PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044120

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044120

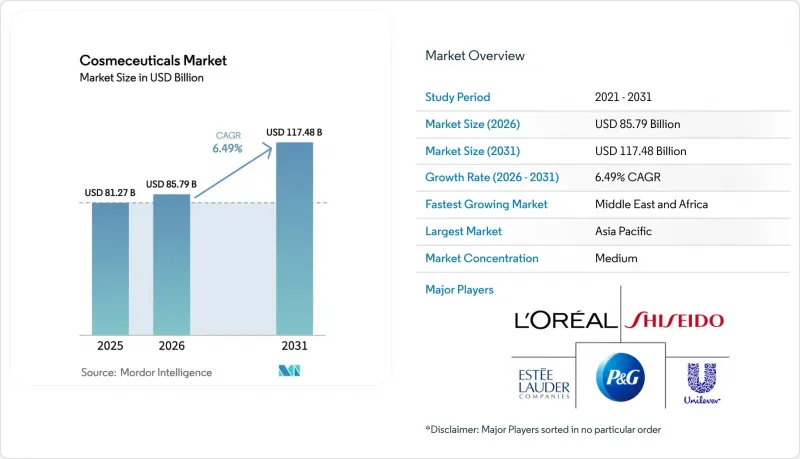

Cosmeceuticals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The cosmeceuticals market size is projected to expand from USD 81.27 billion in 2025 and USD 85.79 billion in 2026 to USD 117.48 billion by 2031, registering a compound annual growth rate (CAGR) of 6.49% between 2026 and 2031.

This growth in the cosmeceuticals market is driven by increasing demand for dermatologist-recommended active ingredients, stricter regulatory oversight on efficacy claims, and a rising consumer focus on preventive skin health. Premium pricing is concentrated on formulations containing encapsulated retinoids, collagen-stimulating peptides, and broad-spectrum antioxidants, which deliver visible results within 8 to 12 weeks. Sun protection products combining ultraviolet (UV) filters with free-radical neutralizers are gaining market share, supported by public health campaigns promoting melanoma awareness. Additionally, probiotic and prebiotic blends are expanding the market by appealing to microbiome-conscious consumers. Omnichannel distribution strategies in the cosmeceuticals market enable brands to capture both in-store consultation traffic and the rapidly growing direct-to-consumer sales. Market consolidation in the cosmeceuticals market remains moderate, with global conglomerates leveraging patented delivery systems, while prescription-channel specialists maintain pricing by combining pharmaceutical credibility with cosmetic appeal.

Global Cosmeceuticals Market Trends and Insights

Increasing consumer interest in anti-aging solutions for wrinkles, pigmentation, and firmness using clinically proven actives

The demand within the cosmeceuticals market for anti-aging is evolving as consumers shift from aspirational beauty to results-oriented skincare, expecting visible improvements in fine lines and hyperpigmentation within 8 to 12 weeks. A 2025 Delphi consensus study published in the Journal of the European Academy of Dermatology and Venereology identified retinoids, niacinamide, vitamin C, and azelaic acid as the most dermatologist-recommended ingredients for addressing photoaging. This aligns with consumer preferences for evidence-based formulations over proprietary blends. Clinical validation of these ingredients is driving premiumization across the cosmeceuticals market, with products containing encapsulated retinol or stabilized L-ascorbic acid priced 30% to 50% higher than conventional moisturizers, while maintaining strong sales in prestige channels. Additionally, the adoption of at-home diagnostic tools, such as AI-powered skin analyzers that measure wrinkle depth and pigment distribution, is accelerating this trend by enabling consumers to objectively track product efficacy. Brands that fail to substantiate anti-aging claims with clinical trial data face potential regulatory scrutiny under the EU's Cosmetics Regulation 1223/2009, which requires efficacy claims to be supported by adequate evidence. This factor is projected to contribute 1.8 percentage points to the overall CAGR, with peak impact expected in the medium term as personalized formulation platforms continue to develop.

Rising awareness of skin cancer, photoaging, and UV damage driving demand for advanced dermocosmetic sun protection

Growing awareness is increasing the demand for hybrid formulations that combine UV filters with antioxidants, such as niacinamide and ferulic acid. These antioxidants help neutralize free radicals generated by UV exposure and provide additional protection beyond Sun Protection Factor (SPF) ratings. In Japan, the quasi-drug classification for sunscreens requires rigorous efficacy testing, creating a regulatory advantage for established companies like Shiseido and Kao. These companies invest in photostable filter technologies, including Tinosorb M and Uvinul A Plus. In Australia, where melanoma rates are among the highest globally, the Therapeutic Goods Administration enforces strict water-resistance standards for sunscreens. This has driven innovation in long-wear formulations that maintain SPF efficacy even after 80 minutes of water immersion . Furthermore, the Centers for Disease Control and Prevention (CDC) 2024 guidelines recommend daily SPF 30+ application for all skin types, including darker phototypes that were previously underserved by cosmetic sunscreens, thereby expanding the addressable cosmeceuticals market.

Regulatory ambiguity impacts claims and product classification

The absence of a unified cosmeceutical category across major markets creates compliance challenges, particularly for smaller brands without dedicated regulatory teams. In the United States, the Food and Drug Administration (FDA) regulates cosmeceuticals under the Federal Food, Drug, and Cosmetic Act. This act defines cosmetics as products intended to cleanse or beautify, while drugs are defined as products intended to treat or prevent disease. Many cosmeceuticals fall between these definitions, often using claims such as "reduce the appearance of wrinkles" instead of "treat wrinkles" to avoid being classified as drugs. In the European Union, Cosmetics Regulation 1223/2009 enforces stricter requirements, such as limiting retinol concentrations to 0.3% in leave-on products and mandating safety assessments for nano-ingredients. These regulations compel brands to reformulate products for regional compliance, increasing inventory complexity. Meanwhile, China's 2024 cosmetics supervision regulations require efficacy substantiation for anti-aging and whitening claims. Brands must submit clinical trial data to the National Medical Products Administration, a process that can delay product launches by 6 to 12 months.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of dermatologist-recommended and prescription-based skincare boosting credibility of cosmeceutical brands

- Rapid advancements in active ingredients like peptides, retinoids, antioxidants, and plant stem cells

- High research and development costs affect profitability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Skin care products accounted for 58.42% of the global cosmeceuticals market in 2025, driven by multi-step routines that include serums, moisturizers, and sunscreens to address concerns such as photoaging, hyperpigmentation, and barrier dysfunction. Anti-aging formulations containing retinoids and peptides held the largest share within the skin care segment, appealing primarily to consumers aged 35 to 55 who focus on reducing wrinkles and improving skin firmness. Additionally, anti-acne products targeting adult acne in both men and women are gaining traction, supported by increased dermatological prescriptions of adapalene and salicylic acid for persistent breakouts.

Sun protection products are gaining traction across the cosmeceuticals market due to rising awareness of melanoma risks, with hybrid formulations that combine broad-spectrum ultraviolet (UV) filters and antioxidants like niacinamide offering enhanced photoprotection beyond sun protection factor (SPF) ratings. This positioning is particularly effective in high-UV regions such as Australia and Southern Europe. Lip care products, while smaller in market size, are projected to grow at an annual rate of 6.99% through 2031, the fastest among product types. This growth is driven by the introduction of peptide-infused balms and hyaluronic acid treatments targeting perioral wrinkles and volume loss, conditions previously addressed primarily through injectable fillers.

Conventional formulations accounted for 71.32% of the cosmeceuticals market in 2025, driven by consumer confidence in synthetic active ingredients such as retinoids, niacinamide, and alpha hydroxy acids. These ingredients have a long history of clinical validation and consistent efficacy. Conventional formulations benefit from established supply chains, lower raw material costs, and regulatory precedents. These factors enable brands to scale production efficiently and offer competitive pricing in mass retail channels.

In comparison, natural and organic cosmeceuticals are projected to grow at an annual rate of 7.83% through 2031, exceeding the growth rate of conventional products by 1.34 percentage points. This growth is being driven by increasing consumer demand for microbiome-friendly formulations, vegan certifications, and transparent ingredient sourcing. Younger demographics, particularly Generation Z (Gen Z) and millennials, are leading this trend. They view clean beauty as an extension of sustainability values and are willing to pay 20% to 30% premiums for products certified by organizations such as Ecocert and The Vegan Society.

The Cosmeceuticals Market Report is Segmented by Product Type (Skin Care Products, Hair Care Products, and More), Category (Conventional, and Natural/Organic), End-User (Male, and Female), Distribution Channel (Supermarkets/Hypermarkets, Beauty and Health Stores, and More), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

In 2025, the Asia-Pacific region led the global cosmeceuticals market, accounting for 35.13% of the total share. This leadership was supported by strict sun protection regulations in countries like Japan and South Korea, where UV filters are classified as quasi-drugs requiring efficacy validation. Additionally, China's 2024 cosmetics supervision regulations require clinical substantiation for anti-aging and whitening claims. Japan's aging population, with 29% of residents over the age of 65, is driving demand for formulations containing firmness-enhancing peptides and retinoids. Meanwhile, South Korea's K-beauty export ecosystem is globalizing innovations such as centella asiatica extracts and fermented ingredients, which combine traditional botanicals with clinical validation. In India, the cosmeceuticals market is expanding as dermatologists increasingly recommend active-based regimens for conditions like hyperpigmentation and melasma, which are common in darker skin phototypes. Brands such as Cipla's Excela and Abbott's Deriva are positioning themselves as cost-effective alternatives to Western premium lines.

The Middle East and Africa, while representing a smaller cosmeceuticals market share in 2025, are projected to grow at an annual rate of 8.21% through 2031, making it the fastest-growing region. This growth is driven by the increasing demand for halal-certified dermocosmetics, which combine religious compliance with clinical efficacy. Saudi Arabia and the United Arab Emirates are leading this growth, with consumers prioritizing products free from alcohol and animal-derived ingredients. Halal certification is a critical factor in these markets, where it is considered essential for personal care products.

North America maintained a significant market share of the cosmeceuticals market in 2025, supported by high consumer awareness of dermatologist-recommended skincare products and well-established distribution channels. These include specialty retailers such as Sephora and Ulta, as well as direct-to-consumer platforms offering personalized formulations like tretinoin and niacinamide. The United States Food and Drug Administration's (FDA) regulatory framework, which classifies cosmeceuticals under the Federal Food, Drug, and Cosmetic Act without a distinct category, adds compliance complexity. However, it also allows brands to make structure-function claims that are restricted in other markets.

- L'Oreal S.A.

- Procter & Gamble Co.

- Unilever PLC

- Shiseido Co., Ltd.

- The Estee Lauder Companies Inc.

- Beiersdorf AG

- Kao Corporation

- Groupe Clarins SA

- Galderma Holding SA

- Colgate-Palmolive Co.

- Amorepacific Corp.

- Kose Corp.

- LVMH Moet Hennessy Louis Vuitton SE

- Pierre Fabre S.A.

- Natura &Co Holding S.A.

- Revlon Inc.

- Rohto Pharmaceutical Co., Ltd.

- Kenvue Inc.

- Henkel AG & Co. KGaA

- Puig S.L.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing consumer interest in anti-aging solutions for wrinkles, pigmentation, and firmness using clinically proven actives

- 4.2.2 Rising awareness of skin cancer, photoaging, and UV damage driving demand for advanced dermocosmetic sun protection

- 4.2.3 Expansion of dermatologist-recommended and prescription-based skincare boosting credibility of cosmeceutical brands

- 4.2.4 Rapid advancements in active ingredients like peptides, retinoids, antioxidants, and plant stem cells

- 4.2.5 Growing preference for clean, vegan, and microbiome-friendly formulations with transparent ingredient lists

- 4.2.6 Increasing adoption of men's grooming and skincare routines featuring anti-aging and anti-acne products

- 4.3 Market Restraints

- 4.3.1 Regulatory ambiguity impacts claims and product classification

- 4.3.2 High research and development costs affect profitability

- 4.3.3 Short product life cycles drive constant innovation

- 4.3.4 Adverse reactions limit adoption among sensitive users

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Skin Care Products

- 5.1.1.1 Anti-ageing

- 5.1.1.2 Anti-acne

- 5.1.1.3 Sun Protection

- 5.1.1.4 Other Skin-care Products

- 5.1.2 Hair Care Products

- 5.1.2.1 Shampoos and Conditioners

- 5.1.2.2 Hair Colourants and Dyes

- 5.1.2.3 Other Hair-care Products

- 5.1.3 Lip Care Products

- 5.1.4 Oral Care Products

- 5.1.1 Skin Care Products

- 5.2 By Category

- 5.2.1 Conventional

- 5.2.2 Natural/Organic

- 5.3 By End-User

- 5.3.1 Male

- 5.3.2 Female

- 5.4 By Distribution Channel

- 5.4.1 Supermarkets/Hypermarkets

- 5.4.2 Beauty and Health Stores

- 5.4.3 Online Retail Stores

- 5.4.4 Other Distribution Channels

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 Italy

- 5.5.2.4 France

- 5.5.2.5 Spain

- 5.5.2.6 Netherlands

- 5.5.2.7 Poland

- 5.5.2.8 Belgium

- 5.5.2.9 Sweden

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Indonesia

- 5.5.3.6 South Korea

- 5.5.3.7 Thailand

- 5.5.3.8 Singapore

- 5.5.3.9 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Chile

- 5.5.4.5 Peru

- 5.5.4.6 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 L'Oreal S.A.

- 6.4.2 Procter & Gamble Co.

- 6.4.3 Unilever PLC

- 6.4.4 Shiseido Co., Ltd.

- 6.4.5 The Estee Lauder Companies Inc.

- 6.4.6 Beiersdorf AG

- 6.4.7 Kao Corporation

- 6.4.8 Groupe Clarins SA

- 6.4.9 Galderma Holding SA

- 6.4.10 Colgate-Palmolive Co.

- 6.4.11 Amorepacific Corp.

- 6.4.12 Kose Corp.

- 6.4.13 LVMH Moet Hennessy Louis Vuitton SE

- 6.4.14 Pierre Fabre S.A.

- 6.4.15 Natura &Co Holding S.A.

- 6.4.16 Revlon Inc.

- 6.4.17 Rohto Pharmaceutical Co., Ltd.

- 6.4.18 Kenvue Inc.

- 6.4.19 Henkel AG & Co. KGaA

- 6.4.20 Puig S.L.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK