PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043842

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043842

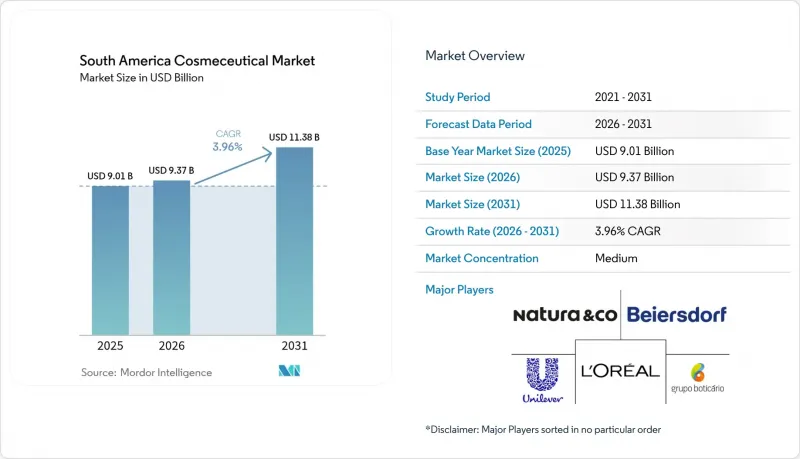

South America Cosmeceutical - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The South America cosmeceutical market size is expected to grow from USD 9.01 billion in 2025 to USD 9.37 billion in 2026 and is forecast to reach USD 11.38 billion by 2031 at 3.96% CAGR over 2026-2031.

The growing influence of dermatologists, a surge in e-commerce, and the region's rich biodiversity are transforming high-efficacy formulations from luxury items to clinical essentials, allowing for premium pricing in both pharmacies and online platforms. Local pharmaceutical firms are hastening acquisitions to bolster their skin-health portfolios and utilize their established prescription-drug logistics. In response, multinational companies are deploying AI-driven diagnostics, streamlining the journey from virtual consultation to purchase. Regulatory advancements, like ANVISA's RDC 907/2024 sandbox, are slashing bioactive time-to-market by roughly 18 months, giving an edge to early adopters. While challenges like currency fluctuations, counterfeit infiltration, and gaps in active ingredients pose hurdles, strategies such as product hybridization, smaller packaging, and tamper-proof seals are mitigating risks throughout the value chain.

South America Cosmeceutical Market Trends and Insights

Rising premium skin-health consciousness and dermatologist influence

In South America, dermatologists are evolving from mere prescribers to proactive brand advocates, a shift that is transforming cosmeceuticals from optional buys to essential clinical products. Data from ABIHPEC reveals that Brazil's dermocosmetics market is expanding, with brands exclusive to pharmacies reaping the lion's share of revenues. In 2024, L'Oreal Brazil notched up BRL 3.3 billion (USD 660 million) in sales through pharmacies. With an ambitious goal to double its total revenue by 2027, the company is weaving dermatologist training programs into its market approach. Galderma is marketing hyaluronic acid fillers and PLLA biostimulatory agents as "conscious self-care" for the youth. This move underscores a wider trend: aesthetic treatments and home-use cosmeceuticals are increasingly offered in subscription packages, generating consistent revenue streams that outpace traditional cosmetics. In 2024, Natura reintroduced its Chronos Derma line, now featuring clinically trialed retinol concentrations. This move underscores a pivotal shift: even brands traditionally reliant on direct sales are now prioritizing clinical efficacy over brand legacy. As a result of this physician-driven demand, product lifecycles are shrinking. Formulations lacking peer-reviewed efficacy are swiftly losing ground on shelves to their clinically validated counterparts, often within just 12 to 18 months of their debut.

Digital and e-commerce penetration in beauty retail

In 2024, e-commerce platforms are breaking down the geographic barriers that once shielded retailers in tier-1 cities. This shift allows brands to connect with consumers in secondary markets without the need for physical distribution investments. MercadoLibre, a major player in Latin America, successfully shipped 1.377 billion items in 2024. Notably, 76% of these deliveries were made within 48 hours. This efficiency has effectively addressed the logistics challenges that once limited access to premium cosmeceuticals outside major cities like Sao Paulo, Buenos Aires, and Bogota. In October 2024, Natura forged a partnership with MercadoLibre in Brazil. By the end of the year, this collaboration had expanded to Argentina. The partnership seamlessly integrates Natura's 3 million direct-sales consultants with MercadoLibre's fulfillment network. This innovative approach melds personal recommendations with algorithm-driven upselling. Brazilian indie brand, Care Natural Beauty, showcases the potential of direct-to-consumer sales. The brand earns a significant 80% of its revenue from its own e-commerce platform, reserving just 20% for sales through Sephora and other third-party marketplaces. This strategy underscores the viability of maintaining premium pricing without compromising on retailer margins. In 2024, ANVISA, Brazil's health regulatory agency, set up an e-commerce working group. Their goal is to standardize online cosmetic sales regulations across states. This move indicates a shift in regulatory perspectives, leaning towards embracing digital-first distribution. In Argentina, the impact of this shift is especially evident. Faced with hyperinflation, consumers began real-time price comparisons across various platforms. This behavior turned transparent online pricing into a significant competitive edge, rather than merely a tactic to undercut prices.

Currency volatility and inflation pressuring premium pricing

As of December 2024, Argentina's annual inflation rate hit a staggering 117.8%, as reported by INDEC. This surge has significantly curtailed the discretionary spending power of many, pushing premium cosmeceuticals out of reach for middle-income consumers. For instance, a standard 400ml shampoo now retails at ARS 4,855 (approximately USD 4.86), and a basic deodorant is priced at ARS 2,653 (around USD 2.65). Throughout 2024, these products saw monthly price hikes between 1.6% and 3.5%. In response, brands have been compelled to downsize their SKU offerings, ensuring prices remain below the psychologically significant ARS 3,000 mark. Meanwhile, in Brazil, the real's depreciation against the dollar, while not as drastic as Argentina's peso collapse, still exerts margin pressures on brands importing active ingredients from Europe or Asia. This is underscored by ANVISA's stipulation that mandates 95% of L'Oreal Brazil's portfolio be produced locally, highlighting the strategic necessity for brands to localize their supply chains. This currency challenge hits harder for brands focusing on natural or organic formulations. These products often depend on imported certification and testing services, which are priced in hard currency, leading to a cost structure that's 15% to 25% steeper than their conventional counterparts. In light of these challenges, brands are adapting: some are downsizing package sizes, others are cutting back on active-ingredient concentrations to trim input costs, and a few are even stepping away from premium tiers altogether. Such moves, while aimed at preserving short-term sales volumes, risk undermining long-term brand equity. This inflation-induced pivot towards value segments is especially evident in the hair care market. Here, consumers are shifting from high-end salon-exclusive brands to more affordable mass-market alternatives, which promise "good enough" performance at just half the price.

Other drivers and restraints analyzed in the detailed report include:

- Botanical bio-actives from amazon and Andean biomes

- Artificial Inteligence-driven personalized skin diagnostics and product customization

- High counterfeit penetration eroding consumer trust

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Skin Care Products held 48.10% market share, while Hair Care Products are projected to grow at a 9.45% CAGR through 2031, driven by the "skinification" trend emphasizing scalp health. In September 2025, Unilever's Dove brand launched 64 new hair care SKUs, supported by a EUR 1 billion (USD 1.1 billion) research and development program and over 20,000 patents utilizing robotics and nanotechnology for ingredient penetration. Natura's 2024 Lumina Anti-Aging Hair Regenerator targets gray hair reversal using biotechnology and Amazonian biodiversity actives, blending cosmeceuticals with regenerative medicine. Brazil, ranked 3rd globally in hair care consumption, saw advertising spending rise from BRL 44.9 billion (USD 9 billion) in 2022 to BRL 60.5 billion (USD 12.1 billion) in 2024, highlighting the category's importance. Anti-aging skin care now incorporates pharmaceutical-grade retinoids and peptides near prescription levels, drawing scrutiny under ANVISA's RDC 965/2025, which regulates active-ingredient limits for OTC products. Tele-dermatology boosts anti-acne products by enabling remote prescriptions of high-efficacy formulations. Sun protection remains key, with BASF's Uvinul TS Hydro, a water-soluble UV filter, addressing the need for lightweight, non-greasy sunscreens in humid climates. Lip and Oral Care Products are expanding with innovations like peptide-infused lip treatments and probiotic oral care solutions.

Hair care growth reflects shifting consumer behavior, with scalp health seen as an extension of facial skin care. Grupo Boticario's Eudora Siage line uses digital diagnostics for personalized scalp treatments, mirroring AI-driven facial skin care trends. Truss, a Brazilian professional hair care brand, reported 34% growth in salon channels in 2024 by positioning scalp products as clinical solutions. L'Oreal's 2024 launch of a line for wavy, kinky, and curly hair addresses South America's diverse textures, a segment often underserved by global brands. Growth is further supported by combined-use products like cleansing-conditioners and hair removal-moisturizers, catering to 75% of Brazilian men who report limited leisure time. Regulatory oversight in hair care remains minimal compared to skin care, as ANVISA's limits primarily apply to leave-on facial products, allowing higher active-ingredient levels in scalp treatments.

In 2025, conventional formulations held a 67.85% market share, while natural and organic products are projected to grow at an 8.34% CAGR through 2031, driven by consumer demand for mental health-focused beauty routines. WGSN's 2024 research shows 49% of Brazilians favor products with mental health benefits, prompting brands to position natural ingredients as wellness solutions. Ecocert's COSMOS standard, active in over 130 countries, including Argentina, certifies authentic natural/organic products but raises production costs by 15% to 25% due to imported testing services. Natura's commitment to 100% regenerative sourcing by 2050, supported by BRL 230 million (USD 46 million) in bioeconomy investments, highlights the shift of natural/organic positioning to a core business model. Brazil's Lei 13.123/2015 ensures indigenous communities receive royalties for traditional knowledge used in formulations, adding cost and compliance challenges.

Conventional formulations dominate due to superior efficacy, longer shelf life, and affordability, especially in an inflationary environment. The natural/organic segment faces perception issues, with consumers viewing certified products as less effective, particularly in anti-aging and anti-acne categories. Brands are addressing this by hybridizing formulations, combining natural bioactives like Amazonian oils with synthetic preservatives, creating a "clean clinical" category. Lola From Rio, a vegan Brazilian brand that merged with Skala and gained Advent International's backing in 2024, shows how indie brands can scale in the natural/organic segment while maintaining mass-market pricing. Regulatory oversight is increasing, with ANVISA's RDC 949/2024 requiring brands to substantiate biodiversity sourcing and benefit-sharing claims. The fragmented certification landscape, COSMOS, USDA NOP, Fair Trade, NATRUE, and ISO 16128, creates consumer confusion and compliance burdens for brands in South America.

The South America Cosmeceutical Market is Segmented by Product Type (Skin Care Products, Hair Care Products, Lip Care Products, and Oral Care Products), Category (Conventional and Natural/Organic), End User (Men and Women), Distribution Channel (Supermarkets and Hypermarkets, Beauty and Health Stores, Online Retail Stores, and Other Distribution Channels), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Natura & Co

- Grupo Boticario

- L'Oreal

- Unilever

- Procter & Gamble

- Beiersdorf

- Estee Lauder

- Johnson & Johnson

- Shiseido

- Galderma

- Pierre Fabre

- Hypera Pharma

- Eurofarma (Dermage)

- Cimed (Milimetric)

- Ache (Profuse)

- Coty

- Clarins

- Avon

- LVMH

- Mary Kay

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising premium skin-health consciousness and dermatologist influence

- 4.2.2 Digital and e-commerce penetration in beauty retail

- 4.2.3 Botanical bio-actives from Amazon and Andean biomes

- 4.2.4 AI-driven personalized skin diagnostics and product customization

- 4.2.5 Pharma convergence and mergers, and acquisitions are fueling high-efficacy formulations

- 4.2.6 Physician-dispensed channel expansion via tele-dermatology

- 4.3 Market Restraints

- 4.3.1 Currency volatility and inflation pressuring premium pricing

- 4.3.2 High counterfeit penetration eroding consumer trust

- 4.3.3 Regulatory gaps around dermocosmetics and active-ingredient limits

- 4.3.4 Logistics fragmentation outside tier-1 cities

- 4.4 Consumer Behaviour Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Product Type

- 5.1.1 Skin Care Products

- 5.1.1.1 Anti-ageing

- 5.1.1.2 Anti-acne

- 5.1.1.3 Sun Protection

- 5.1.1.4 Other Skin-care Products

- 5.1.2 Hair Care Products

- 5.1.2.1 Shampoos and Conditioners

- 5.1.2.2 Hair Colourants and Dyes

- 5.1.2.3 Other Hair-care Products

- 5.1.3 Lip Care Products

- 5.1.4 Oral Care Products

- 5.1.1 Skin Care Products

- 5.2 Category

- 5.2.1 Conventional

- 5.2.2 Natural/Organic

- 5.3 End User

- 5.3.1 Male

- 5.3.2 Female

- 5.4 By Distribution Channel

- 5.4.1 Supermarkets and hypermarkets

- 5.4.2 Beauty and Health Stores

- 5.4.3 Online Retail Stores

- 5.4.4 Other Distribution Channels

- 5.5 Geography

- 5.5.1 Brazil

- 5.5.2 Argentina

- 5.5.3 Colombia

- 5.5.4 Peru

- 5.5.5 Chile

- 5.5.6 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Natura & Co

- 6.4.2 Grupo Boticario

- 6.4.3 L'Oreal

- 6.4.4 Unilever

- 6.4.5 Procter & Gamble

- 6.4.6 Beiersdorf

- 6.4.7 Estee Lauder

- 6.4.8 Johnson & Johnson

- 6.4.9 Shiseido

- 6.4.10 Galderma

- 6.4.11 Pierre Fabre

- 6.4.12 Hypera Pharma

- 6.4.13 Eurofarma (Dermage)

- 6.4.14 Cimed (Milimetric)

- 6.4.15 Ache (Profuse)

- 6.4.16 Coty

- 6.4.17 Clarins

- 6.4.18 Avon

- 6.4.19 LVMH

- 6.4.20 Mary Kay

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK