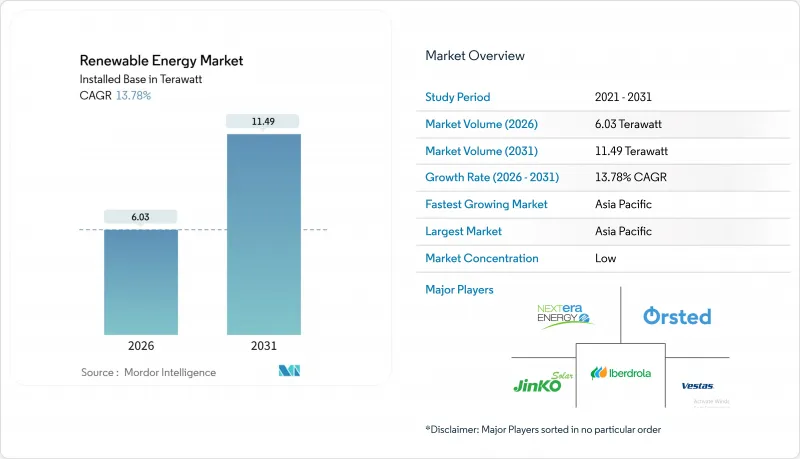

The Renewable Energy Market size in terms of installed base is expected to grow from 6.03 Terawatt in 2026 to 11.49 Terawatt by 2031, at a CAGR of 13.78% during the forecast period (2026-2031).

This expansion is anchored by multi-gigawatt corporate power-purchase agreements that pull projects forward, alongside green-hydrogen ventures that create demand unlinked to traditional grids. Module cost compression, faster permitting, and electrolyzer-driven offtake are converging to make incremental capacity economically attractive even in saturated markets. Competitive dynamics are shifting as independent power producers combine low cost of capital with turnkey EPC offerings, steadily eroding the position of vertically integrated utilities. Meanwhile, hybrid solar-wind-storage systems are emerging as a hedge against curtailment, offering dispatchable renewable electricity that accelerates long-duration storage adoption. In this context, the renewable energy market will see rising margin pressure on legacy developers but expanded opportunity for OEMs that integrate downstream.

Global Renewable Energy Market Trends and Insights

Corporate Power-Purchase Agreements Accelerating Utility-Scale Builds in North America & Europe

Corporate PPAs have matured into 15-20-year balance-sheet hedges that replace merchant risk with investment-grade credit, allowing developers to reach financial close more quickly than under traditional utility tenders. Meta's 1.5 GW portfolio with RWE in 2024 exemplifies how data-center offtakers underwrite multi-country pipelines, compressing solar build cycles to under 24 months and onshore wind to roughly 30 months. Developers prioritize contracted projects over speculative assets, so the renewable energy market is now paced by large buyers rather than regulators. As more corporates set science-based targets, aggregate demand is expected to exceed 40 GW of new capacity annually through 2030, reinforcing the long-term trajectory of the renewable energy market. The resulting visibility lowers the weighted average cost of capital and lifts the deployment ceiling in high-penetration grids.

Hyperscale Data-Centre Demand Boosting Solar-Wind Procurement in the Nordics & Ireland

AI workloads are driving electricity growth at cloud campuses, pushing operators to lock in renewable generation in regions with surplus hydro and wind. Google's 500 MW Norwegian wind deal illustrates how firms exploit the Nordics' clean-power mix, whereas grid congestion around Dublin has shifted investment toward Sweden and Finland. The renewable energy market responds by developing on-site solar and storage that reduce dependence on transmission-constrained nodes. This dynamic channels capital into distributed assets, encouraging grid-forming inverters and microgrid architectures. Near-term demand elasticity remains high, and developers that can bundle generation with batteries gain preferred-supplier status with hyperscalers.

Grid Congestion & Curtailment Risks in ERCOT (US) and Inner Mongolia (CN)

ERCOT curtailed 3.2 TWh of renewable electricity in 2024 as West Texas output overwhelmed transmission to Houston. Interconnection queues now exceed five years, delaying projects such as Enel's 300 MW Azure Sky wind farm until 2026. In China, Inner Mongolia's curtailment still hovers near 4%, prompting price discounts of 15-20% to place power with eastern buyers. These factors trim internal rates of return and temporarily defer roughly 10 GW of high-resource wind and solar additions. While new HVDC lines will eventually alleviate constraints, short-term drag on the renewable energy market CAGR is inevitable.

Other drivers and restraints analyzed in the detailed report include:

- Green-Hydrogen Gigawatt Pipelines Driving Capacity Additions in MENA & Australia

- EU REPowerEU Fast-Track Permitting Cutting Onshore-Wind Lead-Times in Southern Europe

- End-of-Life Blade Waste Regulations Raising Costs in Germany & France

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ocean Energy's 36.95% CAGR from 2026 to 2031 makes it the fastest-growing slice of the renewable energy market. Orbital Marine Power's 2 MW O2 tidal turbine in Orkney achieved a 74% capacity factor in its debut year, well above offshore wind norms, illustrating tidal predictability. Minesto's Dragon 12 kites convert low-velocity currents into useful electricity, expanding the resource base beyond high-flow straits. Solar Energy, at 44.61% renewable energy market share in 2025, maintains leadership thanks to crystalline-silicon panel prices that fell to USD 0.12 per watt in 2024 as polysilicon costs dropped below USD 8 per kilogram. Efficiency gains above 25% for TOPCon and heterojunction cells further compress balance-of-system expenses, sustaining competitive parity even in temperate zones.

Wind Energy contributes about 35% of 2025 capacity, benefiting from streamlined EU permitting and upgraded grid links in China. Offshore wind, however, faces escalating CAPEX for floating foundations that run USD 4-5 million per MW, compared with USD 3-4 million for fixed platforms. Hydropower expands modestly as site availability wanes, though China's 2.4 GW Baihetan pumped-storage plant demonstrates the value of eight-hour storage in a variable-renewable grid. Bioenergy and Geothermal remain niche at under 8%, constrained by feedstock price volatility and limited high-enthalpy reservoirs, yet Iceland's 90 MW Theistareykir expansion shows geothermal's baseload appeal. Collectively, technology diversification shields the renewable energy market from single-segment risk while offering investors multiple entry points.

The Renewable Energy Market Report is Segmented by Technology (Solar Energy, Wind Energy, Hydropower, Bioenergy, Geothermal, and Ocean Energy), End-User (Utilities, Commercial and Industrial, and Residential), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Sizes and Forecasts are Provided in Terms of Installed Capacity (GW).

Geography Analysis

Asia-Pacific dominated with 57.23% of capacity in 2025 and is forecast to advance at a 16.19% CAGR, led by China's 216 GW of 2024 installations and India's 500 GW 2030 target. Chinese state-owned developers are also exporting capital and equipment into Southeast Asia, Latin America, and Africa through concessional loans that bundle modules, turbines, and EPC services. India's offshore-wind tenders and production-linked incentives aim to localize manufacturing, curbing Chinese import reliance.

North America's build-out accelerates under the Inflation Reduction Act, which extends tax credits to 2032 and has already catalyzed USD 150 billion in domestic manufacturing commitments. The United States deployed 32 GW of solar and 8 GW of wind in 2024, although ERCOT's curtailments reveal transmission lag. Canada targets 90% renewable electricity by 2030 using hydropower and offshore wind, whereas Mexico's regulatory changes have chilled private investment despite strong irradiance. Europe leverages REPowerEU to compress permitting, with Spain and Greece benefiting most; Germany still battles interconnection delays exceeding 24 months.

The Middle East and Africa emerge as hydrogen exporters, evidenced by Saudi Arabia's NEOM (4 GW electrolyzer) and Egypt's 10 GW Gulf of Suez wind plan. South America's growth revolves around Brazil's 4 GW wind auction and Chile's USD 25/MWh solar corridor. Argentina co-locates solar with lithium mines to decarbonize processing. These regional dynamics collectively broaden the renewable energy market footprint and diversify supply chains.

- EPC Developers/Operators/Owners

- Equipment Suppliers

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Renewable Energy Mix, 2024

- 4.3 Market Drivers

- 4.3.1 Corporate Power-Purchase Agreements Accelerating Utility-scale Builds in North America & Europe

- 4.3.2 Hyperscale Data-Centre Demand Boosting Solar-Wind Procurement in the Nordics & Ireland

- 4.3.3 Green-Hydrogen Gigawatt Pipelines Driving Capacity Additions in MENA & Australia

- 4.3.4 EU 'REPowerEU' Fast-Track Permitting Cutting Onshore-Wind Lead-Times (<12 Months) in Southern Europe

- 4.4 Market Restraints

- 4.4.1 Grid Congestion & Curtailment Risks in ERCOT (US) and Inner Mongolia (CN)

- 4.4.2 End-of-Life Blade Waste Regulations Raising Costs in Germany & France

- 4.4.3 Lack of Long-Duration Storage Slowing High VRE Penetration in SE-Asia

- 4.4.4 Local-Content Mandates Inflating Offshore-Wind CAPEX in India & Brazil

- 4.5 Supply-Chain Analysis

- 4.6 Regulatory Outlook

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products & Services

- 4.8.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Technology

- 5.1.1 Solar Energy (PV and CSP)

- 5.1.2 Wind Energy (Onshore and Offshore)

- 5.1.3 Hydropower (Small, Large, PSH)

- 5.1.4 Bioenergy

- 5.1.5 Geothermal

- 5.1.6 Ocean Energy (Tidal and Wave)

- 5.2 By End-User

- 5.2.1 Utilities

- 5.2.2 Commercial and Industrial

- 5.2.3 Residential

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Spain

- 5.3.2.5 Nordic Countries

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Malaysia

- 5.3.3.6 Thailand

- 5.3.3.7 Indonesia

- 5.3.3.8 Vietnam

- 5.3.3.9 Australia

- 5.3.3.10 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Egypt

- 5.3.5.5 Rest of Middle East and Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, JVs, Funding, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Products & Services, Recent Developments)

- 6.4.1 EPC Developers/Operators/Owners

- 6.4.1.1 NextEra Energy, Inc.

- 6.4.1.2 Orsted A/S

- 6.4.1.3 Iberdrola, S.A.

- 6.4.1.4 EDF Renewables (EDF S.A.)

- 6.4.1.5 Duke Energy Corporation

- 6.4.1.6 Berkshire Hathaway Energy

- 6.4.1.7 Acciona Energia S.A.

- 6.4.1.8 Engie S.A.

- 6.4.1.9 China Three Gorges Corporation

- 6.4.1.10 Enel Green Power S.p.A.

- 6.4.1.11 Statkraft A.S.

- 6.4.1.12 Pattern Energy Group

- 6.4.1.13 Invenergy LLC

- 6.4.1.14 RWE Renewables GmbH

- 6.4.1.15 ACWA Power

- 6.4.1.16 EDP Renovaveis S.A.

- 6.4.1.17 Brookfield Renewable Partners L.P.

- 6.4.1.18 ReNew Energy Global PLC

- 6.4.1.19 Scatec ASA

- 6.4.2 Equipment Suppliers

- 6.4.2.1 First Solar, Inc.

- 6.4.2.2 Vestas Wind Systems A/S

- 6.4.2.3 Siemens Gamesa Renewable Energy S.A.

- 6.4.2.4 GE Vernova (General Electric)

- 6.4.2.5 JinkoSolar Holding Co. Ltd.

- 6.4.2.6 Canadian Solar Inc.

- 6.4.2.7 Longi Green Energy Technology Co., Ltd.

- 6.4.2.8 Goldwind Science & Technology Co., Ltd.

- 6.4.2.9 Trina Solar Co., Ltd.

- 6.4.2.10 Enphase Energy, Inc.

- 6.4.2.11 Sungrow Power Supply Co., Ltd.

- 6.4.2.12 Mitsubishi Power, Ltd.

- 6.4.2.13 Nordex SE

- 6.4.2.14 MHI Vestas Offshore Wind A/S

- 6.4.2.15 Shanghai Electric Group Co., Ltd.

- 6.4.2.16 Hitachi Energy Ltd.

- 6.4.2.17 ABB Ltd.

- 6.4.2.18 Climeon AB

- 6.4.2.19 Pelamis Wave Power Ltd. (in Administration)

- 6.4.2.20 Ocean Power Technologies, Inc.

- 6.4.1 EPC Developers/Operators/Owners

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment