PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044240

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044240

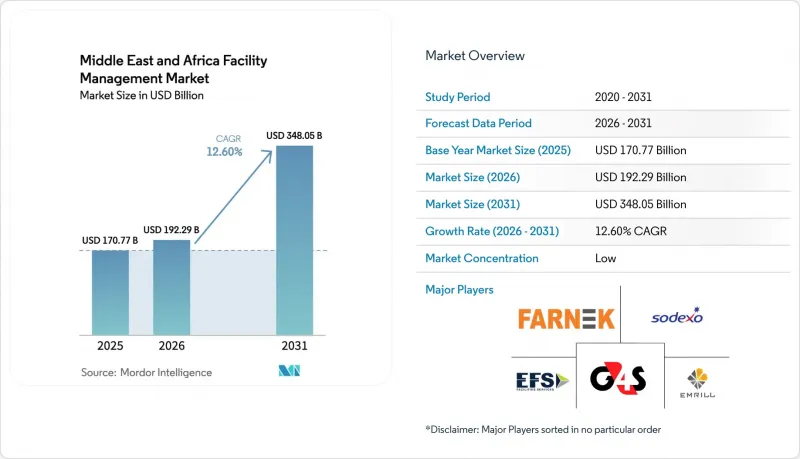

Middle East And Africa Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Middle East and Africa facility management market size was valued at USD 170.77 billion in 2025 and estimated to grow from USD 192.29 billion in 2026 to reach USD 348.05 billion by 2031, at a CAGR of 12.60% during the forecast period (2026-2031).

Mounting infrastructure outlays across Saudi Arabia, the United Arab Emirates, Egypt and South Africa shaped a sizeable pipeline of assets that, in turn, lifted demand for bundled and integrated facility services. Outsourced contracts attracted the bulk of new spending as corporate and public-sector owners increasingly shifted to outcome-based agreements that tied service fees to uptime, energy use and occupant-experience metrics. Digitalisation accelerated across the Middle East and Africa facility management market, with predictive maintenance, IoT-enabled building management systems, and digital-twin platforms optimizing energy consumption and reducing unplanned downtime in critical equipment fleets. Competitive differentiation therefore hinged on data analytics skills and the ability to embed ESG reporting into day-to-day operations, especially on mega projects such as NEOM and the King Abdullah Financial District. At the same time, consolidation quickened as global majors partnered with regional specialists to expand geographic reach and deepen sector know-how.

Middle East And Africa Facility Management Market Trends and Insights

Increasing Infrastructure Development

Saudi Arabia alone had awarded significant construction contracts in 2024 under Vision 2030, and NEOM's USD 500 billion masterplan stimulated significant spike in sector-wide wages, underscoring how large-scale projects fuelled service volumes across the Middle East and Africa facility management market. In Africa, the syndicated facility raised by Africa Finance Corporation in March 2024 signaled renewed capital inflows aimed at closing the funding gap and thereby broadening the asset base requiring lifecycle support. The UAE real estate boom similarly lifted demand for technical asset care in premium office, residential, and retail stock. As a cumulative result, facility executives sought providers able to scale quickly, standardize processes, and manage complex stakeholder groups across multi-phase developments.

Rising Outsourcing in Building Management

Outsourcing gained momentum after landmark deployments such as the King Abdullah Financial District, where an integrated contract underpinned by IBM Maximo boosted customer-satisfaction scores by 95% while lowering corrective maintenance outlays, demonstrating quantifiable value creation for owners. Regulatory bodies followed suit; for example, the Middle East Facility Management Association and Rera Ajman signed a June 2024 accord to formalise best practice and training pathways, institutionalising outsourced models in residential towers and mixed-use precincts. Healthcare operators were early adopters, entrusting critical-environment compliance to external teams steeped in infection-control protocols. Outcome-based contracts tied payments to uptime and energy KPIs, aligning incentives and lengthening average contract tenures.

Skilled Labour Shortages

Africa faced a significant demand for additional project-management professionals annually through 2030. However, training pipelines struggled to meet this demand, leaving critical supervisory positions unfilled and hindering the growth of the Middle East and Africa facility management market. In the Gulf, mechanical-electrical-plumbing firms reported mid-management knowledge gaps that delayed the implementation of digital systems and reduced productivity. In 2024, there is a significant need for upskilling in the construction sector, leading employers to hesitate in investing in training due to high personnel turnover. The scarcity of green-building specialisms further compounded the challenges faced in smart-asset optimisation projects.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advancements in Facility Management

- ESG-Driven Facility Operations Demand

- Volatile Economic Conditions and Oil Price Swings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hard services controlled 56.25% of the Middle East and Africa facility management market in 2025, underpinned by mandatory HVAC, fire-safety and asset-integrity programs designed for harsh climates and high-occupancy assets. Within that basket, MEP services captured most spend, as energy-optimisation retrofits became obligatory for Grade-A stock. Soft services displayed brisk 12.78% CAGR and were increasingly bundled into integrated contracts that elevated occupant-wellbeing metrics and ESG reporting quality.

Soft-service growth reflected expanded scope spanning sustainable cleaning chemicals, wellness certifications and tenant-engagement analytics. Although smaller in absolute value, soft services represented a strategic pathway for providers to embed themselves in client organisations and cross-sell higher-margin advisory work. The dynamic signalled further incremental share gain for soft services within the Middle East and Africa facility management market size during the forecast horizon.

The Middle East and Africa Facility Management Market Report is Segmented by Service Type (Hard Services, and Soft Services), Offering Type (In-House, and Outsourced), End-User Industry (Commercial, Hospitality, and More), and Geography (Saudi Arabia, United Arab Emirates, Qatar, Kuwait, South Africa, Egypt, Nigeria, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Engie Cofely Energy Services LLC (Engie SA)

- EFS Facilities Services Group

- Ejadah Asset Management Group

- Emrill Services LLC

- Farnek Services LLC

- Bidvest Facilities Management

- Kharafi National for Infrastructure Projects Developments Construction & Services SAE

- Initial Saudi Group

- Sodexo

- Ecolab

- Imdaad

- G4S

- CBRE Group Inc.

- ISS A/S

- Jones Lang LaSalle Incorporated

- Khidmah LLC

- Transguard Group

- Al Shirawi Facilities Management LLC

- Serco Group Middle East

- Aramark Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Infrastructure Development

- 4.2.2 Rising Outsourcing in Building Management

- 4.2.3 Heightened Safety and Security Needs

- 4.2.4 Technological Advancements in Facility Management

- 4.2.5 ESG-Driven Facility Operations Demand

- 4.2.6 FM Demand from Giga Mixed-Use Projects

- 4.3 Market Restraint

- 4.3.1 Skilled Labour Shortages

- 4.3.2 Regulatory Challenges

- 4.3.3 Volatile Economic Conditions and Oil Price Swings

- 4.3.4 Fragmented FM Standards Across MEA Countries

- 4.4 Industry Value Chain Analysis

- 4.5 PESTEL Analysis

- 4.6 Regulatory and Legislative Framework for Market Entrants

- 4.7 Impact of Macroeconomic Indicators on FM Demand

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Services

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Investment and Funding Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Services

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard Services

- 5.1.2 Soft Services

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft Services

- 5.1.1 Hard Services

- 5.2 By Offering Type

- 5.2.1 In-house

- 5.2.2 Outsourced

- 5.2.2.1 Single FM

- 5.2.2.2 Bundled FM

- 5.2.2.3 Integrated FM

- 5.3 By End-user Industry

- 5.3.1 Commercial (IT and Telecom, Retail and Warehouses)

- 5.3.2 Hospitality (Hotels, Eateries, Large-scale Restaurants)

- 5.3.3 Institutional and Public Infrastructure (Govt, Education, Transportation)

- 5.3.4 Healthcare (Public and Private Facilities)

- 5.3.5 Industrial and Process (Manufacturing, Energy, Mining)

- 5.3.6 Other End-user Industry

- 5.4 By Country

- 5.4.1 Saudi Arabia

- 5.4.2 United Arab Emirates

- 5.4.3 Qatar

- 5.4.4 Kuwait

- 5.4.5 South Africa

- 5.4.6 Egypt

- 5.4.7 Nigeria

- 5.4.8 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Partnerships

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Engie Cofely Energy Services LLC (Engie SA)

- 6.4.2 EFS Facilities Services Group

- 6.4.3 Ejadah Asset Management Group

- 6.4.4 Emrill Services LLC

- 6.4.5 Farnek Services LLC

- 6.4.6 Bidvest Facilities Management

- 6.4.7 Kharafi National for Infrastructure Projects Developments Construction & Services SAE

- 6.4.8 Initial Saudi Group

- 6.4.9 Sodexo

- 6.4.10 Ecolab

- 6.4.11 Imdaad

- 6.4.12 G4S

- 6.4.13 CBRE Group Inc.

- 6.4.14 ISS A/S

- 6.4.15 Jones Lang LaSalle Incorporated

- 6.4.16 Khidmah LLC

- 6.4.17 Transguard Group

- 6.4.18 Al Shirawi Facilities Management LLC

- 6.4.19 Serco Group Middle East

- 6.4.20 Aramark Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Technology-led Integrated FM (IoT, BMS, AI-based Predictive Maintenance)

- 7.3 ESG-Compliant FM Solutions Demand

- 7.4 Future Service-Model Shifts (Outcome-Based Contracts)