PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044218

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044218

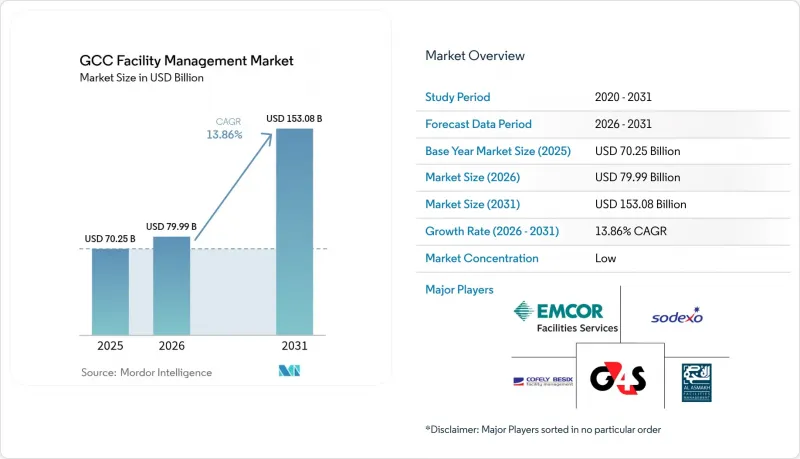

GCC Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The GCC Facility Management Market size is expected to increase from USD 70.25 billion in 2025 to USD 79.99 billion in 2026 and reach USD 153.08 billion by 2031, growing at a CAGR of 13.86% over 2026-2031.

Accelerated diversification initiatives led by Saudi Arabia's Vision 2030 and the UAE's Smart City agenda continued to reshape corporate approaches to facilities, prompting rapid adoption of artificial-intelligence and Internet-of-Things platforms for building management. Megaproject pipelines such as NEOM, the King Salman International Airport expansion, and Dubai's ongoing mixed-use developments underpinned robust demand for outsourced services, while data-center construction and mandatory green-building schemes reinforced specialized hard-service requirements. Competitive intensity remained moderate, yet technology investment and rising labor localization thresholds triggered consolidation pressure as smaller suppliers struggled to fund digital upgrades and training programs.

GCC Facility Management Market Trends and Insights

AI and IoT Integration in Building Management

The UAE piloted AI-enabled digital twins at DEWA's Al Shera'a headquarters, setting a regional benchmark for 30% energy savings and real-time asset analytics. Enova's Gemini-powered virtual assistant illustrated how cloud AI streamlined work-order resolution across mixed portfolios.Saudi developers followed suit, embedding IoT sensors in commercial towers within Riyadh's King Abdullah Financial District to monitor more than 100,000 assets. Adoption widened the performance gap between tech-forward and traditional vendors, accelerating M&A activity as incumbents sought digital capabilities to maintain service-level compliance.

Other drivers and restraints analyzed in the detailed report include:

- Vision 2030 Infrastructure Development

- Data-Center Expansion

- HVAC Innovation and Energy-Efficiency Needs

- Skilled-Labor Shortages

- Nationalization-Policy Challenges

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hard services captured 58.75% of 2025 revenue, underpinning mission-critical mechanical, electrical and plumbing systems across harsh climates. Within this cohort, MEP and HVAC activities represented the largest slice as predictive-maintenance suites such as IBM Maximo trimmed procurement steps from 46 to 14 at Petroleum Development Oman, saving 2,300 hours annually. Asset owners locked multiyear contracts to safeguard LEED certifications and align with insurance stipulations.

Soft services, though smaller, posted the fastest expansion trajectory at 14.12% CAGR, buoyed by heightened hygiene, security and employee-experience standards in post-pandemic workplaces. Musanadah's ISSA affiliation illustrated adoption of international cleaning protocols in Saudi hospitals. As flexible workspaces spread, demand for smart reception, barrier-less parking and app-based concierge surged. Catering subcontracts also shifted toward tech-enabled traceability, evidenced by Novotel's seafood audit partnership across 19 hotels. Providers blending both service clusters under single SLAs achieved higher retention, driving integrated-model premiums.

The GCC Facility Management Market Report is Segmented by Service Type (Hard Services, and Soft Services), Offering Type (In-House, and Outsourced), End-User Industry (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, Industrial and Process Sector, and More), and Geography (Qatar, United Arab Emirates, Kuwait, Saudi Arabia, Oman, Bahrain). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Emcor Facilities Services WLL

- Sodexo Qatar Services

- Al-Asmakh Facilities Management

- G4S Qatar SPC

- Facilities Management and Maintenance Company LLC

- Cofely Besix Facility Management

- Como Facility Management Services

- Enova Facilities Management Services LLC (UAE)

- PIMCO Kuwait

- Ecovert FM Kuwait

- Saudi Emcor Company Limited

- Initial Saudi Group

- Oman International Group SAOC

- ENGIE Cofely LLC (Oman)

- Transguard Group (UAE)

- United Facilities Management (UFM Kuwait)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.1.1 Current Commercial Real-Estate Occupancy Rates in GCC Mega-Cities

- 4.1.2 Profitability Benchmarks of Major FM Providers

- 4.1.3 Workforce Indicators - Skilled and Unskilled Labor Participation (Nationalization Impact)

- 4.1.4 Facility Management Market Share (%) by Service Type

- 4.1.5 Facility Management Market Share (%) by Hard Services

- 4.1.6 Facility Management Market Share (%) by Soft Services

- 4.1.7 Urbanization and Population Growth in Top Metro Areas

- 4.1.8 Sector Investment Priorities in GCC Infrastructure Pipeline

- 4.1.9 Regulatory Drivers Specific to Labour and Safety Standards

- 4.2 Market Drivers

- 4.2.1 Vision 2030 infrastructure development

- 4.2.2 AI and IoT integration in building management

- 4.2.3 Data-center expansion

- 4.2.4 HVAC innovation and energy-efficiency needs

- 4.2.5 Green building certification mandates (LEED, Estidama, etc.)

- 4.2.6 Privatization of municipal services driving large FM outsourcing contracts

- 4.3 Market Restraints

- 4.3.1 Skilled-labor shortages

- 4.3.2 Nationalization-policy challenges

- 4.3.3 Inflation-linked service contract cost pressures

- 4.3.4 Regulatory heterogeneity across GCC states complicating cross-border FM operations

- 4.4 Value Chain Analysis

- 4.5 PESTEL Analysis

- 4.6 Regulatory and Legislative Framework for Market Entrants

- 4.7 Impact of Macroeconomic Indicators on FM Demand

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Services

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Investment and Funding Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Services

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard FM Services

- 5.1.2 Soft Services

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft FM Services

- 5.1.1 Hard Services

- 5.2 By Offering Type

- 5.2.1 In-house

- 5.2.2 Outsourced

- 5.2.2.1 Single FM

- 5.2.2.2 Bundled FM

- 5.2.2.3 Integrated FM

- 5.3 By End-user Industry

- 5.3.1 Commercial (IT and Telecom, Retail and Warehouses)

- 5.3.2 Hospitality (Hotels, Eateries, Large-scale Restaurants)

- 5.3.3 Institutional and Public Infrastructure (Govt, Education, Transportation)

- 5.3.4 Healthcare (Public and Private Facilities)

- 5.3.5 Industrial and Process (Manufacturing, Energy, Mining)

- 5.3.6 Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure)

- 5.4 By Country

- 5.4.1 Qatar

- 5.4.2 United Arab Emirates

- 5.4.3 Kuwait

- 5.4.4 Saudi Arabia

- 5.4.5 Oman

- 5.4.6 Bahrain

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Partnerships

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Emcor Facilities Services WLL

- 6.4.2 Sodexo Qatar Services

- 6.4.3 Al-Asmakh Facilities Management

- 6.4.4 G4S Qatar SPC

- 6.4.5 Facilities Management and Maintenance Company LLC

- 6.4.6 Cofely Besix Facility Management

- 6.4.7 Como Facility Management Services

- 6.4.8 Enova Facilities Management Services LLC (UAE)

- 6.4.9 PIMCO Kuwait

- 6.4.10 Ecovert FM Kuwait

- 6.4.11 Saudi Emcor Company Limited

- 6.4.12 Initial Saudi Group

- 6.4.13 Oman International Group SAOC

- 6.4.14 ENGIE Cofely LLC (Oman)

- 6.4.15 Transguard Group (UAE)

- 6.4.16 United Facilities Management (UFM Kuwait)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Technology-led Integrated FM (IoT, BMS, AI-based Predictive Maintenance)

- 7.3 ESG-Compliant FM Solutions Demand

- 7.4 Future Service-Model Shifts (Outcome-Based Contracts)