PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043991

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043991

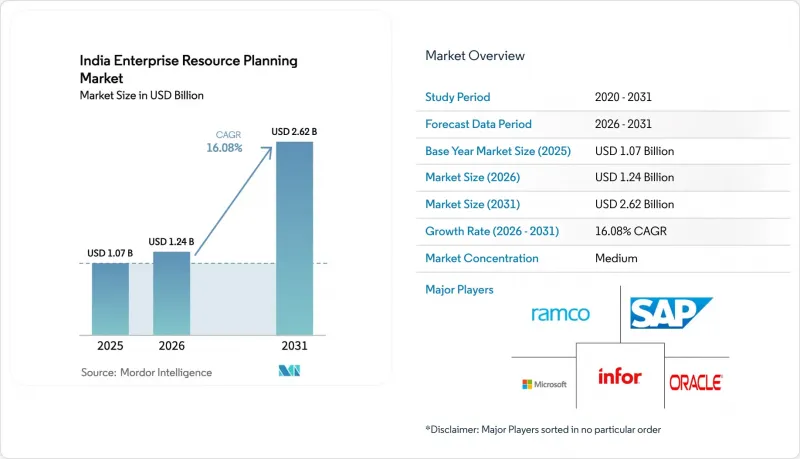

India Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The India Enterprise Resource Planning Market size is expected to grow from USD 1.07 billion in 2025 to USD 1.24 billion in 2026 and is forecast to reach USD 2.62 billion by 2031 at 16.08% CAGR over 2026-2031.

Accelerated Goods and Services Tax compliance deadlines, Digital India 2.0 subsidies, and aggressive cloud migration among mid-market manufacturers keep the demand curve steep. Regulatory mandates for e-invoicing above INR 5 crore, coupled with the Reserve Bank of India's real-time fraud monitoring rules, make ERP a statutory necessity. Cloud hyperscalers now operate availability zones in Hyderabad, Pune, and Mumbai, reducing latency to single-digit milliseconds and eliminating the last technical argument for on-premise systems. Tier-II manufacturing belts in Gujarat, Tamil Nadu, and Maharashtra feed a parallel edge-ERP wave that synchronizes shop-floor sensors with back-office finance modules in near real time, proving that industrial IoT is no longer a privilege reserved for Fortune 500 companies.

India Enterprise Resource Planning Market Trends and Insights

Government Push for GST and Compliance

The phased e-invoice rollout forces 2.8 million enterprises to adopt compliant ERP suites. Ministry of Corporate Affairs audit-trail mandates add timestamp and hash requirements that spreadsheets cannot meet. Vendors with pre-certified GST packs captured 68% of SME installations in H1 2025. A looming reverse-charge mechanism for cross-border services is already driving upgrades to procurement modules, while the 22% jump in e-way bill integrations shows logistics workflows are equally exposed. States differ in legacy VAT nuances, so hyper-local configuration capability has become a decisive vendor differentiator.

Growing Digital Transformation Initiatives

Digital India 2.0 earmarks INR 14,000 crore for public-sector digitization and sets a target of onboarding 500,000 MSMEs onto cloud platforms by 2027. Subsidized ERP licenses offered via Common Services Centres drop acquisition costs by up to 60% for eligible firms. Private surveys of 1,200 CFOs show 71% already executing core-system modernization, with cloud ERP topping the investment list. Production-Linked Incentive schemes across electronics, pharma, and textiles explicitly require real-time production data, embedding ERP deep into subsidy compliance. State-owned enterprises such as Bharat Electronics issue unified ERP tenders, encouraging smaller vendors to obtain ISO 27001 and CERT-In certifications if they wish to compete.

High Implementation Costs

Total ownership for a mid-market roll-out spans USD 150,000-500,000, well above the comfort zone of micro-enterprises. A SIDBI survey shows 48% of SMEs cite cost as the top deterrent, even with 36-month cloud subscriptions. Customization inflates budgets by another 40% because informal credit cycles and consignment sales need bespoke code. Collateral-free loans for digitization posted only 12,000 approvals by January 2026, reflecting both lender caution and borrower reluctance. Vendors experiment with starter tiers priced at INR 499 per user per month, yet stripped-down features often trigger mid-contract upgrades, recreating the affordability barrier they aimed to solve.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Adoption of Cloud-Based Solutions

- Rising Demand for Industry 4.0-Ready Edge ERP in Tier II Manufacturing Clusters

- Data Security and Privacy Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-native suites represented 53.77% of deployments in 2025. Vendors decouple modules, letting customers consume microservices on demand and update features without downtime. This approach delivers a 17.68% CAGR by 2031, as transaction-based pricing aligns costs with business cycles. Mobile-first ERP appeals to warehouse staff and field sales who need inventory and order visibility on smartphones; roll-outs at large retailers validate its utility at scale. Social and collaborative ERP weaves chat and co-editing into transactional screens but remains a niche preference among professional-services firms. Two-tier and edge ERP, forecast to expand at 18.7% CAGR, wins favor with multinationals that keep a lean regional ledger for tax compliance while aggregating globally. Tata Motors' January 2026 pilot at Sanand and Pune plants processes quality images locally, proving edge ERP's latency advantage. Draft cyber-physical standards from the Bureau of Indian Standards recommend edge computing for industrial latency under 100 milliseconds, further legitimizing the architecture.

Finance and accounting accounted for 29.45% of the functional share in 2025. Continuous audit-trail mandates and GST e-invoice thresholds make automated reconciliation non-negotiable. ICICI Bank APIs link ERP cash positions to treasury desks for real-time liquidity optimization, driving deeper integration. Supply-chain and operations modules keep e-commerce warehouses stocked through algorithmic replenishment, while HR updates track provident-fund compliance. Manufacturing execution and quality grow fastest, at a 17.1% CAGR, as PLI schemes tie subsidies to verified digital output. Pharma producers embed electronic batch records to meet new Schedule M guidelines, and customer relationship modules let tractor buyers configure equipment online, bridging traditional and digital channels. Vendors offering pre-integrated MES and ERP suites secure the inside track for the next upgrade cycle.

The India Enterprise Resource Planning Market Report is Segmented by Type (Cloud-Native Suite, Mobile-First ERP, and More), Business Function (Finance and Accounting, and More), Deployment Model (On-Premise, and Cloud), Organization Size (Large Enterprises, and Small and Medium Enterprises), and Industry Vertical (Manufacturing, BFSI, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infor Inc.

- Epicor Software Corporation

- The Sage Group plc

- Tally Solutions Pvt. Ltd.

- Zoho Corporation Pvt. Ltd.

- Focus Softnet Pvt. Ltd.

- Acumatica Inc.

- Deltek Inc.

- SYSPRO (Pty) Ltd

- Deskera Holdinigs Ltd.

- Unit4 N.V.

- Intuit Inc.

- Marg ERP Ltd.

- Busy Infotech Pvt. Ltd.

- Ramco Systems Limited

- Prismatic Technologies Pvt. Ltd.

- IFS AB

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Digital Transformation Initiatives

- 4.2.2 Increasing Adoption of Cloud-Based Solutions

- 4.2.3 Government Push for GST and Compliance

- 4.2.4 Rising Demand for Industry 4.0-Ready Edge ERP in Tier II Manufacturing Clusters

- 4.2.5 Emergence of Unified Payments Interface-Integrated ERP for MSMEs

- 4.2.6 Surge in India-Specific AI Language Models Enabling Vernacular ERP Interfaces

- 4.3 Market Restraints

- 4.3.1 High Implementation Costs

- 4.3.2 Data Security and Privacy Concerns

- 4.3.3 Shortage of Domain-Skilled ERP Consultants in Non-Metro Cities

- 4.3.4 Resistance from Family-Owned SMEs to Process Standardization

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Degree of Competition

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Cloud-Native Suite

- 5.1.2 Mobile-First ERP

- 5.1.3 Social / Collaborative ERP

- 5.1.4 Two-Tier / Edge ERP

- 5.2 By Business Function

- 5.2.1 Finance and Accounting

- 5.2.2 Supply-Chain and Operations

- 5.2.3 Human Capital Management

- 5.2.4 Customer Relationship and Commerce

- 5.2.5 Manufacturing Execution and Quality

- 5.3 By Deployment Model

- 5.3.1 On-Premise

- 5.3.2 Cloud

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By Industry Vertical

- 5.5.1 Manufacturing

- 5.5.2 Retail and E-commerce

- 5.5.3 BFSI

- 5.5.4 Government and Public Sector

- 5.5.5 IT and Telecom

- 5.5.6 Healthcare and Life Sciences

- 5.5.7 Others Industry Vertical

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 Infor Inc.

- 6.4.5 Epicor Software Corporation

- 6.4.6 The Sage Group plc

- 6.4.7 Tally Solutions Pvt. Ltd.

- 6.4.8 Zoho Corporation Pvt. Ltd.

- 6.4.9 Focus Softnet Pvt. Ltd.

- 6.4.10 Acumatica Inc.

- 6.4.11 Deltek Inc.

- 6.4.12 SYSPRO (Pty) Ltd

- 6.4.13 Deskera Holdinigs Ltd.

- 6.4.14 Unit4 N.V.

- 6.4.15 Intuit Inc.

- 6.4.16 Marg ERP Ltd.

- 6.4.17 Busy Infotech Pvt. Ltd.

- 6.4.18 Ramco Systems Limited

- 6.4.19 Prismatic Technologies Pvt. Ltd.

- 6.4.20 IFS AB

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment