PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072648

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072648

Spain Integrated Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

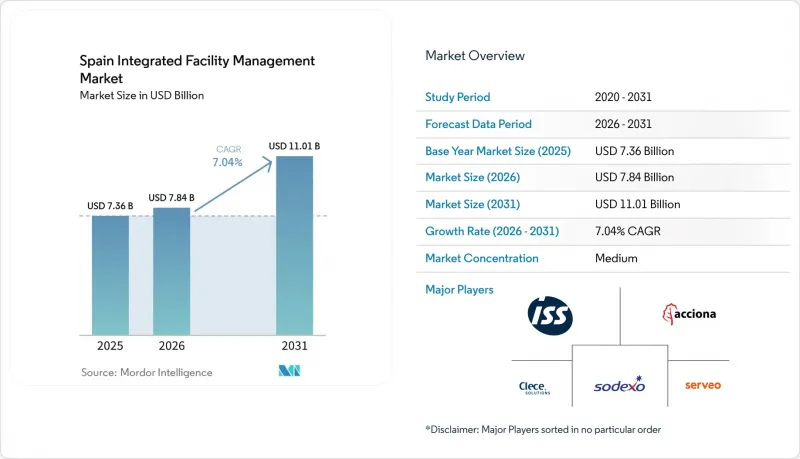

According to Mordor Intelligence, the spain integrated facility management market size is expected to grow from USD 7.36 billion in 2025 to USD 7.84 billion in 2026 and is forecast to reach USD 11.01 billion by 2031 at 7.04% CAGR over 2026-2031.

This report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, and More], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and More]), and End User (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, and More). The Market Forecasts are Provided in Terms of Value (USD).

Spain Integrated Facility Management Market Trends and Insights

Growing Outsourcing of Non-Core Activities

Strategic outsourcing has become a structural operating model in the Spain integrated facility management market because buyers now want simpler governance across cleaning, security, catering, technical maintenance, and workplace support under one contract. The shift is no longer framed only around cost reduction, because large occupiers also want fewer vendor interfaces, tighter reporting lines, and stronger control over service quality across dispersed sites. Mid-sized companies are also moving beyond single-service contracts, which is helping integrated providers win broader scopes and longer terms than they did in earlier outsourcing cycles. Public administration is reinforcing this direction because larger contracts increasingly require stronger digital workflows, clearer performance evidence, and better delivery consistency across public estates. Spain's Plan BIM for Public Procurement made BIM compulsory for public contracts above EUR 5.5 million (USD 6.2 million) from October 2025, which raised the qualification threshold for suppliers seeking larger public assignments. As a result, the Spain integrated facility management market is rewarding operators that can combine operational scale, compliance capacity, and multi-service coordination rather than those that compete only on unit pricing.

Rising Demand for Energy-Efficient Buildings

Energy efficiency is becoming a core growth engine for the Spain integrated facility management market because regulation is turning energy monitoring and optimization into standard contract requirements rather than optional add-ons. Directive (EU) 2024/1275 entered into force in May 2024, and Spain must transpose it into national law by May 2026, which is creating a compliance-led demand cycle for building upgrades, control systems, and technical maintenance. Spain's National Building Renovation Plan is being developed under the recast directive, and the policy framework includes milestones to renovate the weakest-performing non-residential floor area by 2030 and 2033 while targeting a 65% reduction in primary energy use in non-residential buildings by 2050. Spain is also among the EU countries testing the Smart Readiness Indicator, which increases the relevance of building automation, data verification, and third-party performance evidence in technical service contracts. The March 2025 award to ACCIONA Energia for a 5-year EUR 5.6 million (USD 6.3 million) contract covering energy management across more than 400 Madrid City Council buildings shows that municipalities are already outsourcing this work at scale. Providers that can connect compliance, metering, analytics, and operational delivery are therefore likely to capture more renewals as the Spain integrated facility management market moves deeper into energy-led procurement.

High Labor Cost Inflation

Labor cost pressure is the clearest near-term constraint on the Spain integrated facility management market because its largest service areas still depend heavily on labour-intensive delivery models. Soft FM remains especially exposed, since cleaning, security, catering, and front-of-house services are often contracted at fixed prices even when wage obligations rise during the contract term. Spain's FM sector supports more than 600,000 workers directly and indirectly, which means sector-wide wage agreements and social contribution costs have an immediate effect on provider margins and bid discipline. This pressure is also changing investment priorities, because providers are accelerating automation in tasks such as cleaning and monitoring in order to offset the wage path built into multi-year contracts. Spain's General Disability Law adds another compliance layer for larger employers by requiring companies with 50 or more workers to maintain a 2% workforce quota for employees with disabilities. The result is that the Spain integrated facility management market is still growing, but price resets, staffing models, and contract terms are under much closer review than they were in earlier outsourcing cycles.

Other drivers and restraints analyzed in the detailed report include:

- Expansion Of Smart Building Technologies

- EU Taxonomy Pressure on ESG Reporting

- Fragmented Supplier Base in Specific Trades

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Soft Facility Management (FM) held 62.53% of the Spain integrated facility management (IFM) market share in 2025, reflecting the scale and recurrence of cleaning, security, catering, and front-of-house services across public, commercial, and healthcare estates. The segment remains dominant because these activities were among the first building functions that Spanish occupiers and public entities moved outside the organization, which drew greater management attention, while security services are evolving through centralized alarm reception models and remote supervision, giving large FM operators a long runway to build workforce depth and national coverage. That historical path still matters in 2026, because large buyers continue to prefer bundled labor-based services that can be rolled out quickly across many sites without changing the underlying asset base. Spain's General Disability Law also shapes procurement behavior in parts of the market, since buyers often favor established providers with mature workforce programs and broader compliance capacity. Catering is gaining added relevance as workplace quality and employee wellness receive more management attention, while security services are changing through centralized alarm reception models and remote supervision that reduce the need for purely site-bound coverage.

Hard FM is projected to expand at 7.91% CAGR, making it the fastest-growing part of the Spain IFM market size outlook through 2031. The segment is structurally advantaged because technical compliance, building automation, and energy performance are now rising together instead of as separate spending lines. The recast EPBD and Spain's renovation agenda are widening the need for asset management, mechanical and electrical services, fire and life safety work, and energy optimization across non-residential buildings. Spain's HVAC sector grew 11.4% in 2025, driven by aerothermal and geothermal adoption across residential, commercial, and industrial uses, and that larger installed base will need maintenance, diagnostics, and performance verification over time. This shift strengthens the technical side of the Spain integrated facility management industry because compliance, equipment complexity, and lifecycle planning are becoming part of everyday service delivery rather than occasional project work.

Complete Report Scope:

- By Service Type

- Hard Facility Management

- Asset Management

- MEP and HVAC Services

- Fire Systems and Safety

- Other Hard Facility Management Services

- Soft Facility Management

- Office Support and Security

- Cleaning Services

- Catering Services

- Other Facility Management Services

- Hard Facility Management

- By End User Industry

- Commercial

- Hospitality

- Institutional and Public Infrastructure

- Healthcare

- Industrial and Process Sector

- Other End-user Industries

List of Companies Covered in this Report:

- Acciona Facility Services S.A.

- ISS Facility Services Espana S.A.

- Sodexo Espana S.A.

- Clece S.A.

- Serveo Servicios Integrales S.A.

- Grupo Eulen S.A.

- Sacyr Facilities S.L.U.

- Vinci Facilities Iberia S.A.U.

- CBRE Group Inc. (Spain)

- JLL Spain

- Atalian Servest Iberia S.A.U.

- Grupo Norte Agrupacion Empresarial de Servicios S.A.

- ENGIE Cofely Espana S.L.U.

- OHL Servicios Ingesan S.A.

- Grupo SIFU

- Mitie Facilities Management Espana S.L.

- Johnson Controls Spain

- Ferrovial Servicios (Legacy Contracts)

- Altrad Rodisola S.A.U.

- Seralia Facility Services S.L.

- Ilunion Facility Services S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Outsourcing of Non-Core Activities

- 4.2.2 Rising Demand for Energy-Efficient Buildings

- 4.2.3 Expansion of Smart Building Technologies

- 4.2.4 Increasing Workplace Wellness Focus

- 4.2.5 EU Taxonomy Pressure on ESG Reporting

- 4.2.6 Deployment of AI-Enabled Predictive Maintenance

- 4.3 Market Restraints

- 4.3.1 High Labor Cost Inflation

- 4.3.2 Fragmented Supplier Base in Specialized Trades

- 4.3.3 Data-Privacy Concerns in IoT Monitoring

- 4.3.4 Shortage of Certified HVAC Technicians

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Facility Management

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard Facility Management Services

- 5.1.2 Soft Facility Management

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Facility Management Services

- 5.1.1 Hard Facility Management

- 5.2 By End User Industry

- 5.2.1 Commercial

- 5.2.2 Hospitality

- 5.2.3 Institutional and Public Infrastructure

- 5.2.4 Healthcare

- 5.2.5 Industrial and Process Sector

- 5.2.6 Other End-user Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Acciona Facility Services S.A.

- 6.4.2 ISS Facility Services Espana S.A.

- 6.4.3 Sodexo Espana S.A.

- 6.4.4 Clece S.A.

- 6.4.5 Serveo Servicios Integrales S.A.

- 6.4.6 Grupo Eulen S.A.

- 6.4.7 Sacyr Facilities S.L.U.

- 6.4.8 Vinci Facilities Iberia S.A.U.

- 6.4.9 CBRE Group Inc. (Spain)

- 6.4.10 JLL Spain

- 6.4.11 Atalian Servest Iberia S.A.U.

- 6.4.12 Grupo Norte Agrupacion Empresarial de Servicios S.A.

- 6.4.13 ENGIE Cofely Espana S.L.U.

- 6.4.14 OHL Servicios Ingesan S.A.

- 6.4.15 Grupo SIFU

- 6.4.16 Mitie Facilities Management Espana S.L.

- 6.4.17 Johnson Controls Spain

- 6.4.18 Ferrovial Servicios (Legacy Contracts)

- 6.4.19 Altrad Rodisola S.A.U.

- 6.4.20 Seralia Facility Services S.L.

- 6.4.21 Ilunion Facility Services S.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment