PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044276

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044276

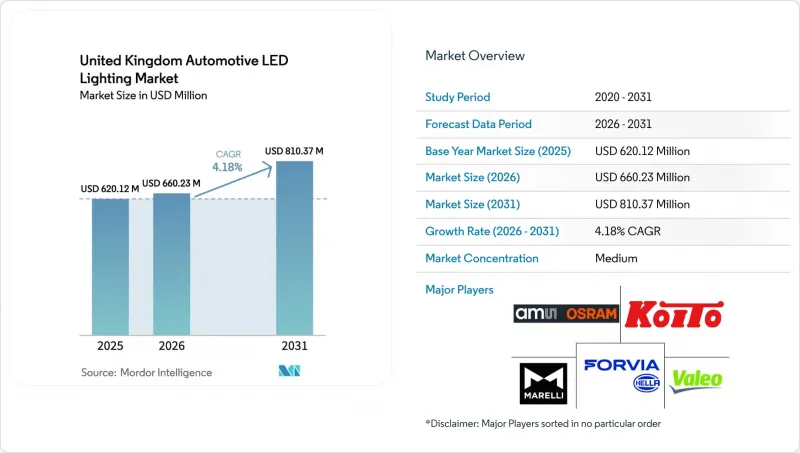

United Kingdom Automotive LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The United Kingdom Automotive LED Lighting Market size is projected to be USD 620.12 million in 2025, USD 660.23 million in 2026, and reach USD 810.37 million by 2031, growing at a CAGR of 4.18% from 2026 to 2031.

The steady uptrend reflects the country's migration from halogen toward semiconductor-based illumination, a shift accelerated by mandatory LED head-lamp rules, expanding electric-vehicle (EV) registrations, and a vibrant retrofit culture that prizes design flexibility and lower energy draw. Rising smart-motorway coverage is pushing adaptive head-lamp adoption, while declining emitter prices down 15-20% between 2023 and 2025 are squeezing the halogen cost advantage. Supply-chain pressures for gallium-nitride wafers and rare-earth phosphors remain a constraint, yet Tier-1 suppliers are mitigating risk through multi-sourcing and localized inventories. Competitive intensity is tempered by circular-economy moves such as remanufactured LED head-lamps, which lower total cost of ownership and widen market access.

United Kingdom Automotive LED Lighting Market Trends and Insights

Mandatory LED Head-Lamp Regulations for New Vehicles

The 2024 rule requiring LED or equivalent semiconductor head-lamps on new type-approved vehicles has turned compliance into a non-negotiable design parameter. Domestic plants assembled 779,584 cars in 2024, and more than 2 million new vehicles reached UK roads in 2025, each now budgeting for LED modules. Tier-1 suppliers have compressed validation cycles joint programs between Valeo and ams OSRAM trimmed ambient-lighting integration from two years to under one setting a new pace for head-lamp rollouts. Ready-certified products such as the ECE R128-approved XLS LR6 rear LED shorten OEM testing, further accelerating penetration. Assembly lines have retooled for thermal-management demands, raising capital outlays yet lowering inventory obsolescence risk. Overall, this regulation adds 1.2 percentage points to the forecast CAGR of the United Kingdom automotive LED lighting market.

Declining LED Component Costs and Higher Energy Efficiency

Emitter oversupply in Asian fab clusters shaved up to one-fifth off LED prices between 2023 and 2025, unlocking mass-market adoption of 180-lumen rear modules once limited to premium trims. Power draw for full-LED head-lamps is 40-60% lower than halogen, an energy gain prized by EV makers seeking longer WLTP ranges. The United Kingdom counted 1.759 million zero-emission vehicles on the road in 2025, a captive base for energy-efficient lighting. Marelli's LeanLight architecture cut cost by 22% and parts count by 34%, illustrating the march toward cost parity. These gains lift retrofit appeal but compress margins, as plug-and-play kits reach price points acceptable to value-oriented drivers.

Higher Upfront Cost of LED Modules vs Halogen

Full-LED head-lamp assemblies still price 40-70% above halogen, producing payback periods longer than many ownership cycles in cost-sensitive regions. A retrofit pair can cost up to GBP 400 (USD 504) installed versus GBP 50 (USD 63) for halogen bulbs, limiting penetration among budget-constrained motorists. FORVIA HELLA's 9M 2025 margin squeezed to 2.7% as suppliers absorbed cost inflation rather than pass it through, underscoring profitability pressure. Price resistance is most acute in Northern Ireland and Wales, where used-vehicle sales dominate, clipping 0.6 percentage points from the forecast CAGR.

Other drivers and restraints analyzed in the detailed report include:

- Rising Electric-Vehicle Sales Boosting Demand for Advanced Lighting

- Aftermarket Demand for Aesthetic and Performance Upgrades

- Supply-Chain Risk for Gallium-Nitride and Rare-Earth Inputs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The aftermarket represented 68.11% of United Kingdom automotive LED lighting market revenue in 2025, buoyed by a 41.964 million-vehicle parc where the median age exceeds eight years. Independent garages leverage this installed base, offering retrofit kits that reduce energy draw and bulb-replacement downtime. The United Kingdom automotive LED lighting market size for OEM sales is smaller, yet OEM revenue is forecast to climb at a 4.83% CAGR as factory-fit LED head-lamps become standard equipment on new EVs and ADAS-enabled models.

OEM adoption is propelled by the 2024 mandate and by design-win pipelines exceeding EUR 2.5 billion (USD 2.83 billion) at ams OSRAM, evidencing long-term volume visibility. Valeo's April 2025 rollout of a remanufactured LED head-lamp blurs the aftermarket-OEM divide by offering OE quality at retrofit prices. Meanwhile, distributors need value-added services mobile fitting or subscription lighting upgrades to protect margins against falling component costs.

Passenger cars delivered 62.36% of United Kingdom automotive LED lighting market share in 2025 thanks to their registration volume and high LED take-rates in premium trims. Yet light commercial vehicles (LCVs) are expanding at 5.12% through 2031 as last-mile operators electrify vans and specify adaptive LEDs compatible with smart-motorway systems.

Zero-emission LCVs captured 9.8% of registrations in Q3 2025, up from 5.7% a year earlier. Fleet managers view LED efficiency 40-60% lower power draw than halogen as critical for range and payload. Orders such as FORVIA HELLA's 2025 LED work-lamp contract with a European bus maker confirm spillover into heavy vehicles. Two-wheelers lag due to cost sensitivity, but an emerging micro-mobility segment could shift that balance later in the decade.

The United Kingdom Automotive LED Lighting Market Report is Segmented by Sales Channel (OEM, and Aftermarket), Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, and Two-Wheelers), Installation Type (New Installation, and Retrofit Installation), Application (Exterior Lighting, and Interior Lighting). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Valeo SE

- Hella GmbH & Co. KGaA (FORVIA SE)

- Koito Manufacturing Co., Ltd.

- ams OSRAM AG

- Marelli Holdings Co., Ltd.

- Stanley Electric Co., Ltd.

- Hyundai Mobis Co., Ltd.

- Robert Bosch GmbH

- ZKW Group GmbH

- Lumileds Holding B.V.

- Lear Corporation

- Varroc Engineering Limited

- Denso Corporation

- Gentex Corporation

- Continental AG

- Panasonic Holdings Corporation

- Koninklijke Philips N.V.

- Eaton Corporation plc

- Signify N.V.

- Flex-N-Gate Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandatory LED Head-Lamp Regulations for New Vehicles

- 4.2.2 Declining LED Component Costs and Higher Energy Efficiency

- 4.2.3 Rising Electric-Vehicle Sales Boosting Demand for Advanced Lighting

- 4.2.4 Aftermarket Demand for Aesthetic and Performance Upgrades

- 4.2.5 Smart-Motorway Projects Driving Adaptive Head-Light Adoption

- 4.2.6 Tax Incentives for Domestic Semiconductor Packaging

- 4.3 Market Restraints

- 4.3.1 Higher Upfront Cost of LED Modules vs. Halogen

- 4.3.2 Supply-Chain Risk for Gallium-Nitride and Rare-Earth Inputs

- 4.3.3 Stringent UK Glare Regulations Limiting High-Lumen Retrofits

- 4.3.4 Surge in Imported Second-Hand Cars with Halogen Lamps

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of Substitutes

- 4.8.4 Threat of New Entrants

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Sales Channel

- 5.1.1 OEM

- 5.1.2 Aftermarket

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles

- 5.2.3 Heavy Commercial Vehicles

- 5.2.4 Two-Wheelers

- 5.3 By Installation Type

- 5.3.1 New Installation

- 5.3.2 Retrofit Installation

- 5.4 By Application

- 5.4.1 Exterior Lighting

- 5.4.1.1 Headlamps

- 5.4.1.2 Daytime Running Lights

- 5.4.1.3 Taillights

- 5.4.1.4 Fog Lamps

- 5.4.1.5 Turn Signals

- 5.4.1.6 Other Exterior Lightings

- 5.4.2 Interior Lighting

- 5.4.2.1 Dome and Map Lights

- 5.4.2.2 Ambient Lighting

- 5.4.2.3 Instrument Cluster and Infotainment Back-Lighting

- 5.4.2.4 Other Interior Lightings

- 5.4.1 Exterior Lighting

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Valeo SE

- 6.4.2 Hella GmbH & Co. KGaA (FORVIA SE)

- 6.4.3 Koito Manufacturing Co., Ltd.

- 6.4.4 ams OSRAM AG

- 6.4.5 Marelli Holdings Co., Ltd.

- 6.4.6 Stanley Electric Co., Ltd.

- 6.4.7 Hyundai Mobis Co., Ltd.

- 6.4.8 Robert Bosch GmbH

- 6.4.9 ZKW Group GmbH

- 6.4.10 Lumileds Holding B.V.

- 6.4.11 Lear Corporation

- 6.4.12 Varroc Engineering Limited

- 6.4.13 Denso Corporation

- 6.4.14 Gentex Corporation

- 6.4.15 Continental AG

- 6.4.16 Panasonic Holdings Corporation

- 6.4.17 Koninklijke Philips N.V.

- 6.4.18 Eaton Corporation plc

- 6.4.19 Signify N.V.

- 6.4.20 Flex-N-Gate Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment